Population Aging, Retirement Income Security, and Asset Markets in China

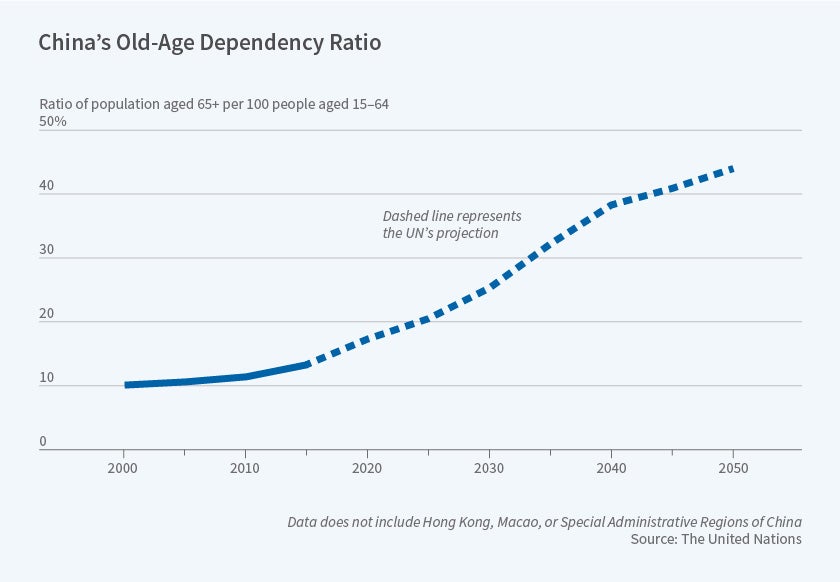

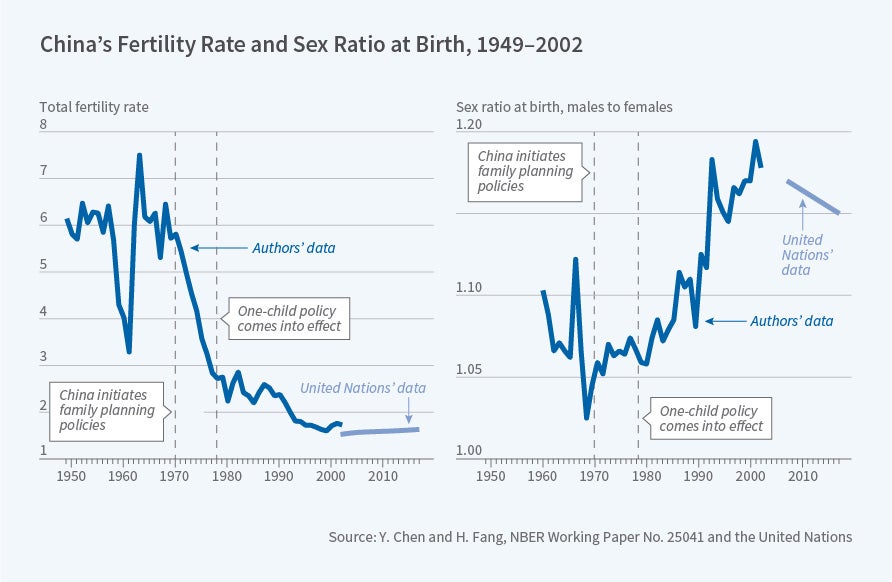

Among the many challenges facing the Chinese economy, population aging is no doubt one of the most important. The old-age dependency ratio in China increased from 10 percent in 2000 to 13 percent in 2015, and is expected to increase to 44 percent by 2050 [Figure 1]. Both increasing life expectancy and declining fertility contributed to China's rapid population aging. Family planning policies, including but not restricted to the one-child policy, have led to a rapid decline in total fertility, from 5.7 in 1969 to 2.7 in 1978, when the one-child policy started, to about 1.6 currently [Figure 2, on the next page]. According to World Bank data, the average life expectancy at birth in China has steadily increased from 57.6 years in 1969 to 65.9 in 1978 to 76.4 in 2017.

Population aging has important implications for China's social insurance programs, retirement income security, and asset markets, including the housing market. In a series of papers, my coauthors and I have studied the impact of population aging in China from a variety of angles.

What is the current status of the Chinese pension system? To the extent that it is inadequate, what are the roles of alternative financial products such as reverse mortgages in providing retirement income for the elderly? What are the consequences of family planning policies on the physical and emotional well-being of the elderly? What are the impacts of population aging on asset markets? What are the likely impediments to and distributional consequences of policies that increase the retirement age?

