Interbank Network Risk, Regulation, and Financial Crises

The financial crisis of 2008–09 intensified interest in how relationships within the financial system can amplify and transmit shocks. At a basic level, firms took advantage of rising real estate prices by scaling up lending and leverage, which fueled further increases in asset prices. When asset price growth slowed, problems at individual financial institutions suggested problems at other firms and triggered a reduced ability to borrow for many firms, whether or not they were contractually connected to the mortgage credit shock. For example, in September 2008, the inability of the Reserve Primary Fund to maintain a constant $1 per share price led to runs on other money market mutual funds, including many that had little or no direct exposure to Lehman Brothers or the Reserve Primary Fund. Moreover, as the interbank lending market collapsed, banks scrambled to hoard reserves as a means of self-insurance against prospective liquidity needs, further aggravating declines in asset prices and lending.

Despite the importance of modern financial markets, their complexity makes it hard to study the effects of asset price shocks or how they are transmitted and amplified across firms and markets. For instance, information about a bank's interconnections with other lenders — its "counter-party positions" — is often closely held and accessible to only a handful of researchers at regulatory agencies. Further, with many banks having international branches and engaged in a wide variety of off-balance-sheet activities, it is difficult to distinguish the effect of a single shock or policy from other concurrent factors.

My research uses the lens of history for insight into these dynamics. US financial history is advantageous for a variety of reasons. First, as most states prohibited or severely restricted interstate bank branching, the financial statements of individual banks reflect their lending to local customers. This creates a large sample of banks to study, each of which operates in a distinct economic environment. Moreover, historically, few banks engaged in significant off-balance-sheet activity. This structure facilitates the identification of the effects of shocks to individual banks from other simultaneous macroeconomic factors. Second, the financial statements of each bank were publicly available, and publications often listed each bank's specific interbank correspondent connections. The historical period, therefore, is the only time when a full picture of the nation's interbank network can be studied without confidential data. Third, there was a great deal of regulatory variation within the country's unified legal and monetary system. Each state had regulatory control over its state-chartered banks, while national banks chartered by the Comptroller of the Currency faced a common set of regulations throughout the country. This feature allows the study of banks that are in the same location and during the same year, but subject to different sets of regulations. As highlighted below, the historical environment sheds light not only on the factors that lead to financial panics, but also on how interbank dynamics play out during panics.

Commodity Shocks and Regulation

As in 2008–09, asset price booms and busts historically were often intertwined with lending booms and busts. Rising asset prices can stimulate lending and increased leverage, which in turn cause asset prices to rise further. Similarly, falling asset prices can force debt contraction and deleveraging that reinforce the decline in asset prices. The interrelationship between asset prices and lending booms thus raises important questions, including how various regulations and policies affect the vulnerability of the banking system to asset price shocks, and how bank lending and instability can exacerbate asset price movements. I have sought to use the unique variations in the historical environment to examine the roles that lending and regulation play in boom-bust events.

David Wheelock and I examine bank lending in the boom-bust cycle affecting US agricultural land prices during and after World War I.1 The wartime collapse of European agriculture drove commodity prices sharply higher and, for the United States, constituted an external demand shock that sparked a boom in farmland prices. However, European production bounced back quickly when the war ended, driving down US crop prices and initiating a wave of farm foreclosures and bank failures in the early 1920s. Using a county-specific measure of farm output prices, we show that rising crop prices encouraged entry of new banks and balance sheet expansion of new and previously established banks. The less-regulated, state-chartered banks, as well as those established during the war, were especially aggressive lenders and much more likely to close when the bust occurred. Moreover, deposit insurance amplified the deleterious effects of rising crop prices, whereas higher capital requirements dampened them. We also find that bank closures exacerbated the collapse of farmland values during 1920–25. Thus, our research provides new evidence of how banks can both be affected by and contribute to asset price booms and busts, and how banking policies can influence the feedback loop around such events.

