Long-Run Evolution of the Size Distribution of Businesses

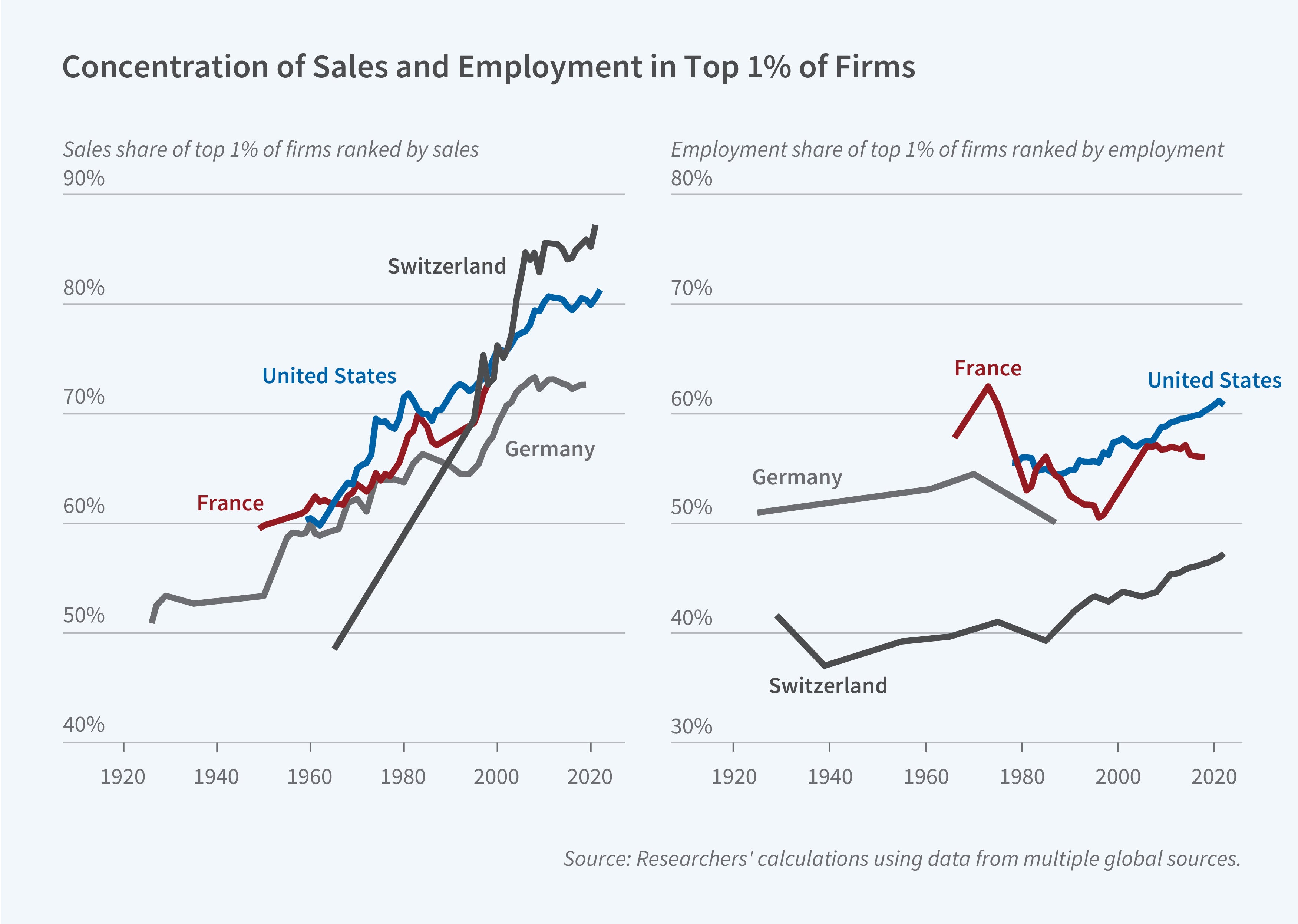

In Business Concentration Around the World: 1900–2020 (NBER Working Paper 34711), Yueran Ma, Mengdi Zhang, and Kaspar Zimmermann analyze data on firm size distributions in 10 advanced market economies in Asia, Europe, North America, and Oceania. They find that sales, net income, and equity capital have become increasingly concentrated in the largest firms. The top 1 percent of firms by sales now account for around 80 percent of economy-wide sales in many countries, up from around 50 percent in the early twentieth century. Employment concentration has nevertheless remained relatively stable, with the largest 1 percent of firms by number of employees accounting for roughly half of economy-wide employment throughout this period.

The concentration of sales, income, and capital among the largest firms has risen worldwide, while the concentration of employment has been stable.

The sales share of the top 1 percent of firms rose from around 50 percent in the 1950s and 1960s to between 70 and 80 percent by the 2010s in most countries with available data. The net income share of the top 1 percent in Australia and Canada increased from between 40 and 50 percent in the 1940s to around 60 percent by the 1970s and 1980s and 80 percent by 2000 in Australia (Canadian data end in 1987). For equity capital, in Germany, Denmark, and Switzerland, the top 1 percent share grew from around 40 percent in the early 1900s to 60 percent or more by the 1980s. The trends of rising business concentration hold at the industry as well as the national level.

In contrast, employment concentration remained largely stable over the period of study. The top 1 percent of firms by employment accounted for roughly 50 percent of economy-wide employment throughout the twentieth century in most countries in the sample. In manufacturing, employment concentration showed little long-run change. However, in retail and wholesale trade, employment concentration increased substantially, with magnitudes comparable to the rise in sales concentration.

Standard production functions with complementarity between capital and labor would predict the concentration of sales, capital, and employment to move together. The researchers suggest that automation—with large firms increasingly substituting capital for labor—may explain the divergence of employment concentration, particularly in manufacturing where capital-to-labor ratios have increased substantially more than in retail and wholesale trade. The pervasiveness of rising concentration across diverse countries and time periods suggests that broad-based economic forces rather than country-specific policies or demographics are important for understanding these fundamental shifts in production organization.

The researchers acknowledge support through the NSF CAREER award.