It should be noted at the outset that population aging is a challenge that almost all industrialized nations face. The elderly face an amalgam of risks about income, health expenditure, long-term care expenditure, and mortality, and at the same time have more-limited income sources than their younger counterparts. In developed economies, the elderly rely on a mixture of self-savings, social insurance programs, and private insurance products to cope with these risks.1 The population-aging challenge China faces is particularly acute for several reasons. First, the trend is accelerated by China's family planning policies since the early 1970s; second, the current social insurance system in China tends to have low and unequal benefit levels; and third, the private insurance markets for the risks the elderly face are not yet well developed.

Family Planning Policies and the Life of the Chinese Elderly

Family planning policies introduced in the early 1970s in China contributed to the population-aging challenges China faces today. It is therefore important to examine how these policies have reshaped the quality of life, including the physical and mental well-being of the Chinese elderly.2 In an effort to curb population growth, China implemented its one child per couple policy nationwide from 1979 to 2015; somewhat less known, however, was the "Later, Longer, Fewer" (LLF) campaign also initiated in the early 1970s. In fact, it was the LLF campaign that started the rapid decline of China's total fertility rate from 5.7 in 1969 to 2.7 in 1978 [Figure 2].3

LLF campaigns offer a valuable opportunity to study how family planning policies affect the life of the Chinese elderly for three reasons. First, in contrast to the one-child policy, the rollout of LLF varied across provinces. Second, LLF policies during the 1970s explain about half of the decline in the fertility rate but, in contrast to the one-child policy, they did not result in an increase in the sex ratio [Figure 2]. Third, the first cohorts affected by LLF are now entering their 60s. Yi Chen and I identify the causal effect of LLF policies from two types of province-level variations. The first is different years for the establishment of Provincial Family Planning Leading Groups, which were in charge of LLF implementation at the provincial level. The second is different profiles of the age-specific fertility rate in 1969 prior to the enforcement of any effective family planning policy.

How family planning affects the quality of life in old age in China is ambiguous. While children historically play critical roles in providing old-age support, the reduction in the number of children does not necessarily reduce the quality of life for seniors, for three reasons. First, having fewer children spares resources that could be redirected to parents themselves. Second, parents can potentially turn to other measures of old-age support — for example, more savings — to substitute for having fewer children. Third, a quantity-quality tradeoff may result in higher transfers from fewer children.

We use data from the China Health and Retirement Longitudinal Study (CHARLS) to examine the long-term consequences of China's family planning policy on a set of outcomes including support from children, consumption, and physical and mental health, for those aged 60 or above.

On children's support for their parents, we consider measures of co-residence, financial or in-kind support, and time transfer, or informal care. Regarding living arrangements, we find no evidence that family planning affects households' decisions regarding co-residency. However, the family planning policies reduce the probability of seniors having children in their village or community by 8.8 percentage points and of having children in their county/district by 7.6 percentage points. The LLF policies also reduce elderly parents' net annual transfers from children by 395.9 RMB (about 18.6 percent of the sample average) and are associated with reduction of children's monthly contacts and visits to parents by 3.08 and 3.00 times per month, respectively.

Despite reduced financial support from children, we find no effect on total household expenditures, though we find evidence that family planning affects the composition of expenditures: Households that are more exposed to LLF policies spend more on food and living expenses and less on health-related expenses.

The most important finding is that family planning has drastically different effects on elderly parents' physical and mental well-being. Using a wide range of health measures, either subjective or objective, we find that family planning has either no effect or a slightly positive effect on elderly parents' physical health status. In contrast, parents who are more exposed to the policies report more severe depression symptoms. The effect is larger for women and rural parents. Three depression symptoms that are most responsive to the policies are: "feel everything they are doing is an effort," "feel lonely," and "feel unhappy." We hypothesize that less interaction with children is an important driving force for these effects.

The Chinese Pension System

In a survey paper, Jin Feng and I provide a detailed account of the current state of the Chinese pension system, as well as its historical development.4

China's pension system is multi-layered. The first layer consists of several public pension pro-grams. Some are mandatory, including Basic Old Age Insurance (BOAI) for employees in for-profit enterprises and Public Employee Pension (PEP) for civil servants and employees in nonprofit government institutions. Some are voluntary, including Urban Resident Pension (URP) and New Rural Resident Pension (NRP), respectively, for urban and rural residents aged 16 and older without a formal non-agricultural job. These pension plans aim to provide basic social security to all residents when they reach old age, regardless of whether they were employed. The second layer consists of employer-sponsored annuity programs, which employers voluntarily provide as a supplement to the public pension programs. The third layer consists of household savings-based annuity insurance policies. First-layer public pension schemes receive substantial direct subsidies from the government, and all plans or products receive tax preferences.

