Cross-Country Differences in Exchange Rate Effects on Inflation

When a large fraction of a country's trade is denominated in foreign currencies, its rate of inflation is more strongly affected by exchange-rate fluctuations.

Exchange rates, which give the price of a country's currency relative to foreign currencies, fluctuate based on global market dynamics. These fluctuations can affect domestic inflation rates. For example, if the U.S. dollar depreciates, imported goods generally become more expensive, and the prices of domestically produced goods may also rise as domestic producers face weaker competition from abroad.

In The International Price System (NBER Working Paper 21646), Gita Gopinath argues that the relationship between exchange-rate fluctuations and inflation varies considerably from country to country. Analyzing data from 46 developed and developing nations, she finds that which currency is used to set international prices has large, asymmetric effects on whether exchange-rate fluctuations pass through to domestic prices.

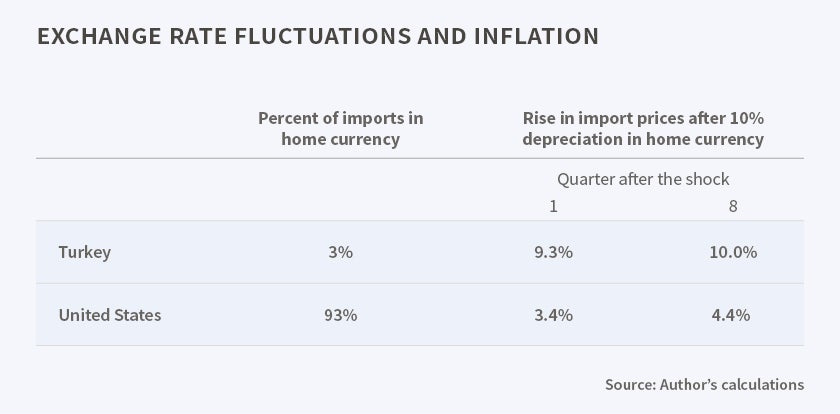

Gopinath's principal finding is that when a large fraction of a country's trade is denominated in foreign currencies, its rate of inflation will be more strongly affected by exchange-rate fluctuations. As an example, Turkey invoices just three percent of its imports in Turkish lira. When the lira depreciates by 10 percent relative to the currencies of Turkey's trading partners, Gopinath calculates, import prices measured in lira rise by 9.3 percent after one quarter and 10 percent after two years, meaning that the exchange-rate fluctuation is fully passed through to prices. In contrast, the United States invoices 93 percent of its imports in U.S. dollars. When the dollar depreciates by 10 percent, import prices measured in dollars rise by only 3.4 percent after one quarter and 4.4 percent after two years.

This incomplete pass-through rate has important benefits for the U.S. economy. In particular, it implies that the U.S. inflation rate is relatively immune to the monetary policy of the rest of the world. If Turkey tightens its monetary policy, this will affect the exchange rate between the U.S. and Turkey, but will not have much effect on U.S. inflation. However, if the U.S. tightens monetary policy, the resulting appreciation of the dollar will tend to inflate prices in Turkey, as 60 percent of Turkish imports are denominated in dollars.

Gopinath shows that, like the overall basket of Turkish imports, the subset of U.S. imports that is priced in foreign currencies also has a high pass-through rate. Of course, this would happen mechanically if prices did not adjust. But, importantly, it also holds for goods for which prices change after an exchange rate shock.

Gopinath argues that the strong effects of currency denomination arise because it is costly for firms to adjust prices. She shows that if it were costless to adjust prices, currency denomination would be irrelevant. When there are costs to renegotiating prices, however, exporting firms' choice of currency denomination will depend on their own cost composition and on the currency choices of other exporters. If most other exporters price in dollars, then a firm will be better able to control its relative price in the market if it also prices in dollars. The findings suggest that absent coordinated international action, the dollar is likely to remain the dominant currency of international trade for the foreseeable future.

—Andrew Whitten