Capital Gains Taxation and Startup Founders

The US capital gains tax is realization based, which means that taxes are due when appreciated assets are sold. Critics of this approach argue that it allows asset holders, such as corporate founders, to defer their tax obligations, sometimes indefinitely. An alternative approach, taxing gains on accrual, would require asset holders to value their assets periodically and to pay tax on the gain since the last valuation. Critics of this approach argue that it could force founders to surrender ownership stakes just to pay tax bills, potentially discouraging startup formation. In Dilution vs. Risk Taking: Capital Gains Taxes and Entrepreneurship (NBER Working Paper 34512), Eduardo M. Azevedo, Florian Scheuer, Kent Smetters, and Min Yang examine how shifting from realization-based to accrual-based capital gains taxation would affect venture-backed startup founders. They emphasize two effects of such a shift from realization- to accrual-based taxation: successful founders face greater ownership dilution from advance tax payments under an accrual-based scheme, while unsuccessful founders receive tax credits that function as partial insurance against downside risk.

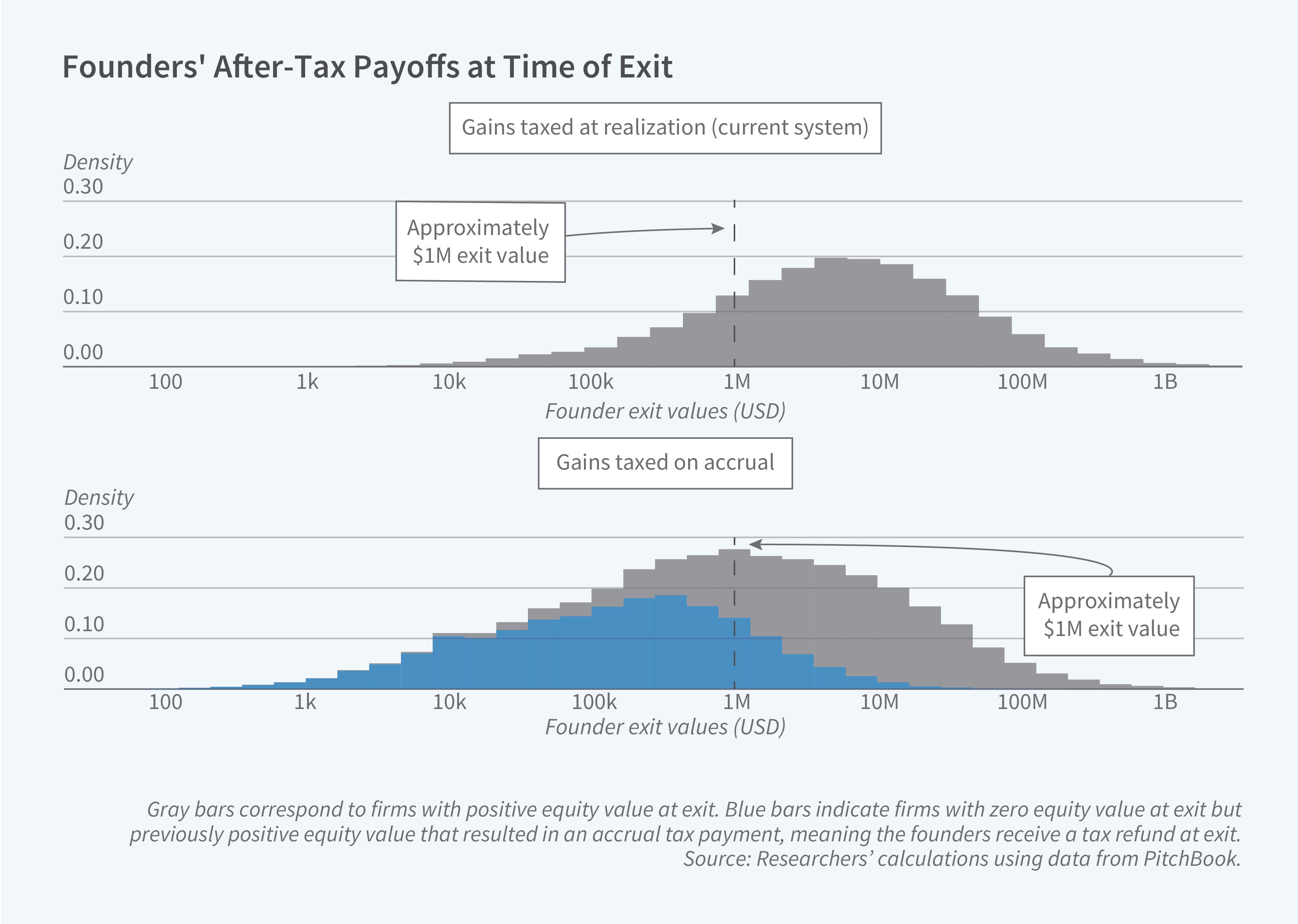

Shifting from realization-based to accrual-based taxation of the gains on founders’ equity would dilute the stakes of those who succeed but also provide some insurance to those who fail.

To evaluate these two effects, the researchers assemble a novel dataset covering approximately 96,000 US venture capital-backed startups, 48,000 exits, 167,000 funding rounds, and 180,000 founders over the years 1987 to 2021. They draw information from SEC filings and financial data providers including PitchBook, CB Insights, PrivCo, S&P Capital IQ, and Compustat. Using deal-level information, they calculate how founder ownership is diluted across successive funding rounds, then feed the resulting payoff distributions into a dynamic career-choice model in which individuals weigh entrepreneurship against salaried employment.

While founders are collectively wiped out in 74 percent of cases, individual dropouts among the remaining successful companies further reduce the pool. Ultimately, only 16 percent of individual founders receive a positive payoff. Among those founders who receive positive returns, outcomes are extreme: the top 2 percent of founders capture 80 percent of total exit value. The average after-tax exit value across all founders is approximately $7.2 million. However, for the 16 percent of founders who do achieve a positive exit, the average payoff is $45.6 million, though the median remains much lower at $5.6 million.

When they simulate a shift to an accrual-based capital gains tax, the researchers find that the average founder ownership at exit falls by roughly 25 percent, and average founder payoffs decline by 15 percent. The payoff for founders in the 99th percentile falls by more than a factor of three under a full accrual system. At the same time, if accrual taxation provided fully refundable tax credits, the share of founders receiving any positive payoff would rise from 16 percent to 47 percent, illustrating the insurance channel.

The researchers also find that a 2 percent annual wealth tax produces comparable dilution to an accrual-based capital gains tax but, unlike the accrual-based tax, provides no insurance benefit through tax credits, meaning the wealth tax unambiguously reduces entrepreneurial incentives.

Florian Scheuer acknowledges support from SNSF Consolidator Grant No. 213673.