War Bonds, Postwar Inflation, and Voter Sentiment

During World War II, the US government, under Democratic Party leadership, encouraged citizens to invest in savings bonds, and over 85 million Americans subscribed. But high post-war inflation diminished the value of these bonds. The Republican Party criticized Democrats for the poor returns earned by bondholders. Running on a platform that promised to control inflation, the Republicans won the presidency in 1952, ending two decades of Democratic dominance. In Inflation, War Bonds, and the Rise of Republicans in the 1950s (NBER Working Paper 31969), researchers Gillian Brunet, Eric Hilt, and Matthew S. Jaremski examine how ownership of war bonds affected the presidential elections of the 1950s.

In May 1941, the federal government began selling “E bonds” to finance WWII. Bond drives supported by celebrities, government officials, and civil society organizations boosted sales, as did major events like the bombing of Pearl Harbor in December 1941. From 21 percent of households in November 1941, the E-bond ownership rate rose to 65 percent in May 1942 and to nearly 85 percent by 1944.

High inflation between the end of WWII and the start of the Korean War eroded the value of war bonds and enhanced Republicans’ electoral appeal.

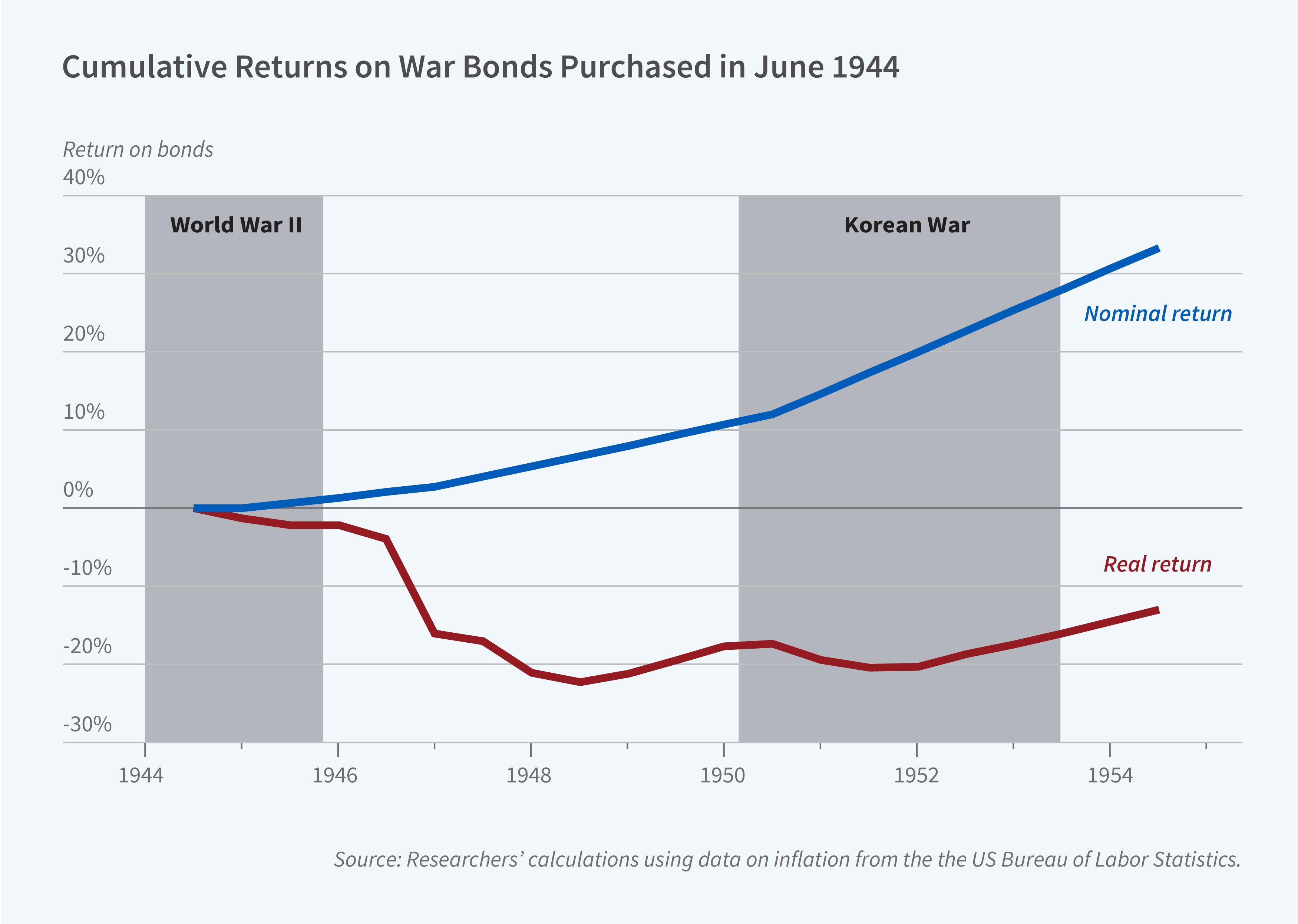

As a result of the high inflation rates in the postwar years and the early 1950s, the real return — the nominal bond return minus inflation — on E bonds held to their maturity at 10 years was negative. For an E bond purchased in June 1944, the cumulative nominal return to maturity was over 30 percent, but the real return was negative 13 percent. The bondholder could not have avoided negative returns by redeeming early. For most redemption dates after 1946, a 1944 E bond’s cumulative real return ranged from negative 16 percent to negative 22 percent.

The marketing campaigns of the drives claimed that E bonds were “The Greatest Investment on Earth,” and presented the public with images of postwar prosperity produced by E bonds’ returns. A 1944 Gallup poll revealed that 91 percent of adults believed E bonds were a good investment. If Consumer Price Index inflation forecasts at that time had been accurate, the cumulative real return on 1944 E bonds at the time of the 1952 election would have been about 10 percent. Instead, unexpectedly severe postwar inflation led to realized real returns of negative 17 percent in 1952. Although E bonds offered better returns than savings accounts, the public felt misled.

Postwar inflation began in 1946, and survey data suggest that voters anticipated mild deflation by the time of the 1948 elections, when Democrat Harry Truman retained the presidency. The outbreak of the Korean War in July 1950, however, saw the onset of another significant wave of inflation. By 1952, inflation had become a prominent issue: 35 percent of survey respondents in August of that year identified it as the country’s most significant problem, up from 8 percent in March 1948. Moreover, households expected that inflation would continue, adding to the appeal of the Republicans’ anti-inflation rhetoric in the 1952 campaign.

The researchers analyze county-level data on E bond subscription rates from 1944. In the 1952 election, a 1 standard deviation increase in E bond purchases per capita in a county — an increase of about $63 per person — was associated with a 1.2 percent increase in the Republican vote share. This finding is largely unaffected by controlling for independent estimates of support for WWII, and the level of bank balances that were available to invest in war bonds.

— Leonardo Vasquez