Worker Voice and Firm Governance

What happens when workers get a formal seat at the table in corporate governance? In many European countries, laws require that worker representatives serve on company boards and participate in management decisions, a shared governance system known as codetermination. Germany's version, dating to the postwar era in its current form, is perhaps the most prominent: workers elect representatives to corporate supervisory boards, and establishment-level works councils participate in day-to-day workplace decisions. During its long history, codetermination has regularly attracted attention in countries that typically exclusively rely on shareholder control, such as the United States or the United Kingdom. The central question for economists is whether giving workers formal representation in firm governance meaningfully affects wages, productivity, and investment—and if so, in which direction—or whether it primarily affects only subjective (but arguably important) outcomes, such as workers' sense of voice and dignity. Over the past several years, we have pursued a research agenda examining this question, combining quasi-experimental reform-based research designs in Germany and Finland with cross-country analyses. Our empirical findings point to a nuanced pattern: codetermination is a moderate institution, one that neither dramatically raises wages nor harms firms through reduced investment, but whose effects depend importantly on institutional design. It might have different effects depending on the overall institutional environment it is embedded in. And open questions include effects on financial performance, innovation, subjective outcomes, and, importantly, its aggregate equilibrium effects.

The German System of Industrial Relations

To understand codetermination, it helps to understand the broader institutional landscape in which it operates. In a recent overview, we describe the "German model" of industrial relations as resting on two pillars.1 The first is sectoral collective bargaining—with the twist of employer choice: industry-level unions and employer associations negotiate collective bargaining agreements that set wage floors and working conditions for entire sectors and regions. But rather than accepting the imposition of wage floors on all firms through mandatory coverage or through widespread extensions of those agreements to all employers, German employers can decide whether to accept these wage floors or to retain wage-setting flexibility. As of 2020, about 52 percent of German workers were covered by such agreements—far above the roughly 6 percent private-sector coverage rate in the United States but far below the coverage rate in Italy or the Nordic countries, for example, even though only 15 percent of German workers belong to a union. This institutional architecture differs starkly from the American system of employer-level bargaining: In the United States, coverage and membership nearly coincide, collective bargaining agreements do not allow for upward wage flexibility, union voice in management decision-making is largely curtailed, and employer resistance to unionization is common.

