The Bottom Line on Hedge Fund Performance Fees

Data on 5,917 hedge funds over 22 years suggest that after incentive fees and management fees are assessed, investors received only 36 cents of every dollar earned on invested capital.

The hedge fund industry prides itself on its incentive compensation structure, which provides tight alignment of fund managers’ and investors’ incentives. Specifically, managers should receive performance fees only when investors make money. Accordingly, managers’ compensation is composed of both an annual management fee and an incentive fee. The former typically ranges between 1 and 2 percent of assets under management, while the latter is often about 20 percent of earned gains. Incentive fees accrue only on gains that exceed a minimum hurdle rate — a risk-free rate — and exceed a previous high valuation. This way, investors pay incentive fees only on “new” gains.

In reality, the relationship between long-term hedge fund performance and incentive fees is significantly distorted. In The Performance of Hedge Fund Performance Fees (NBER Working Paper 27454) Itzhak Ben-David, Justin Birru, and Andrea Rossi use data on a sample of 5,917 hedge funds from 1995 to 2016 to investigate how hedge fund incentive contracts perform in practice. They find that while the average contractual incentive fee in the sample is 19 percent, managers collected 49.6 percent of funds’ cumulative gross profits above the hurdle rate as incentive fees. Inclusive of management fees, fund managers collected 64 cents of every dollar earned, net of riskless returns, on invested capital, while investors took home 36 cents. The high share of returns paid to managers stems from asymmetries in the performance contract, investors’ return-chasing behavior, and closures of underwater funds.

The gap between the nominal incentive fee rate of 19 percent and the effective rate of 49.6 percent can be traced to the fee contract’s asymmetric nature. The researchers identify three mechanisms at play. First, since investors pay fees at the fund level, they cannot offset losses in one fund against gains in another. Therefore, losing funds reduce investors’ total profits, but not the incentive fees collected by managers. Second, investors pay fees as funds generate gains, but do not receive these fees back when funds experience losses in future years. Furthermore, many investors chase returns, meaning that they tend to withdraw capital after losses. Third, funds with consistent losses tend to liquidate, and when that happens, incentive fees paid on earlier gains are not refunded to investors.

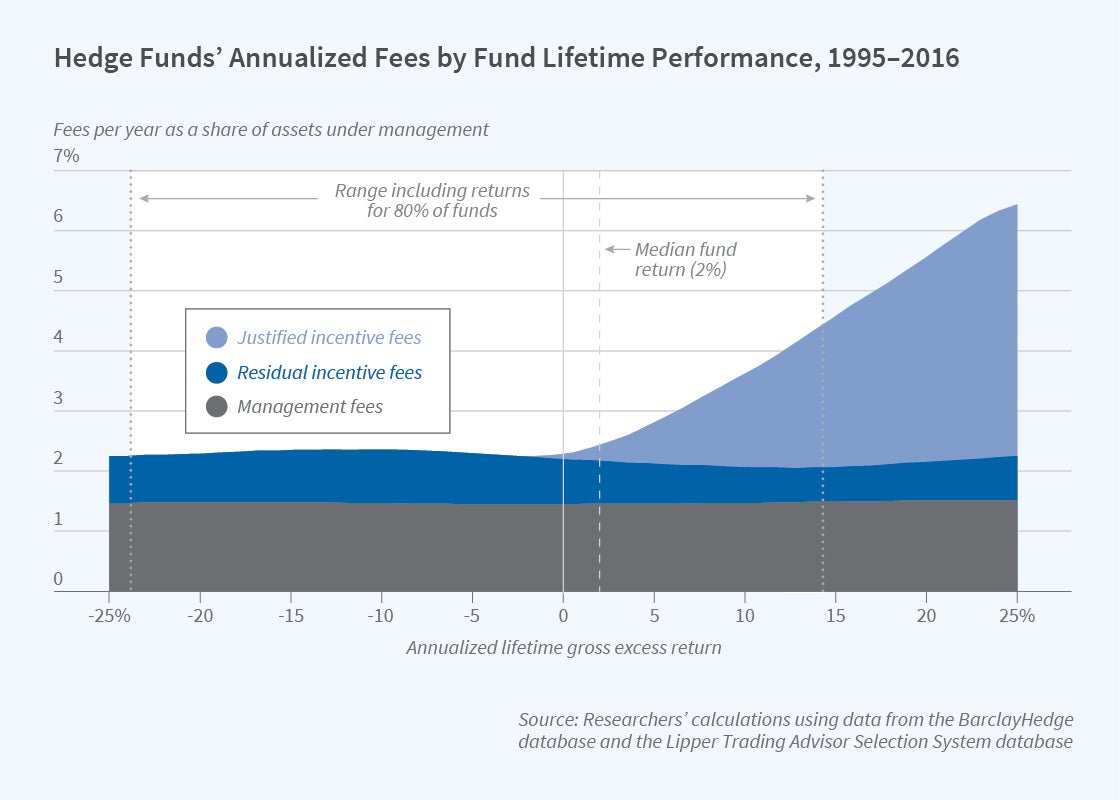

The researchers split the incentive fees paid to managers into fees earned on lifetime profits (“justified fees”) and incentive fees that were paid on gains that were offset by later losses (“residual fees”). In aggregate across funds, residual fees amount to 1.19 percent of assets under management per year. Moreover, residual fees are evenly distributed across funds’ performance spectrum, as shown in the figure.

Over the 22 years studied, the capital invested in the hedge funds in the sample earned gross profits of $228 billion. Hedge fund managers collected incentive fees of $133 billion, out of which $70 billion were residual fees. Extrapolating to the entire hedge fund industry over that period, the researchers estimate that the residual fees amounted to $194 billion. They conclude that “the prevailing hedge fund compensation structure fails to protect investors from paying fees to fund managers that perform poorly in the long run” and that higher incentive fees may not ensure a tighter link between fees and fund performance.

— Linda Gorman