Convenience Yields: The US Dollar vs. US Treasuries

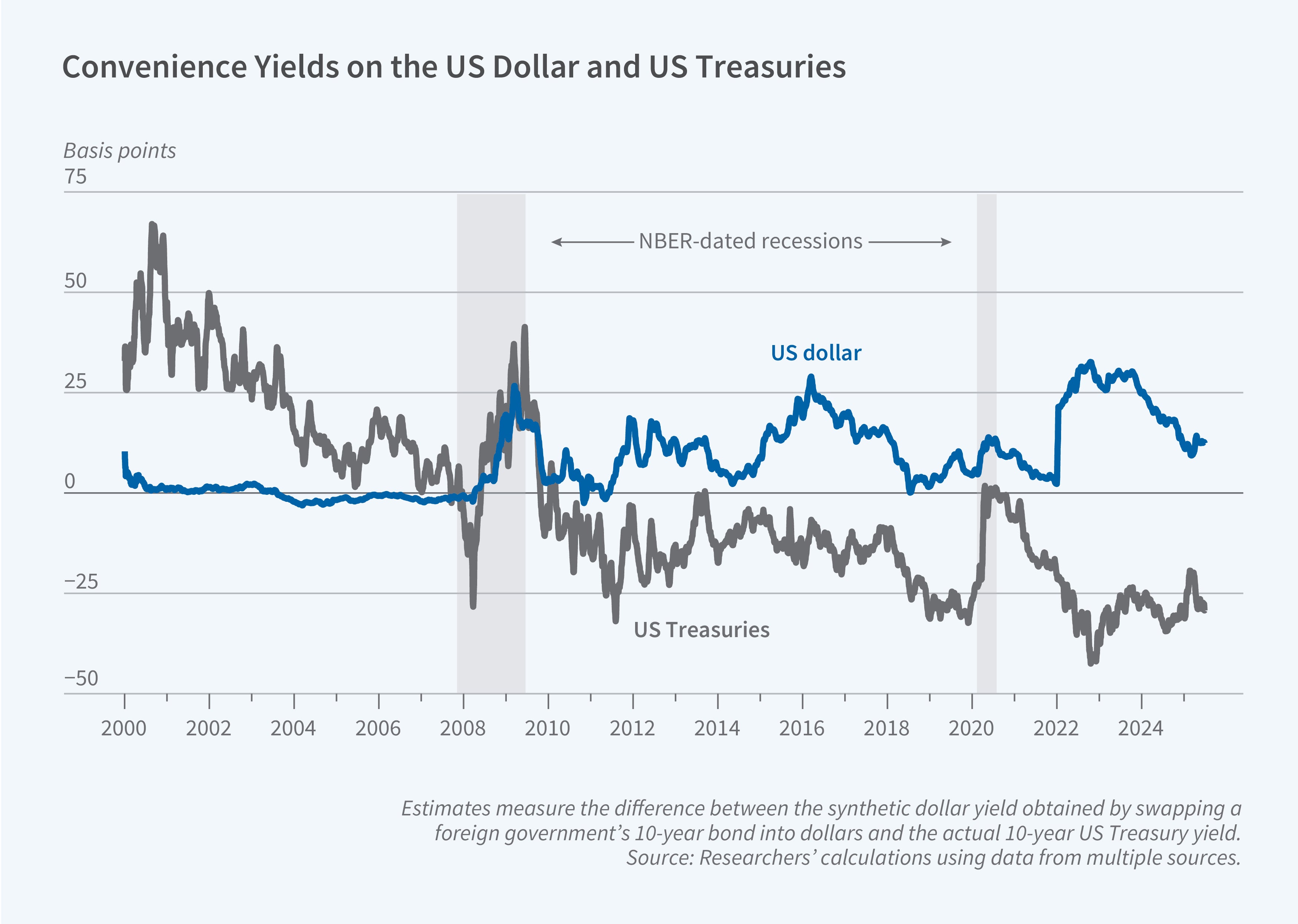

In Decoupling Dollar and Treasury Privilege (NBER Working Paper 35000), Wenxin Du, Ritt Keerati, and Jesse Schreger document a pronounced divergence between the convenience yields on the US dollar and US Treasury securities since the early 2010s. The convenience yield—the premium investors implicitly pay for the safety, liquidity, and collateral value of an asset—has historically been positive for both. While the dollar retains strong convenience in global markets, the convenience yield on Treasuries has declined and turned negative relative to government bonds of other developed economies.

For more than a decade, the dollar has displayed a positive global convenience yield while there has been a negative convenience yield on US Treasuries relative to G10 government bonds.

The researchers measure convenience yields using deviations from covered interest parity (CIP), which stipulates that the cost of borrowing in one currency should equal the cost of borrowing in another after hedging exchange rate risk. They compute CIP deviations for risk-free benchmark rates—capturing dollar convenience—and separately for government bond yields—capturing Treasury convenience—across currencies of the G10 nations and 19 emerging markets at maturities from three months to 30 years.

The median five-year Treasury convenience relative to G10 currencies became negative in 2012 and has declined since then, averaging –26 basis points from 2021 onward compared with –7 basis points during 2012–20. Short-term Treasury convenience yields at three-month and one-year horizons became persistently negative in 2023 and have remained below zero since then. Meanwhile, the dollar convenience yield has remained positive throughout the post–global financial crisis period. It averaged roughly 20 basis points across G10 currencies from 2021 to 2025.

The researchers show that the decoupling of the dollar and Treasury convenience yields is driven primarily by the collapse of US swap spreads—the difference between the interest rate swap rate and the Treasury yield. These spreads have become deeply negative, especially at longer maturities. The risk properties of the two measures have also diverged: while the dollar convenience yield tends to rise during periods of elevated global stress, the Treasury convenience yield has been moving in the opposite direction at medium- and long-term maturities during the 2020s.

A key driver of the Treasury convenience decline is the relative supply of government bonds. Estimates covering 2000–24 show that a 1 percent increase in the US debt-to-GDP ratio is associated with a 0.37 to 0.86 basis point decrease in Treasury convenience, while increases in foreign government debt-to-GDP ratios are associated with higher relative Treasury convenience. The response to the April 2025 reciprocal tariff announcement further illustrates this pattern as the Treasury premium declined most against countries with low government debt burdens, such as Australia, Germany, and Sweden, but barely moved against high-debt countries like the United Kingdom and Japan. The findings suggest that the sheer volume of US government debt issuance has eroded the convenience yield of Treasuries, even as the dollar’s central role in global finance remains intact.