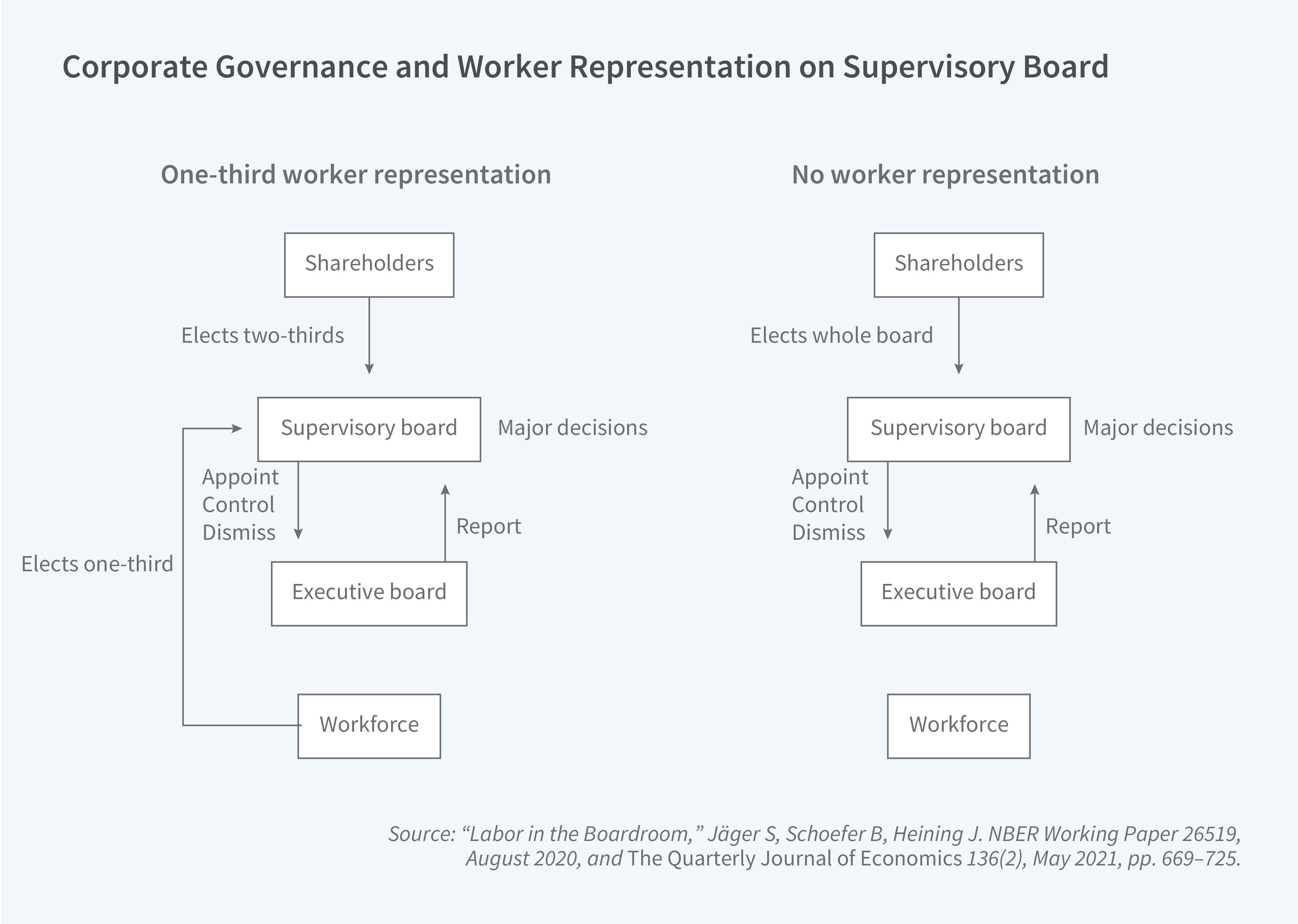

The second and less-studied pillar is firm-level codetermination. It operates through two channels. Under board-level codetermination, workers in larger firms elect representatives to the corporate supervisory board—the body that appoints and monitors the executive board. Firms with 500 to 2,000 employees must allocate one-third of supervisory board seats to workers; firms with more than 2,000 employees must allocate one-half, though shareholders retain a tie-breaking vote. Through shop-floor codetermination, workers in any establishment with at least five employees may elect a works council with co-decision-making rights over working hours, leave schedules, monitoring, and dismissal procedures. About 40 percent of German workers are covered by works councils.

Does Board-Level Representation Raise Wages?

A fundamental question about codetermination is whether giving workers seats on corporate boards increases their bargaining power and, in turn, their wages—i.e., whether codetermination is essentially another version of local level unions and should be viewed through the lens of a US-style union model. An alternative view, advanced by the proponents of the shareholder values paradigm, is that board-level codetermination will ultimately lower wages through an exacerbation of hold-up and agency problems.2

In a study with Jörg Heining, we address this question using a natural experiment in Germany.3 In 1994, a reform of the Stock Corporation Act abolished the one-third board-level representation mandate for stock corporations incorporated after August 10, 1994. Crucially, the mandate was preserved—grandfathered—for corporations incorporated before that date. This created sharp, cohort-based variation in board composition among otherwise similar firms: corporations created just before the cutoff were required to have one-third worker representation on their supervisory boards, while their slightly younger peers created just after were not (unless they grew above the 500-employee threshold at which a size-based one-third mandate would kick in again). This variation motivated the first micro difference-in-differences design of this codetermination institution, for which causal inference in credible identification design has been elusive due to endogeneity concerns. Figure 1 depicts the two forms of corporate governance structures resulting from the German system.

