Asset Transfers and End-of-Life Management of Oil and Gas Wells

The US has an estimated 2.1 million abandoned and unplugged oil and gas wells, as well as nearly 1 million still-producing wells. At the end of their productive lives, wells must be sealed through a process known as “plugging” to prevent groundwater contamination, methane emissions, and other environmental hazards. These environmental hazards impose social costs; one federal study valued the social cost of methane emissions from orphaned wells at $1.0 to $2.2 billion per year. Typical plugging costs range from $20,000 to $180,000 per well.

In Cutting Costs or Cutting Corners: Asset Reallocation in Oil and Gas Production (NBER Working Paper 34961), Sarah C. Armitage, Judson Boomhower, and Catherine Hausman investigate how the transfer of oil and gas wells between firms affects production outcomes and environmental remediation. The researchers explore two potential motivations for transfers: productive reallocation, in which smaller firms with lower operating costs can profitably extend a well’s life, and liability shielding, in which well-capitalized firms can avoid end-of-life environmental costs by selling wells to undercapitalized operators who may declare bankruptcy (or otherwise walk away) rather than pay for plugging.

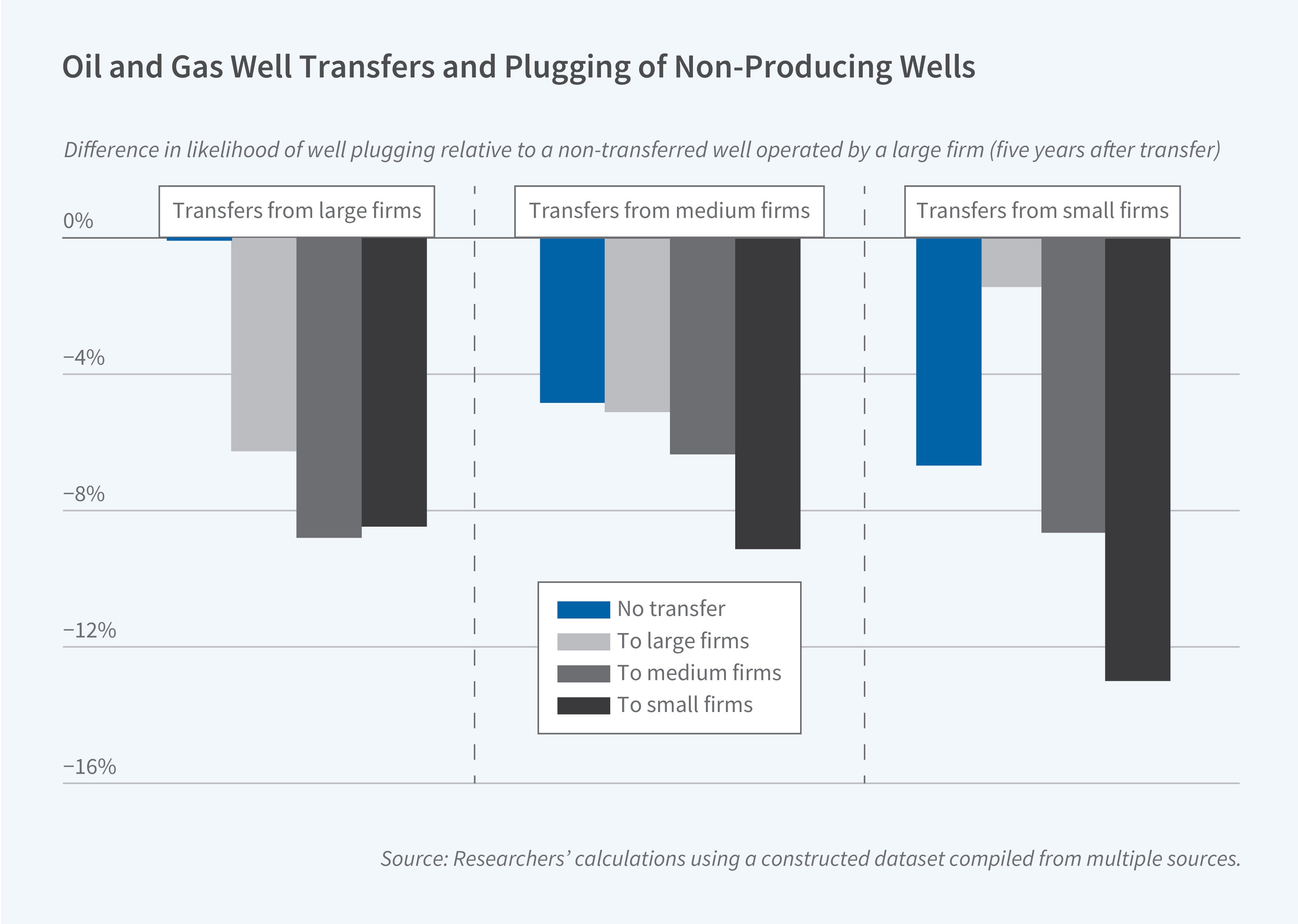

Transferred wells are less likely to be plugged and more likely to generate environmental costs.

The researchers assemble a novel dataset for hundreds of thousands of wells across California, Colorado, Pennsylvania, and Texas from 1992 to 2023. These four states represent roughly 45 percent of US oil and gas production. They find that 8 percent of wells change operators in a typical year, excluding several large corporate mergers, implying that on average a well will be transferred every 13 years. Lower-value wells are transferred more frequently: a well at the 25th percentile of continuation revenue is approximately 2 percentage points more likely to be transferred than a well at the 75th percentile. Low-value wells are disproportionately transferred to low-value firms, with the average transfer of a well below the top quartile of continuation revenue involving a buyer that is smaller than the seller.

Non-producing wells that have been transferred are overall 5 percentage points less likely to have been plugged five years after transfer than wells that have not been transferred. Wells operated by or transferred to small firms are especially unlikely to be plugged. In contrast, the overall production volumes of transferred wells after transfer are similar to those of non-transferred wells. Wells transferred to small firms in particular produce lower volumes but are more likely to remain producing.