URP and NRP were merged into a uniform Resident Pension system in 2014; PEP was merged into BOAI in 2015, making BOAI the uniform program for all employees in urban sectors. As of the end of 2017, BOAI had 402.9 million participants, of which about 37 million were public sector employees, and the Resident Pension plan had 512.6 million participants. The public pension plans covered 65.8 percent of China's total population, with a total public pension expenditure of 4.032 trillion RMB, about 5 percent of China's GDP. Participation in the second layer was much more limited. Only about 80,000 firms, accounting for less than 0.5 percent of all firms, offered employer-sponsored annuity programs to 23.3 million employees in 2017. The third layer is still in its infancy.

These are the key characteristics of the Chinese pension system:

• The in-system dependency ratio of China's Basic Old Age Insurance system (the ratio of beneficiaries to contributors to the system) is about 38 percent, much higher than the population-wide dependency ratio of 26 percent in 2017. The in-system dependency ratio of the Resident Pension scheme was 43 percent in 2016.

• China has one of the highest statutory pension contribution rates in the world at 28 percent, with 20 percent contribution by the employer, and 8 percent contribution by the employee into a notional individual account with a notional interest rate that currently stands at 8.31 percent.

• The average benefit replacement ratio — pension benefits per pensioner as a percentage of the average wage of workers — has declined steadily and stood at 46 percent in 2017.

• Current retirement ages are 60 for men, 50 for women who work in blue-collar jobs, and 55 for women who work in white-collar jobs. About 93 percent of women are required to retire at age 50.

• This is a fragmented system managed by local governments. Some provinces pool the funds at the provincial level, but most funds are pooled at the city or county level.

• Despite the high statutory contribution rate, the BOAI would have run a fiscal deficit in almost half of the provinces in the absence of government subsidies in 2016.

The Chinese pension system faces many challenges, including weak participation incentives, regional as well as urban/rural disparity in benefits, low benefits, and fiscal unsustainability. Various pension reform proposals are being discussed. One obvious proposal is to raise retirement ages. In on-going research projects, my coauthors and I examine two issues related to this proposal. First, we study its distributional consequences, recognizing that life expectancy differs significantly between blue-collar and white-collar workers. Second, we critically evaluate the presumption that the elderly would be able to find employment if retirement ages were raised, focusing on the potential labor rationing of elderly workers caused by rapid cohort-to-cohort productivity growth and mechanisms for wage compressions.

The Chinese Housing Market

Partly to pave the way for reform of state-owned enterprises (SOEs) prior to China's accession to World Trade Organization, and partly as a response to the adverse effects of the 1997 Asian financial crisis, the Chinese government in 1998 established the real estate sector as a new engine of economic growth. Residential mortgages at subsidized interest rates were introduced by China's central bank, the People's Bank of China (PBC), and between 1998 and 2002, the PBC lowered the mortgage interest rate five times to encourage home purchases. By 2005, China had become the largest residential mortgage market in Asia.

As housing becomes the most important asset for most Chinese households, home-equity release products can play an important role in providing retirement income for the Chinese elderly. To properly assess housing equity appreciation, one needs quality-controlled housing price indices for China.

Quanlin Gu, Wei Xiong, Li-An Zhou, and I undertake this exercise using a comprehensive da-taset of mortgage loans issued by a major Chinese commercial bank from 2003–13.5

We construct housing price indices for 120 major cities in China, using a methodology that can be viewed as an analog of the well-known Case-Shiller index.6 This index is based on comparison of repeat sales of the same homes, but due to the nascent nature of the Chinese market, there are relatively few repeat home sales in the country. However, an important feature of the Chinese housing market is that housing units are typically apartments in large developments; thus, apartment units in the same development that were sold at different months can be thought of the analog of Case-Shiller repeat sales, as the units share similar characteristics and amenities.

Our indices are more reliable than the two widely used official housing price series reported by the National Bureau of Statistics (NBS) of China: the NBS 70-City Index and the NBS Average Price Index. The 70-City Index is remarkably smooth and shows very little real housing price growth in the last decade, while the Average Price Index fails to control for quality, as it does not account for the fact that the newly transacted units in a city are gradually moving to its outer rings, an important factor in rapidly expanding Chinese cities.