Using administrative matched employer-employee data covering the universe of German social security records, our main outcome variable is worker-level outcomes. That is, we compare wages in firms incorporated just before (subject to codetermination) and after the August 1994 cutoff (no longer subject to it). As a second difference, we also draw on a control group of firms: limited liability companies, whose codetermination rules were unaffected by the reform.

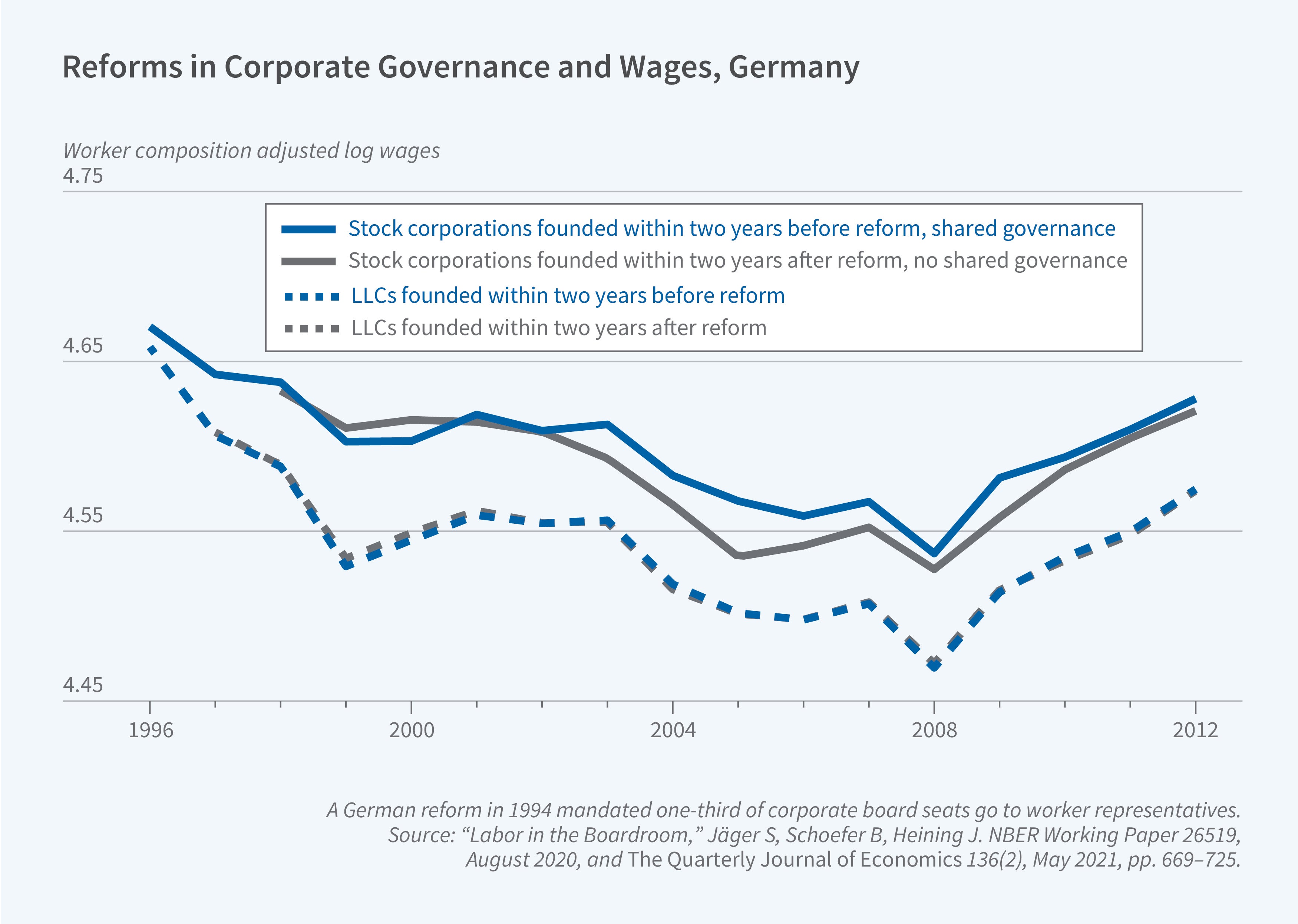

The empirical evidence paints a relatively moderate picture of this facet of German codetermination: Board-level worker representation has no detectable effect on wages or the wage structure within the firm. Our point estimates are close to zero, and the confidence intervals allow us to rule out wage effects larger than about 4 percent. Both the point estimates around zero and the small positive confidence intervals are well below the cross-sectional union wage premium of 10 to 20 percent typically estimated in the United States. Moreover, we find no effects on within-firm wage inequality, no shift in the degree of rent sharing between firms and workers, and no change in the labor share of revenue. Figure 2 illustrates the wage effects for composition-adjusted wages.

We also find no evidence of the hold-up costs predicted by some economic theories: if workers use their board positions to extract rents, firms might reduce investment in response. In fact, codetermined firms have, if anything, slightly higher capital intensity. This directly contradicts influential predictions that worker representation would lead firms to underinvest. The result is consistent with the institutional reality that worker representatives on German supervisory boards hold a minority of seats, do not directly set wages, and tend to exercise their role cooperatively rather than in an adversarial manner.

A Broader View of Codetermination's Effects

Our German findings are echoed by evidence from other settings. In a comprehensive assessment with Shakked Noy, we survey the available micro-level evidence on codetermination across multiple countries (and complement it with new macro-level analysis, summarized below).4 We hope that future research in other settings will continue to emerge, whether it evaluates historic or emerging reforms.

