Explaining Geographic Disparities in the Commercialization of Academic Research

A significant amount of corporate innovation, including in dynamic industries such as software and biotech, is the direct result of university-based research. Consequently, policymakers around the globe have sought to promote the diffusion and successful commercialization of academic research in the private sector.

In The Wandering Scholars: Understanding the Heterogeneity of University Commercialization (NBER Working Paper 32069), Josh Lerner, Henry Manley, Carolyn Stein, and Heidi Williams examine place-based variation in the commercialization of academic research. It has long been understood that certain universities are particularly productive relative to their peers in moving their research “out of the ivory tower” and into the commercial domain. To what extent are these patterns due to the influence of the school and its environs versus the mixture of faculty who teach at particular universities?

About one-fifth of the geographic variation in the commercialization of academic research is related to differences in the extent to which campuses foster commercialization and the proximity of venture capital.

The researchers seek to unravel this puzzle by studying faculty members who move from one university to another. They find that when faculty move to university environments that foster commercialization, they become more likely to engage in research that leads to such outcomes themselves. Their headline estimates suggest that between 15 and 25 percent of cross-university variation in commercialization rates is due to place-specific factors.

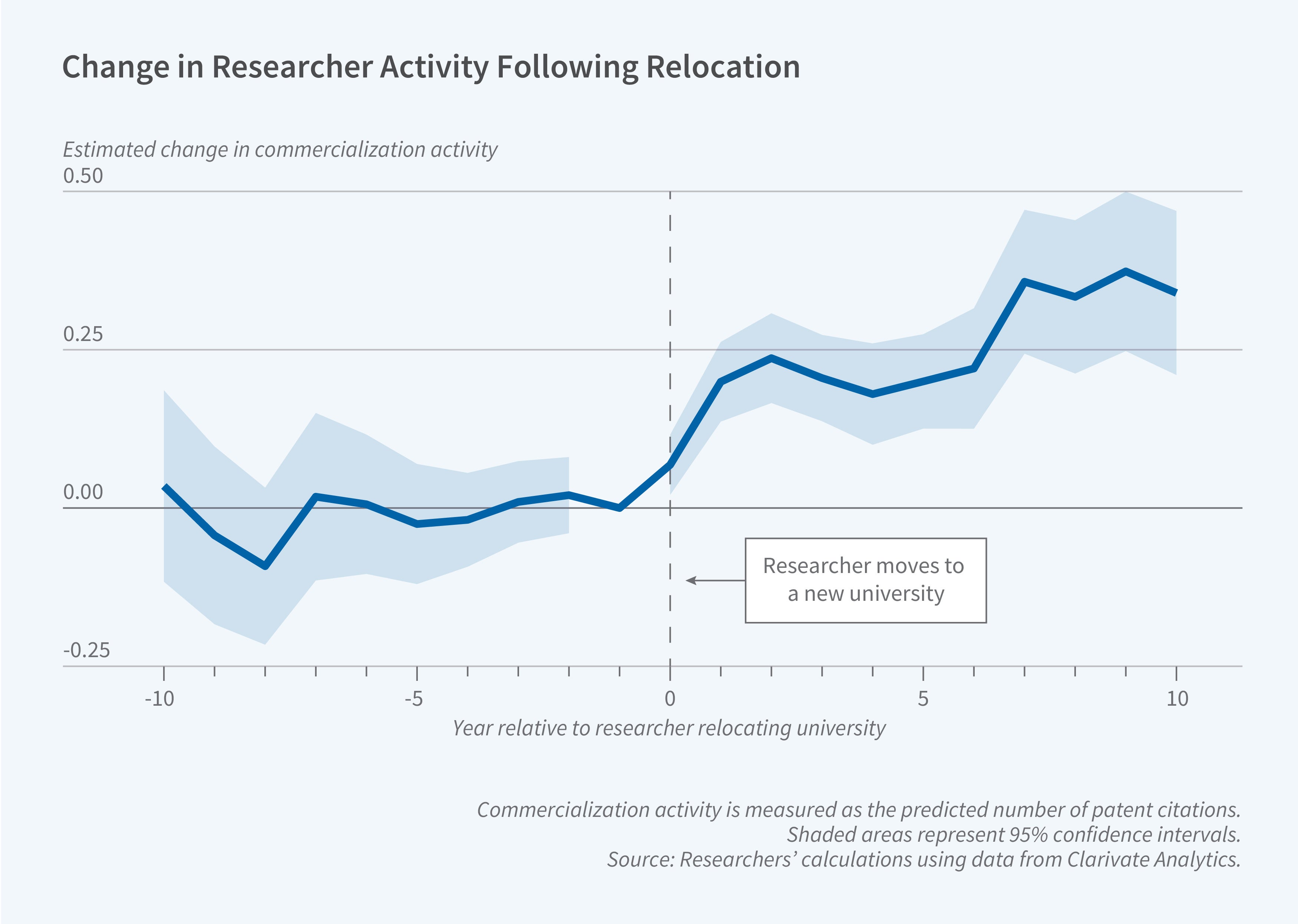

The researchers examine a variety of measures of academic commercialization but focus on citations to academic articles in patent applications. They create a dataset of 14,213 “movers” — researchers that move from one university to another — using email addresses listed on research papers to determine university affiliations. Because the vast majority of patent citations to research papers are in the life sciences, they restrict their set of innovative scholars to biomedical researchers. Then, they estimate an event study model that leverages researcher moves to separately identify the effect of a researcher on commercialization activity versus their institution.

The university fixed effects estimated by their model are of particular interest, as they represent the universities’ commercialization value add. However, the factors which cause the variation in these university effects are not clear, making it difficult to assess which policy levers might be useful in encouraging more commercialization of university research. For example, is it that Stanford has unique proximity to venture capital firms clustered on nearby Sand Hill Road, or that their technology transfer office is particularly efficient in fostering connections between Stanford-based researchers and industry? Or both?

Taken together, the results provide a first step towards decomposing the geographic variation in research commercialization activity and set the stage for future work on harnessing academic science as a force for economic growth.

— Greta Gaffin

This research was funded in part by Harvard Business School's Division of Research and Doctoral Programs, Harvard Economics' SUPER Program, the Alfred P. Sloan Foundation, and the Smith Richardson Foundation. Researcher Lerner has received compensation from advising institutional investors in venture capital funds, venture capital groups, and governments designing policies relevant to innovation and venture capital.

Researcher Williams has received research funding from the Aphorism Foundation, Emergent Ventures, the Institute for Progress, Open Philanthropy, Schmidt Futures, the Smith Richardson Foundation, and the US National Institutes of Health.