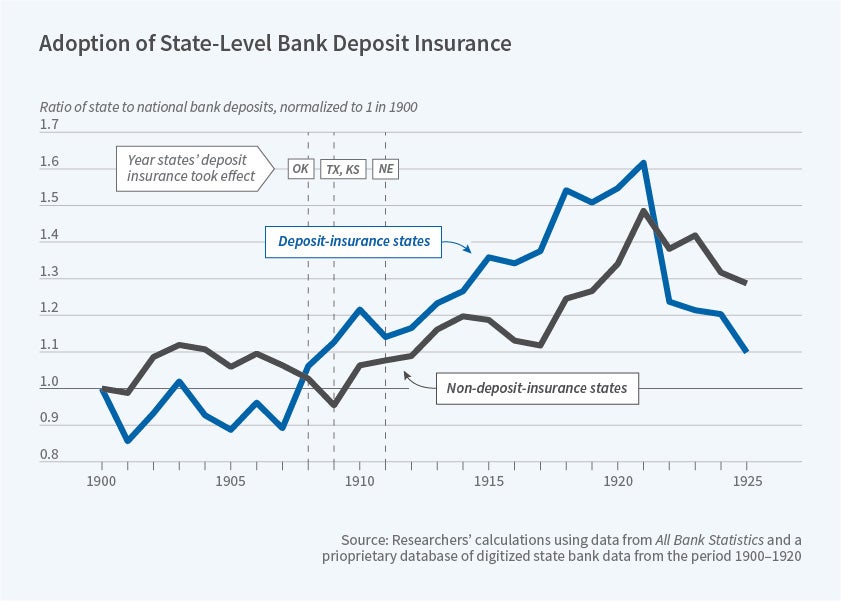

Charles Calomiris and I closely examine the effects of deposit insurance.2 Our findings not only corroborate prior literature on the moral-hazard consequences of deposit insurance, but also show how the introduction of deposit insurance created systemic risk. We find that deposit insurance caused risk to increase by removing the market discipline that had been constraining uninsured banks' decision-making. Depositors applied strict market discipline on uninsured national banks, but supplied funds to insured state banks without requiring those banks to maintain financially sound balance sheets. Figure 1 shows that the ratio of state bank deposits to national bank deposits grew after adoption of deposit insurance, even compared to nearby states. Insured banks as a result increased their loans as well as reduced their cash and capital buffers. Loans increased most strongly in insured banks located in counties where the World War I price rises had the biggest effect, suggesting that deposit insurance might have its most negative consequences when investment opportunities are plentiful.

Interbank Structure and Risk

The interconnected nature of financial networks can propagate shocks, increase systemic risk, and magnify economic downturns. Insights from theoretical studies suggest that the tendency of interbank networks to amplify shocks reflects the relative size of network members, the extent of interconnections between them, and the magnitude of shocks hitting the system, whereas the systemic risk posed by individual institutions depends on heterogeneity in network structure and the concentration of counterparty exposures. Although studies suggest that network structure affects systemic risk, the lack of comprehensive interbank information has prevented much empirical work on how networks evolve and how banks handle interbank shocks. Using data on the entire US interbank network in the early 1900s, I have begun to study how the network evolved and functioned over an important period in US financial history.

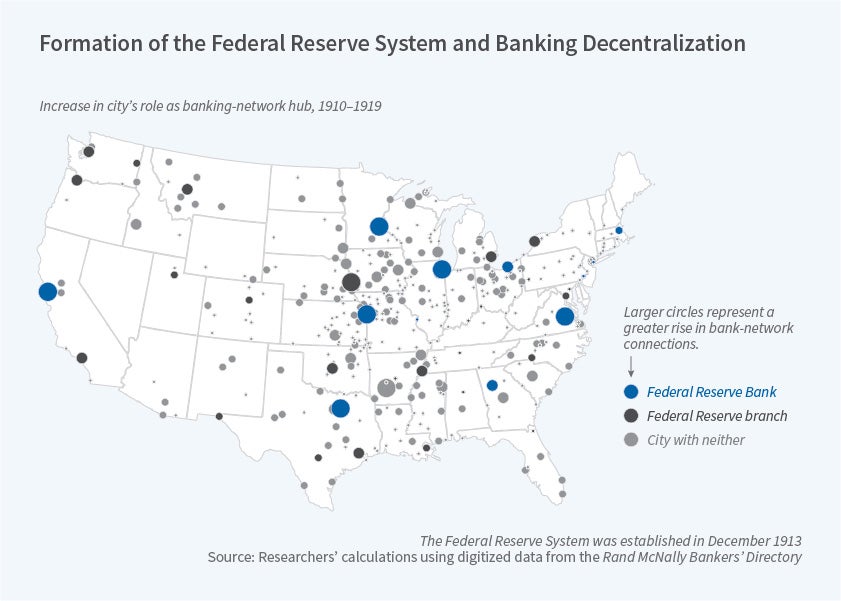

My work with Wheelock finds that the network at the end of the 19th century was pyramidal in structure, with a small number of banks serving as correspondents for a high percentage of the nation's banks. 3 The network became less concentrated after the establishment of the Federal Reserve System in 1914, as banks shifted their interbank relationships away from New York City and toward banks in Fed cities within their local district. As seen in Figure 2, Federal Reserve Bank and branch cities generally had the largest increases in eigenvector centrality (the influence nodes have on networks) in 1910–19. Fitting with my previous study on New York with Calomiris, Haelim Anderson, and Gary Richardson, Fed member banks located in Fed cities across the country were especially favored as correspondents because of their unique access to the Fed's liquidity and payments services, which they were able to pass through to other banks.4 Thus, the Fed's founding changed the relative attractiveness of correspondents in different locations. This reduced network concentration meant that the risk of contagion emanating from a crisis hitting a core city was lessened, but the system remained vulnerable to local and regional panics, and ultimately depended on the Fed to prevent them from spreading across the banking system.

