Fund Flows, Returns, and Mutual Fund Managers’ Pay

Actively managed mutual funds, which pool money from many investors and invest it in stocks, bonds, and other financial assets, are an important part of the US financial system. About half of US households invest part of their savings in mutual funds. Some are actively managed; others follow a passive index–style investing approach. In 2016, mutual and pension funds held around 44 percent of the US equity market. Managers of actively managed funds make frequent trading and investment decisions that have important ramifications for the savings or pensions of invested households.

Despite the scale and importance of these funds’ activities, the incentives facing fund managers are poorly understood, mainly due to a lack of data on managers’ compensation. Designers of compensation structures for fund managers face the classic problem of aligning the incentives of the “agent” — in this case the fund’s manager — with the interests of the “principal” — the fund’s investors.

In Fund Flows and Income Risk of Fund Managers (NBER Working Paper 31986), Xiao Cen, Winston Wei Dou, Leonid Kogan, and Wei Wu construct a dataset covering the compensation and employment histories of managers at actively managed US equity mutual funds. They use it to study the determinants of fund managers’ compensation and career outcomes. They extract fund managers’ names from the databases of the Center for Research in Security Prices and Morningstar, and from LinkedIn, fund prospectuses, and fund websites. They then use managers’ names to find other pieces of identifying information, which in turn enables the linking of managers to observations in the Longitudinal Employer-Household Dynamics dataset of the US Census Bureau, which contains information about compensation and employment.

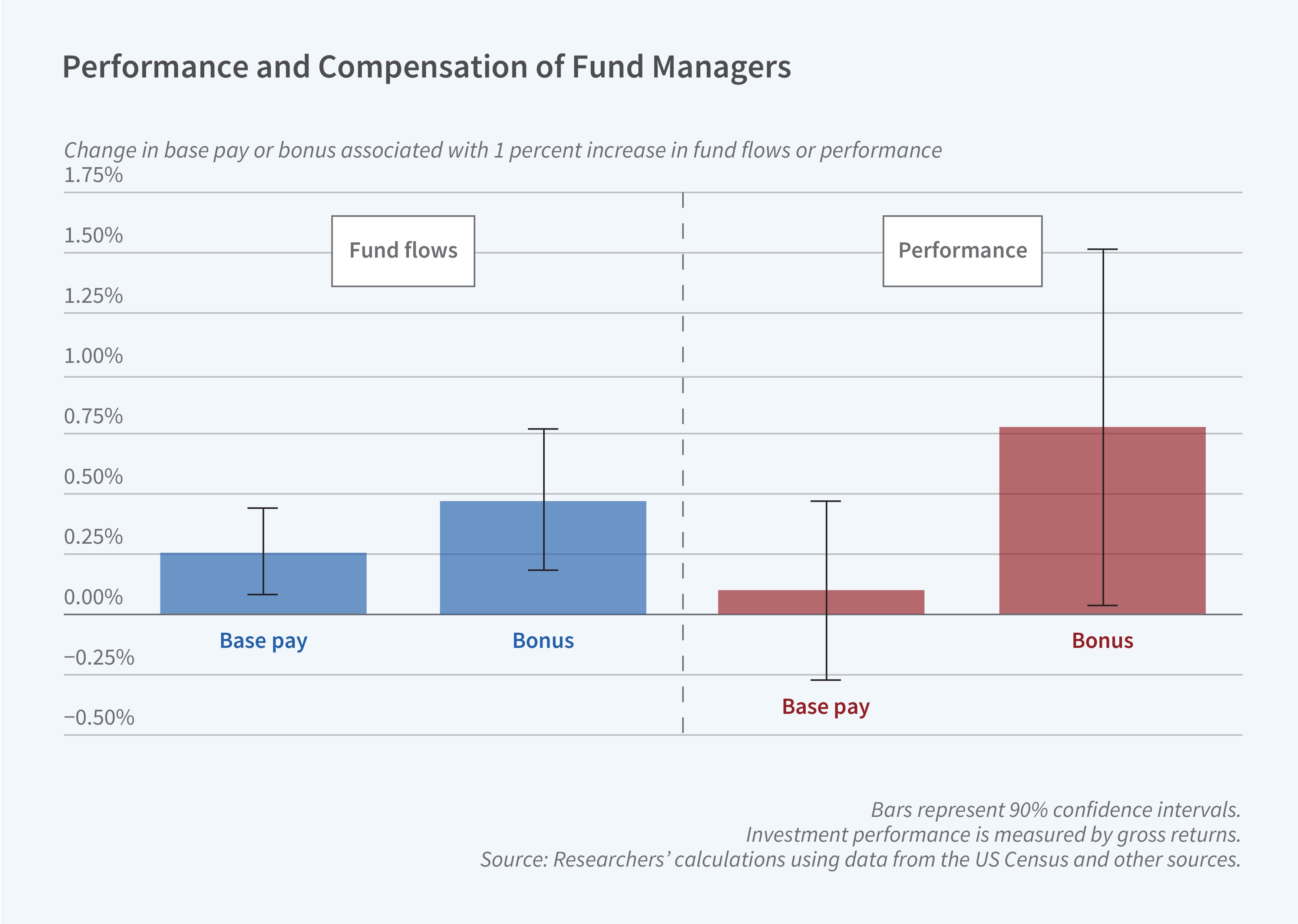

Growth in assets under management increases managers’ compensation, while strong investment returns primarily affect pay through their impact on AUM although they also influence bonuses.

The researchers demonstrate that fund managers’ compensation is primarily tied to their assets under management (AUM). In particular, a 1 standard deviation increase in capital inflows to a fund’s assets is associated with an estimated 6 percentage point rise in compensation. Additionally, strong performance by managers — yielding high returns on investments, whether relative to the market or not — primarily increases their compensation through its effect on AUM and has a sizable additional impact on bonuses. Furthermore, a manager’s pay is linked not just to the inflow of capital into their own fund but also to inflows into the broader fund family they belong to. These findings are at odds with the public statements of mutual funds, of which less than 20 percent claim their managers’ pay depends on AUM.

— Shakked Noy

Researchers Cen and Wu acknowledge the financial supports from Mays Mini Research Grant. Researcher Dou is grateful for the financial supports from the Rodney L. White Center for Financial Research, Wharton Dean’s Research Fund, and the Golub Faculty Scholar Award at Wharton. This study uses data from the Census Bureau’s Longitudinal Employer-Household Dynamics Program, a program partially supported by the following National Science Foundation Grants SES-9978093, SES-0339191, and ITR-0427889; National Institute on Aging Grant AG018854; and grants from the Alfred P. Sloan Foundation.