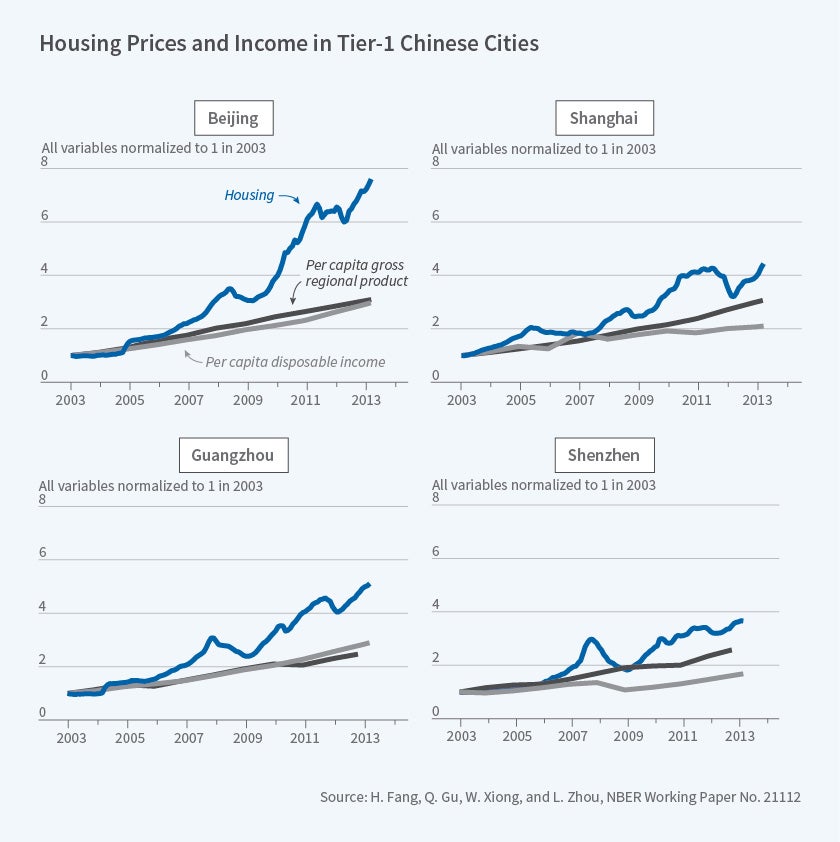

Figures 3 and 4 plot our housing price indices for the four first-tier cities — Beijing, Shanghai, Guangzhou, and Shenzhen — which are the most populous and economically important metropolitan areas in China and the averages of 31 second- and 85 third-tier cities between 2003 and 2013. They confirm enormous housing price appreciation across China. In first-tier cities, housing prices had an average annual real growth rate of 13.1 percent during this decade. Housing prices in second- and third-tier cities had average annual real growth rates of 10.5 percent and 7.9 percent, respectively. These growth rates substantially surpass housing price appreciation during the U.S. housing bubble in the 2000s and are comparable to those during the Japanese housing bubble in the 1980s.

Figures 3 and 4 also show that, while rapid housing price appreciation often has been highlighted as a concern for the Chinese housing market, the price appreciation was accompanied by equally spectacular growth in households' disposable income (DI) and average gross regional product (GRP). The average annual real growth rate was about 9 percent throughout the country during the decade. Simultaneous enormous housing price appreciation and income growth did not occur during the U.S. and Japanese housing bubbles.

Reverse Mortgages as a Source of Insurance and Retirement Income?

China is under tremendous pressure to provide adequate financial resources for its rapidly growing elderly population. Besides considering reform and expansion of the Chinese pension system, private insurance markets also could play an important part in risk mitigation.

Chinese households hold a large proportion of their wealth in the form of housing. Large increases in house prices have led to large increases in household wealth.7

In contrast, other predominant investment vehicles available to the Chinese have had low returns in this period. The real one-year bank deposit rate averaged only 0.01 percent in 2003-2013; the Chinese stock market was still relatively small, with a capitalization of slightly less than 20 trillion RMB in 2013, and the returns were volatile and much lower than those in the housing market. The bond market was even smaller.

Recent surveys find that homeownership rates are high in China, and housing is the largest component of household wealth. In the 2011 CHARLS national baseline, 88 percent of urban residents and 92 percent of rural residents aged 45 or older lived in households owning at least one property. Similarly, the 2012 China Household Finance Survey found that home ownership rates were 88.1 percent and 94.7 percent, respectively, for urban and rural households.8 Housing equity comprised 79–85 percent of total wealth for urban residents and 61–74 percent for rural residents in various surveys. Home ownership rates and housing equity are even higher among older residents. Both the homeownership rate and the fraction of housing in household wealth in China are significantly higher than those in the United States.

How can the elderly access their housing wealth to provide retirement income? Reverse mortgages allow homeowners to borrow against their home without having to make repayments while they still live there. Once the homeowner dies or permanently moves into a nursing home, the home is sold, and the sale proceeds are used to repay the loan.

