Disaster Risk and Rising Home Insurance Premiums

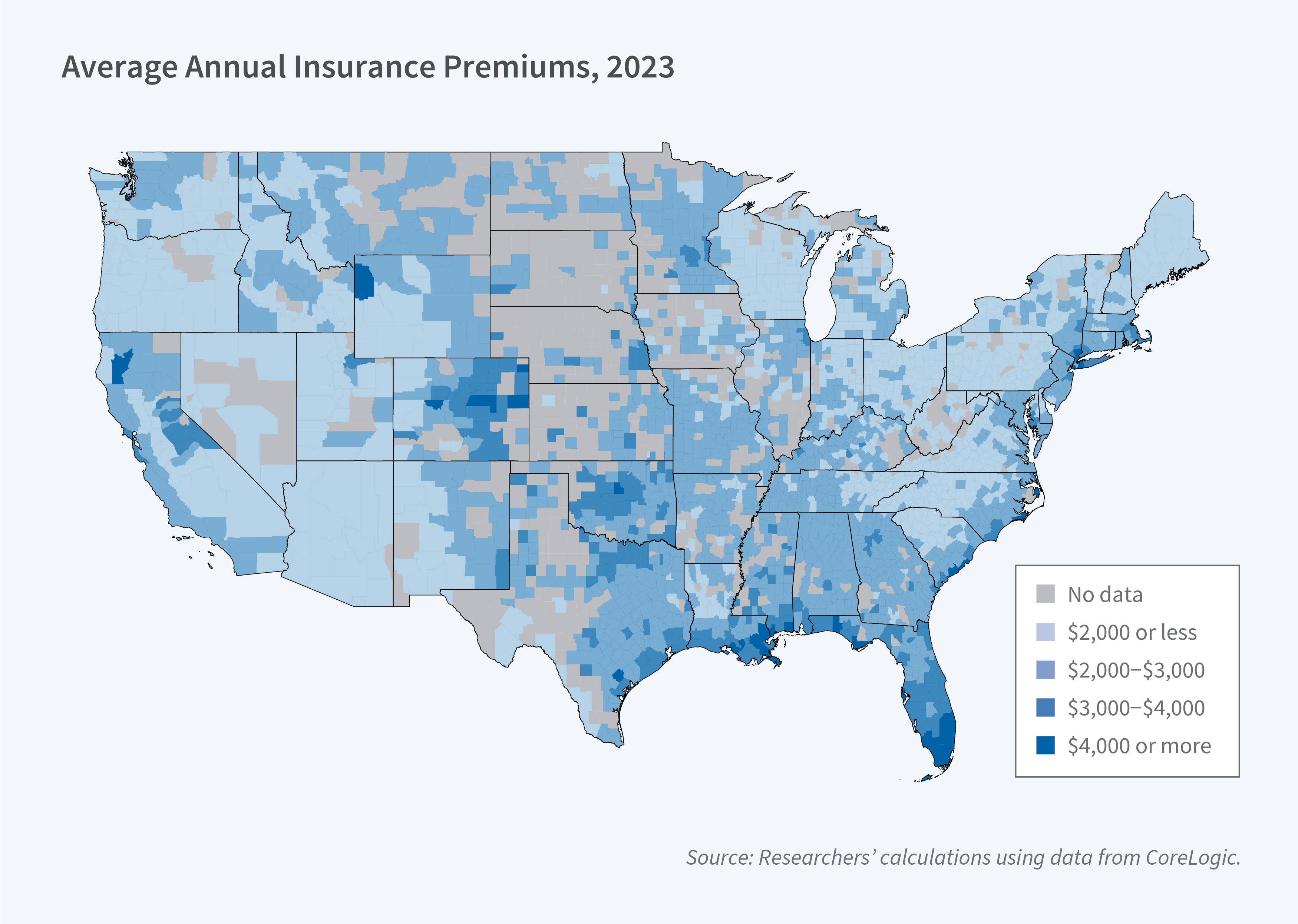

Average property insurance premiums have risen by more than 30 percent since 2020, and there is wide variation by location. Premiums have risen the most for homeowners in areas with the highest risk of natural disasters such as hurricanes or wildfires.

While premiums have always been higher in riskier locations, the relationship between disaster risk and premiums has grown stronger over time. If present trends in the incidence of natural disasters continue, premiums are likely to continue to rise.

The main factor behind the higher prices homeowners face is a rapid rise in reinsurance rates, according to Benjamin J. Keys and Philip Mulder in Property Insurance and Disaster Risk: New Evidence from Mortgage Escrow Data (NBER Working Paper 32579). Insurance companies buy reinsurance to guard against one or more catastrophes wiping out their assets.

The researchers study the drivers of insurance prices by analyzing data on escrow payments. Most mortgage holders make monthly payments to an escrow account that covers the mortgage principal and interest, local property taxes, and homeowners’ insurance. By isolating the insurance piece of those payments, the researchers were able to build a dataset with more than 47 million observations of insurance costs in the US between 2014 and 2023.

Between 2020 and 2023, average home insurance costs rose from $1,902 to $2,530 — a 13 percent rise once adjusted for inflation. But in ZIP codes with the highest disaster risk, the increases were much larger. Neither changes in home values nor changes in state-specific regulations or other factors can account for this finding. In 2018, a 1 standard deviation increase in disaster risk in a ZIP code resulted in an average premium increase of about $300. By 2023, the increase was nearly $500. More than a quarter of the rise in inflation-adjusted homeowners’ insurance costs can be explained by this rise in the risk premium.

The rise in risk premiums coincides with a doubling of US property and casualty reinsurance costs between 2018 and 2023. The researchers call this a “reinsurance shock.” It is the main reason homeowners’ insurance rates are rising, but its effects also vary across locations. Take the border counties between Florida and Georgia along the Atlantic coast, where communities are at equal risk for hurricanes regardless of which side of the state border they are on. In Florida, specialty insurers dominate the residential market and rely on reinsurance to cover nearly 40 percent of the properties in the state. In Georgia, by contrast, national carriers play a bigger role and rely on reinsurers for less than 10 percent of the properties in that state. This may explain why inflation-adjusted premiums in some coastal counties in northeast Florida rose by about $1,000 between 2018 and 2023, while for nearby and similarly situated counties in coastal Georgia, they increased by less than $500.

The researchers observe that rising reinsurance rates could be due to a number of factors, including migration of the US population toward increasingly risky areas, the end of a low-interest-rate environment, and a “climate epiphany” as reinsurers assess their future exposure in light of growing climate risks. They also point out that if extreme weather events become more frequent, the reinsurance shock may continue and strengthen.

—Laurent Belsie

The researchers thank the Wharton ESG Initiative’s Research Fund, ESG Initiative Climate Center, and the Research Sponsors of the Zell/Lurie Real Estate Center for support.