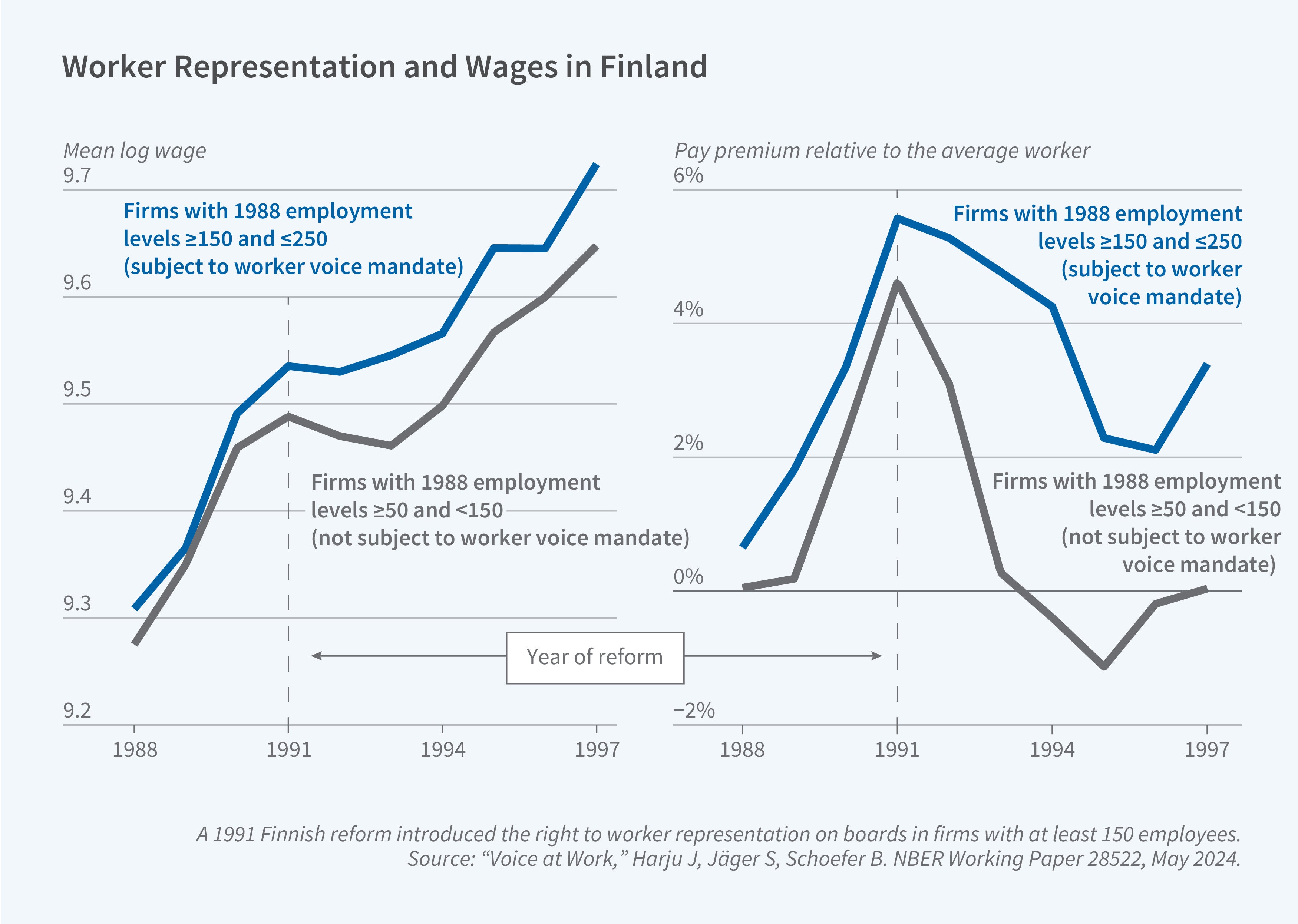

Reform-based quasi-experimental studies are difficult to implement as codetermination institutions are typically stable, with clean introductions or phase-outs being rare and rules in place before the advent of high-quality micro data. With Jarkko Harju, we studied the 1991 introduction of board-level codetermination in Finland.5 Here, the micro evidence points in the same direction: board-level worker representation has small, positive effects on wages. Figure 3 illustrates this effect. Effects on firm performance measures such as productivity, investment, and survival tend to be positive as well, with no evidence of adverse effects and more sizable, positive effects on labor productivity.

Consistent with these findings, firms do not appear to bunch just below the employee thresholds at which codetermination mandates take effect, providing revealed-preference evidence that the institutions do not impose large costs on firms that those firms seek to avoid. This evidence echoes our results from Germany, where in the temporal dimension we found no evidence that stock corporations avoided codetermination by delaying incorporation.

These findings raise the broader question about which particular designs of codetermination may yield gains for workers or both sides, without employer opposition. In fact, in Finland, firms and workers negotiate the particular form of worker involvement, resulting in information sharing and softer worker voice, in contrast to the perhaps uniquely strong form that has emerged and remained persistent in the German context. These results suggest that the design of worker representation may matter considerably. Designs closer to pure voice—facilitating information exchange without reallocating formal decision-making power—appear to generate measurable productivity gains and employment stability, even when they do not substantially shift bargaining power over wages.