While the Fed's establishment may have reduced the concentration of interbank relationships in certain areas, our follow-up work with Calomiris shows that it might also have led individual banks to become complacent about liquidity risk, and therefore more vulnerable to liquidity shocks.5 Before the Fed was established, greater exposure to interbank deposits encouraged banks to increase their capital ratios. By contrast, the amount of interbank deposits had much less impact on risk-management decisions after the Fed's founding. In essence, the Fed provided a perception of liquidity risk insurance against the sorts of shocks associated with previous banking panics, and in so doing weakened the incentives for banks to guard against interbank liquidity risk.

Knowing that banks had reduced their buffers against interbank liquidity risk, we go on to investigate the role of interbank connections in transmitting shocks during the Great Depression. Specifically, we examine the effects of contagion through direct contractual obligations between individual banks. Controlling for balance sheet characteristics commonly associated with the probability of failure, a bank's probability of closing during the Depression was higher when a higher percentage of its connected banks closed. Closures in one area spread to other areas through interbank connections even when the specific connected bank did not ultimately close. Our results indicate, therefore, that contagion through network ties was a significant source of banking instability during the Great Depression.

Unwinding Quantitative Easing

While most studies have focused on the actions of the Fed during the most recent downturn, the Great Depression offers insight on how to unwind the substantial excess reserves that built up as a result of quantitative easing (QE). Just as in 2007–10, short-term interest rates quickly hit the zero lower bound in the early 1930s and nontraditional monetary policies were considered to stimulate the economy. The net inflows of gold to the United States between May 1934 and December 1941 were more than $14.5 billion, and while gold inflows were not directly controlled by the Fed, the decision not to sterilize gold inflows led to an enormous increase in the monetary base. While we have not yet seen the full unwinding of the current QE program, my work with Gabriel Mathy studies how the United States unwound the monetary expansion of the Great Depression.6

Our analysis indicates that the cessation of the largely exogenous gold inflows is the only factor that can explain the sudden decline in excess reserves in early 1941. Between the trough of the Great Depression in 1933 and the end of World War II, excess reserves fell in only two periods. The first and only temporary decline in early-to-mid 1937 occurred when gold inflows slowed after the gold bloc countries devalued and the Fed raised reserve requirements. Excess reserves quickly rebounded, however, during the recession of 1937–38. The second and more permanent decline in excess reserves started in early 1941 and corresponded to the cessation of gold flows from Europe during the war. Excess reserves were on track to have unwound fully, even without the issuance of war bonds or an increase in reserve requirements in late 1941. Therefore, policy tightening was unnecessary. Instead, by allowing funds to disperse naturally after the gold inflows had ceased, the Fed prevented any large spikes in markets and was able to slowly unwind its QE program.

To conclude, history not only plays a key role in shaping the institutions and markets that exist today, but also enables the study of important dynamics that are sometimes obscured in modern data. Recent research, for instance, has highlighted the relationships between interbank networks, regulation, and financial crises. The literature shows that the concentration of interbank funds in a few institutions can lead to and exacerbate instability. However, the structure of the networks is often shaped by the regulatory and economic environment surrounding the banks. Insights from studies of the Great Depression and other stress episodes where interbank connections are known, therefore, can help in the design of better policies to contain the spillovers associated with counterparty exposures.

Endnotes

"Banking on the Boom, Tripped by the Bust: Banks and the World War I Agricultural Price Shock," Jaremski M, Wheelock D. NBER Working Paper 25159, June 2019. Forthcoming in Journal of Money, Credit, and Banking.

"Stealing Deposits: Deposit Insurance, Risk-Taking and the Removal of Market Discipline in Early 20th Century Banks," Calomiris C, Jaremski M. NBER Working Paper 22692, September 2016, and Journal of Finance 74(2), April 2019, pp. 711–54.

"The Founding of the Federal Reserve, the Great Depression and the Evolution of the U.S. Interbank Network," Jaremski M, Wheelock D. NBER Working Paper 26034, July 2019. Forthcoming in Journal of Economic History.

"Liquidity Risk, Bank Networks, and the Value of Joining the Federal Reserve System," Calomiris C, Jaremski M, Park H, Richardson G. NBER Working Paper 21684, October 2015, and Journal of Money, Credit and Banking 50(1), February 2018, pp. 173–201.

"Interbank Connections, Contagion and Bank Distress in the Great Depression," Calomiris C, Jaremski M, Wheelock D. NBER Working Paper 25897, May 2019.

"How was the Quantitative Easing Program of the 1930s Unwound?" Jaremski M, Mathy G. NBER Working Paper 23788, September 2017, and Explorations in Economic History 69, July 2018, pp. 27–49.