In 2014, the Chinese government authorized a pilot program to introduce reverse mortgages in China. These loans were initially offered by Happy Life Insurance in four cities for two years. Happy Life now offers reverse mortgages in eight cities: Beijing, Shanghai, Guangzhou, Wuhan, Hangzhou, Dalian, Nanjing, and Suzhou. However, so far the demand for the product has been low: only 139 contracts were underwritten by mid-2018. The reverse mortgage product offered by Happy Life is very complex and inflexible, and the product description is hard to understand.

Katja Hanewald, Hazel Bateman, Shang Wu, and I investigate whether there would be a demand for properly designed and clearly explained reverse mortgages in China.9 We test an improved, more flexible reverse mortgage product design that addresses some of the shortcomings of the unpopular product piloted by Happy Life.

The key innovation of our study is the product design and product description. Our hypothetical product allows borrowers to choose the level of debt as well as the type of payment that best suits their retirement needs. Possible payment types include a lump sum, lifetime fixed regular payments, or flexible payments. In addition, our product explicitly allows the borrowers' heirs to settle the outstanding debt and keep the property at the end of the contract, if they prefer. We also take special care to address potential purchasers' concerns about how house sales will be conducted, whether rental is permitted, and how a loss of the property will be handled. In addition, we make sure to test the subjects' understanding of our reverse mortgage product, which has a simpler debt structure and lower fees than the reverse mortgage offered by Happy Life. We test the demand for this product in two large online surveys, one targeting homeowners aged 45–65 as potential purchasers and the other targeting adult children aged 20–49 who represented the children of potential purchasers. Each survey has 1,100 participants.

We find a high level of interest in reverse mortgages both among older homeowners and the adult children of older homeowners. This result contradicts some widely held perceptions of intergenerational wealth transfer in China. Survey participants want to use the reverse mortgage payments for a range of purposes. Funding a more comfortable retirement and paying for better medical treatments or aged care services are the most important reasons given for interest in the product by both older homeowners and adult children. Consistent with previous literature, we find that product familiarity and product understanding are associated with higher interest in the product. We are currently examining the demand for hybrid reverse mortgage products bundled with long-term care and/or health insurance.

Endnotes

H. Fang, "Insurance Markets for the Elderly," NBER Working Paper No. 20549, October 2014, and published in J. Piggott and A. Woodland, eds., Handbook of Economics of Population Aging, Vol. 1A, Amsterdam, The Netherlands, Elsevier/North Holland Press, 2016, pp. 237–309.

Y. Chen and H. Fang, "The Long-Term Consequences of Having Fewer Children in Old Age: Evidence from China's 'Later, Longer, Fewer' Campaign," NBER Working Paper No. 25041, September 2018.

K. Babiarz, P. Ma, G. Miller, and S. Song, "The Limits (and Human Costs) of Population Policy: Fertility Decline and Sex Selection in China under Mao," NBER Working Paper No. 25130, October 2018, also studied the impact of LLF campaigns on fertility and sex selection.

H. Fang and J. Feng, "The Chinese Pension System," NBER Working Paper No. 25088, September 2018, and forthcoming in M. Armstad, G. Sun, and W. Xiong, Handbook on Chinese Financial Markets, Princeton University Press.

H. Fang, Q. Gu, W. Xiong, and L. Zhou, "Demystifying the Chinese Housing Boom," NBER Working Paper No. 21112, April 2015, and the NBER Macroeconomics Annual, 2015, pp. 105–66. We also answer the following questions: Did the soaring prices make housing out of the reach of typical households? How much financial burden did households face in buying homes?

K. Case and R. Shiller, "Prices of Single-Family Homes Since1970: New Indexes for Four Cities," New England Economic Review, 1, 1987, pp. 45–56.

Ibid, NBER Working Paper No. 21112.

A. Park and Y. Shen, "Understanding wealth and housing inequality among China's older population," China Economic Journal, 8(3), 2015, pp. 288–307; L. Gan, Z. Yin, N. Jia, S. Xu, S. Ma, and L. Zheng, Data You Need to Know About China: Research Report of China Household Finance Survey (2012), Berlin: Springer-Verlag, 2014; and Y. Xie and Y. Jin, "Household Wealth in China," Chinese Sociological Review, 47(3), 2015, pp. 203–29.

K. Hanewald, H. Bateman, H. Fang, and S. Wu, "Is There a Demand for Reverse Mortgages in China? Evidence from Two Online Surveys," NBER Working Paper No. 25491, January 2019.