The Dollar’s Evolving Role in International Bond Markets

International debt securities (IDS)—bonds issued, listed, or governed outside the issuer’s home country—had a total value of $2 billion in 1970 but grew to $30 trillion by 2024. While the dollar has been the largest denomination currency for IDS since 2000, its dominance has fluctuated considerably, even as possible alternatives like the euro, created in 1999, and the Chinese renminbi, whose internationalization began in 2010, have emerged. In Dollarization Waves: New Evidence from a Comprehensive International Bond Database (NBER Working Paper 34942), Swapan-Kumar Pradhan, Eswar S. Prasad, Előd Takáts, and Judit Temesvary use a dataset compiled by the Bank for International Settlements to examine how the dollar’s prominence in IDS has varied since the 1960s.

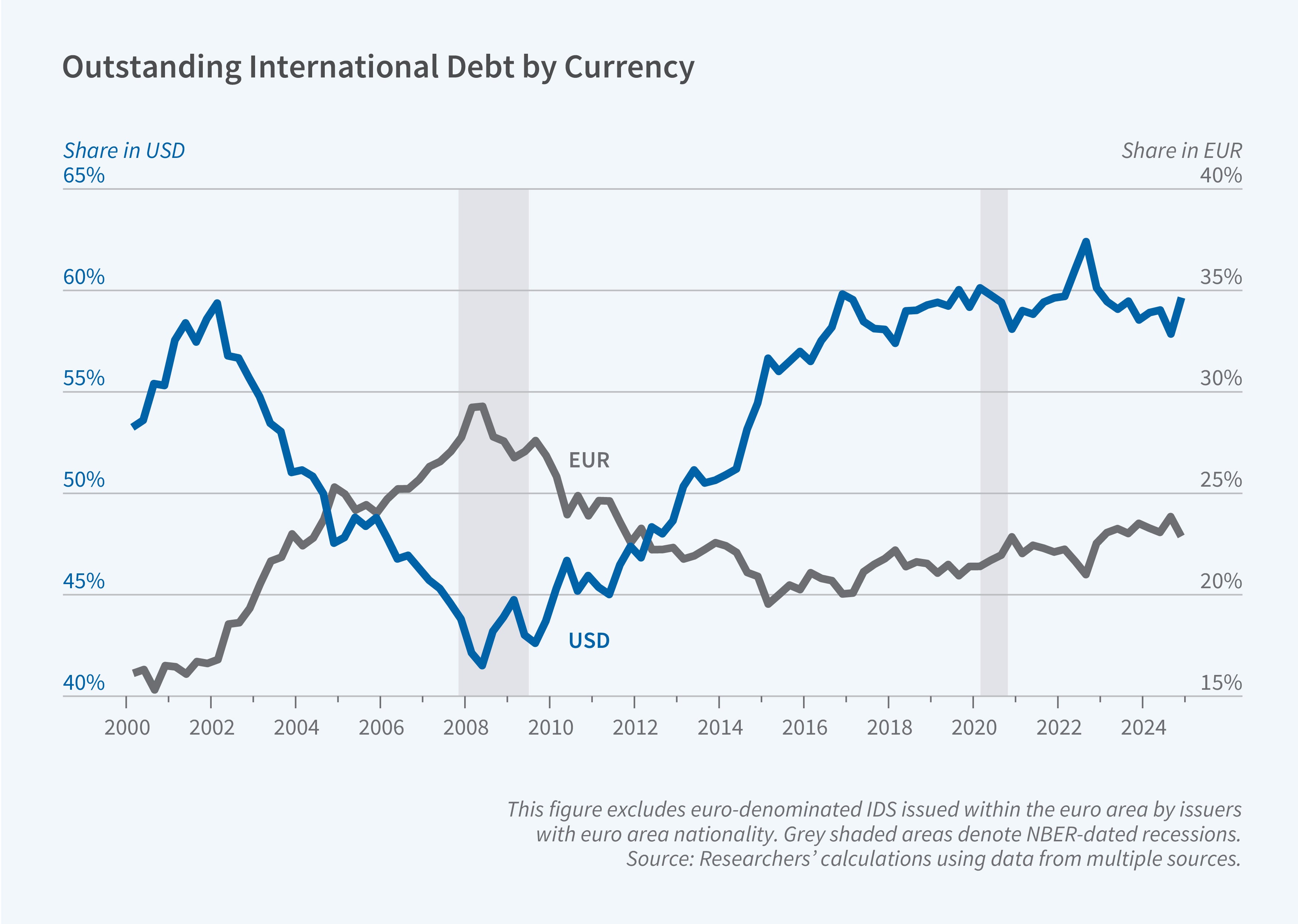

The currency denomination of international debt securities has fluctuated over the last six decades, with the dollar’s share in 2024 close to where it stood in the early 2000s.

The dollar’s share of IDS does not display a uniform trend. Instead, it has ebbed and flowed. In this century, the dollar’s share of outstanding IDS fell from roughly 60 percent in the early 2000s to about 43 percent around 2008, then surged back to approximately 60 percent by the latter half of the 2010s. Earlier data, starting in 1966, reveals two prior waves, with the dollar’s share rising in the early 1980s and again in the late 1990s before declining after each peak. The dollar’s share in 2024 is similar to what it was in both the early 1970s and the early 2000s.

The euro experienced a notable rise after its creation in 1999, with euro-denominated new issuance nearly matching dollar issuance in the years preceding the global financial crisis (GFC). However, the euro’s share subsequently declined as euro-denominated issuance by banks and nonbank financial institutions was pulled back after the crisis. By 2024, the euro’s share remained higher than at its introduction but well below its pre-GFC peak. The Japanese yen and Swiss franc have experienced declining IDS shares, while the Chinese renminbi’s share has risen modestly since the GFC from near zero to rival the yen’s share by 2024. Holding exchange rates constant at their 2000 levels smooths the fluctuations in the dollar share but does not eliminate them.

Alignment between a country’s domestic currency and a reserve currency is a strong predictor of denomination patterns. A 1 percentage point increase in a country’s dollar currency zone alignment is associated with an average 0.13 percentage point increase in the dollar’s share of that country’s new IDS issuance. Higher domestic policy rates correlate with greater dollar denomination, while higher US Treasury yields—reflecting increased dollar funding costs—are negatively associated with the dollar’s share.

Heightened geopolitical risk in an issuer’s home country leads public sector issuers to increase dollar-denominated issuance. The exception is US-based issuers, for whom rising domestic geopolitical risk is associated with diversifying away from the dollar and toward the euro.