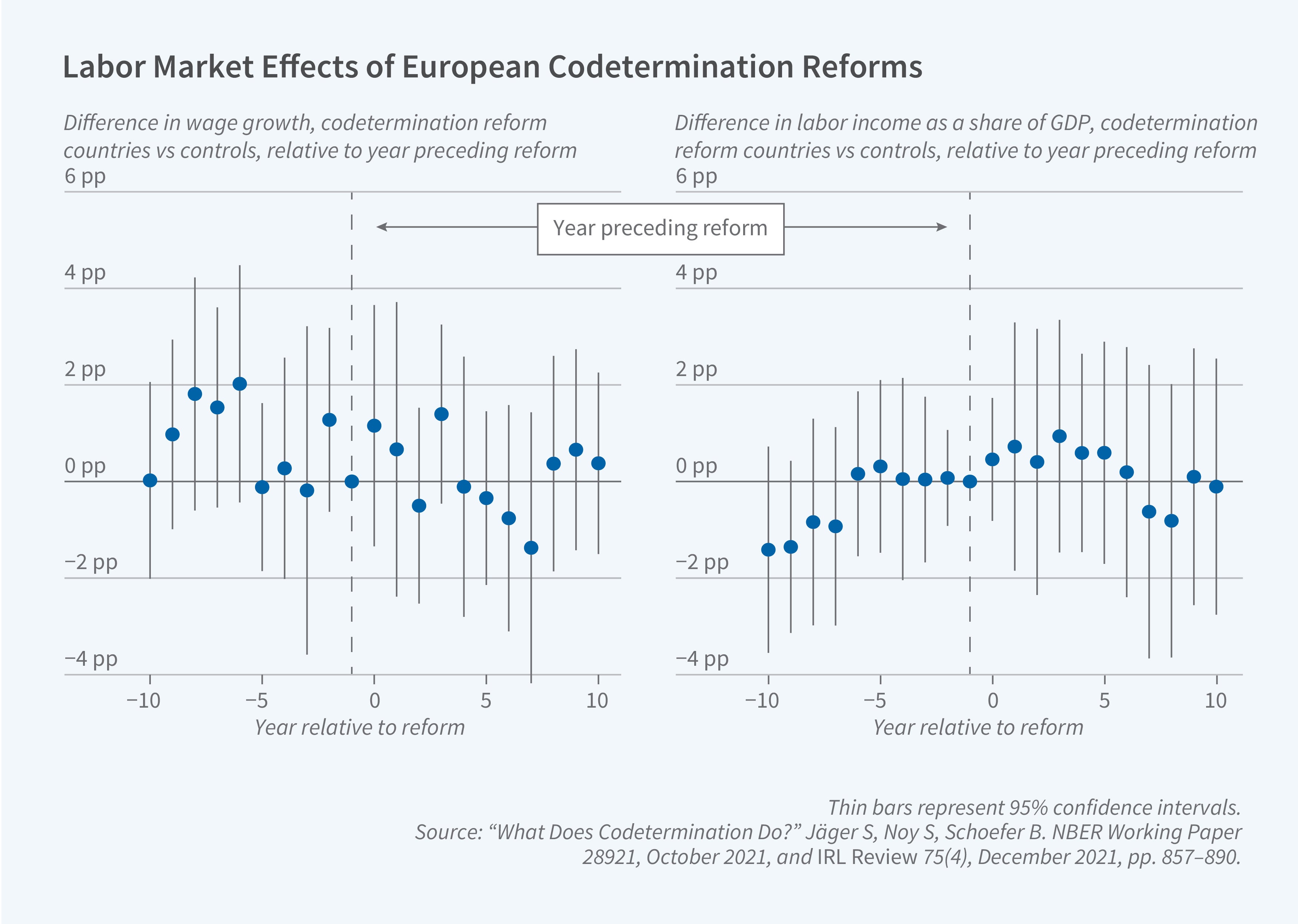

To assess whether these micro-level findings hold in the aggregate, our work with Noy also implements country-level event studies around 10 major codetermination reforms across 14 European democracies from 1960 to 2019 using a synthetic control approach. We find no significant effects of codetermination reforms on wage growth, the labor share, total factor productivity growth, or GDP per capita growth. Figure 4 illustrates these findings for wages and the labor share.

In these country-level panel regressions, confidence intervals widen substantially. This limitation reflects the typical tension between credibly identified micro estimates and attempts to gain insights into the aggregate equilibrium effects of such institutions. Our hope is that the literature continues to make progress not just on the micro end of the spectrum.

