Banks vs. Private Credit Funds: A Balance-Sheet Comparison

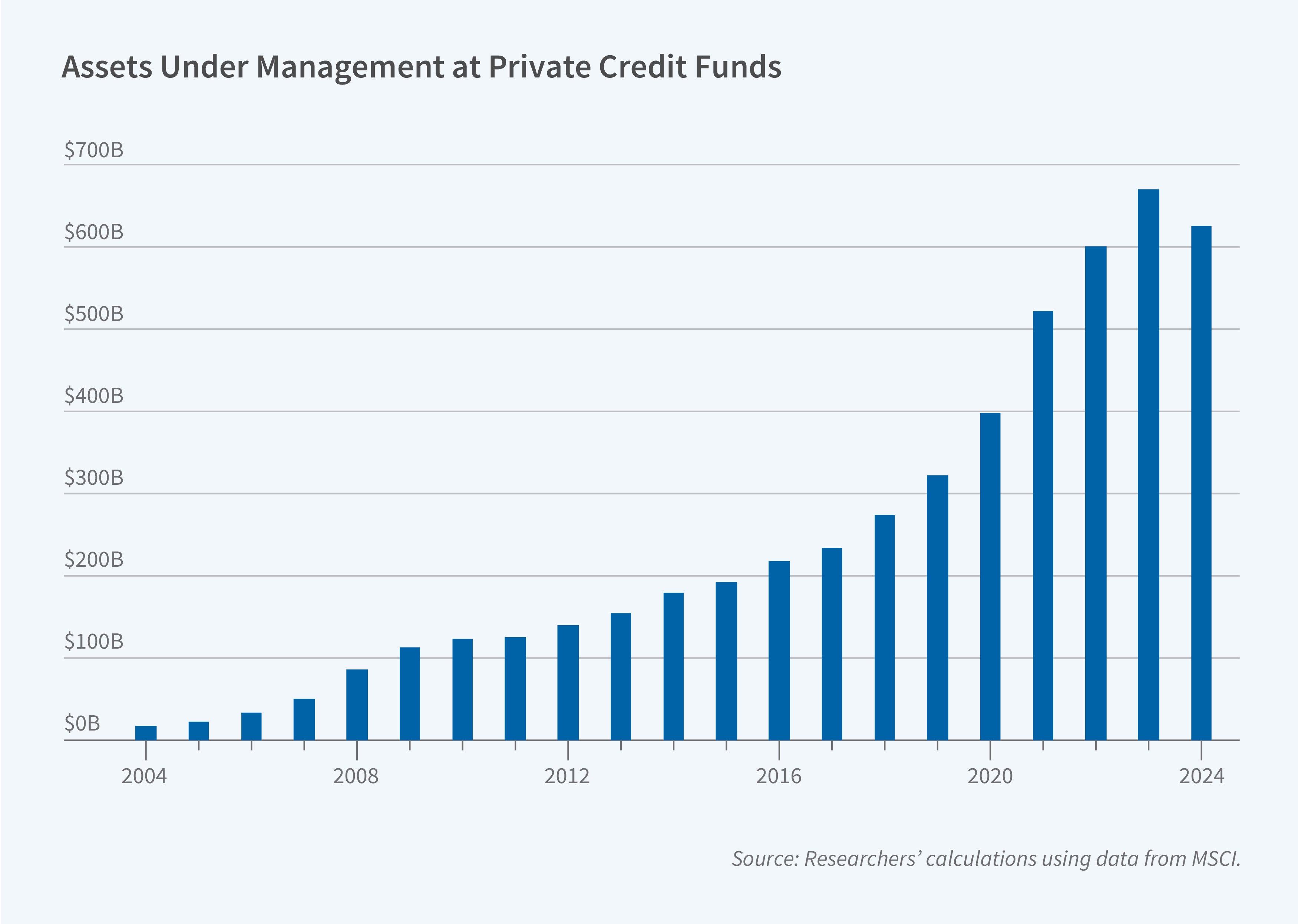

Recent decades have seen corporate lending shift away from traditional banks and toward private credit funds. The latter are investment vehicles structured as limited partnerships that extend loans to businesses, often middle-market firms without easy access to conventional financing. Assets in the private credit sector have grown from under $10 billion in the early 2000s to more than $1 trillion in 2024. Along with this growth, there have been rising concerns that private credit may replicate the fragilities historically associated with banking: high leverage, maturity mismatch, opacity, and interconnectedness with the broader financial system.

In Private Credit, Balance Sheets and Financial Stability (NBER Working Paper 34991), Gregor Matvos, Tomasz Piskorski, and Amit Seru examine whether these concerns are supported by the structure of private credit funds’ balance sheets. Their analysis draws on the MSCI Private Capital Universe, a proprietary dataset covering approximately 1,300 funds and nearly 9,000 individual loan holdings from 2000 to 2024, representing roughly 65 percent of US private credit activity. They compare the capitalization, funding structure, maturity alignment, and performance of these funds to comparable measures for US commercial banks.

Equity typically accounts for between 65 and 80 percent of the financial structure of private credit funds, compared with approximately 10 percent of the capital structure for US commercial banks. Banks thus operate with much more leverage. The equity-to-assets ratio across all funds averages 0.85, with an asset-weighted mean of 0.79, indicating that larger and smaller funds display similar leverage. Even among funds that report active use of bank credit lines, about two-thirds of assets remain equity financed. These credit lines, primarily provided by commercial banks, function as liquidity management tools to bridge capital calls and smooth transaction timing rather than as sources of persistent leverage.

Private credit funds exhibit little or no maturity mismatch—a structural vulnerability that has been central to banking crises from the Great Depression through 2008. Funds typically have a lifetime of about 10 years, while the underlying loans they hold mature in approximately five years on average. Asset cash flows therefore arrive well before the fund winds down. This contrasts sharply with banks, which finance long-duration assets with short-term deposits that can be withdrawn on demand.

Private credit portfolios are broadly diversified. Asset-level data covering $477 billion in holdings show that financials account for 20.6 percent of total assets, followed by industrials at 15.4 percent and healthcare at 12.4 percent. Although New York, Texas, and California together represent about one-quarter of private credit exposure, the remaining loans are distributed across numerous states. This diversification limits the sector’s vulnerability to idiosyncratic, sector-specific shocks.

Realized performance data indicate that downside risk is largely absorbed by equity investors rather than creditors. Across 1,267 funds, mean annualized net returns to limited partners are 9.6 percent, with a median of 9.1 percent. Extreme losses are rare; the 5th percentile return is approximately –3.8 percent. Results for fully exited funds are broadly similar, with mean returns of 9.9 percent, suggesting that these patterns are not primarily driven by valuation smoothing in active portfolios.

The researchers note that most of the private credit sector’s expansion has occurred during relatively benign credit conditions, so its resilience under severe macroeconomic stress remains untested. They also identify a number of potential sources of future fragility, including competitive pressures that could lead to higher leverage and looser underwriting over time, expanding bank-nonbank linkages during economic downturns, transparency, and the risk that losses of limited partners, many of whom invest in multiple funds, could result in correlated portfolio adjustments and tightening of overall credit supply. A related set of questions concerns governance, control rights, and monitoring in private credit. In this context, stressed conditions could trigger “valuation contagion,” where uncertainty about asset values spills over into fundraising, secondary markets, or affiliated vehicles, potentially contracting credit to affected firms.

The researchers acknowledge support from the Private Equity Research Consortium, the Institute for Private Capital, and MSCI.