We identify three explanations for codetermination's limited effects. First, existing laws impart relatively little formal authority to workers: Board-level representation is almost always a minority position, meaning shareholders can always outvote worker representatives. The specific strength and design of worker rights vary across countries, and we suspect that important insights can be gained by leveraging this qualitative variation of codetermination rules. Second, drawing on survey data, we find that many European workplaces already exhibit high levels of informal worker participation, so the marginal contribution of formal representation may be small. Third, where it exists, codetermination operates alongside complementary institutions—sectoral bargaining, strong labor regulations, and relatively cooperative labor-management norms—that may already manage the problems codetermination and worker representation would otherwise address. All these considerations require a nuanced approach to extrapolating context-specific estimates of causal effects, especially in environments such as the United States. However, recent work on the introduction of board-level representation in large French firms in 2015 finds similar results as those in the German and Finnish contexts, even though industrial relations in France are substantially more contentious and adversarial than in Germany or Finland.6

Collective Bargaining in International Perspective

The overall findings on codetermination raise the question of how related labor market institutions shape wages and inequality across countries and bring to the forefront their heterogeneous designs. In a recent study with Suresh Naidu, we turn our focus back to the institutions that have traditionally received more attention from labor economists: collective bargaining systems.

This study estimates the effect or workings of coverage and collective bargaining across 18 advanced economies using harmonized employer-employee data, a departure from the usual country-level approach in the literature.7 The institutional variation is enormous: collective bargaining coverage ranges from about 12 percent in the United States to near-universality in France, and bargaining structures differ dramatically in their centralization, coordination, and flexibility. As such, our study also provides a systematic description and comparison of the institutional features, besides estimating country-level effects of coverage on wage structures.

The harmonized design permits us to reach new comparative econometric conclusions. For instance, a central empirical finding is that while there is a strong cross-country correlation between higher bargaining coverage and lower wage inequality, the direct micro-level effects of coverage on individual workers' wages are too small to fully account for this pattern.

Understanding the role of spillovers, equilibrium effects, and the broader institutional environment remains an important frontier for research—both for the traditional study of collective bargaining systems and for less studied labor market institutions such as codetermination.

Endnotes

The German Model of Industrial Relations: Balancing Flexibility and Collective Action, Jäger S, Noy S, Schoefer B. NBER Working Paper 30377, August 2022, and Journal of Economic Perspectives 36(4), Fall 2022, pp. 53–80.

Rights and Production Functions: An Application to Labor-Managed Firms and Codetermination, Jensen MC, Meckling WH. The Journal of Business 52(4), October 1979, pp. 469–506. In 1979, Jensen and Meckling assessed the consequences of codetermination as follows: “[T]he workers will begin ‘eating it up’ [the firm] by transforming the assets of the firm into consumption or personal assets[...]. It will become difficult for the firm to obtain capital in the private capital markets. [...] The result of this process will be a significant reduction in the country’s capital stock, increased unemployment, reduced labor income, and an overall reduction in output and welfare.”

Labor in the Boardroom, Jäger S, Schoefer B, Heining J. NBER Working Paper 26519, August 2020, and The Quarterly Journal of Economics 136(2), May 2021, pp. 669–725.

What Does Codetermination Do? Jäger S, Noy S, Schoefer B. NBER Working Paper 28921, October 2021, and IRL Review 75(4), December 2021, pp. 857–890.

Voice at Work, Harju J, Jäger S, Schoefer B. NBER Working Paper 28522, May 2024, and American Economic Journal: Applied Economics 17(3), July 2025, pp. 271–309.

A Seat at the Table: The Effects of Workers' Representation on Firm Performance and Jobs, Mina A, Moschella D, Tiedtke J. SSRN, September 10, 2025.

Collective Bargaining, Unions, and the Wage Structure: An International Perspective, Jäger S, Naidu S, Schoefer B. NBER Working Paper 33267, December 2024, and forthcoming in Handbook of Labor Economics.