The Effect of the Fed’s Quantitative Easing on Bank Lending

Banks face a tradeoff between lending out as many of their assets as possible to maximize interest revenue and keeping enough liquid assets on hand to stave off potential bank runs. Since a run on a specific bank can lead to broader financial contagion, governments typically intervene to constrain banks’ behavior through instruments like leverage ratio regulations. These regulations involve restrictions on the ratio of a bank’s Tier 1 capital — its shareholders’ equity and retained earnings — to its total assets.

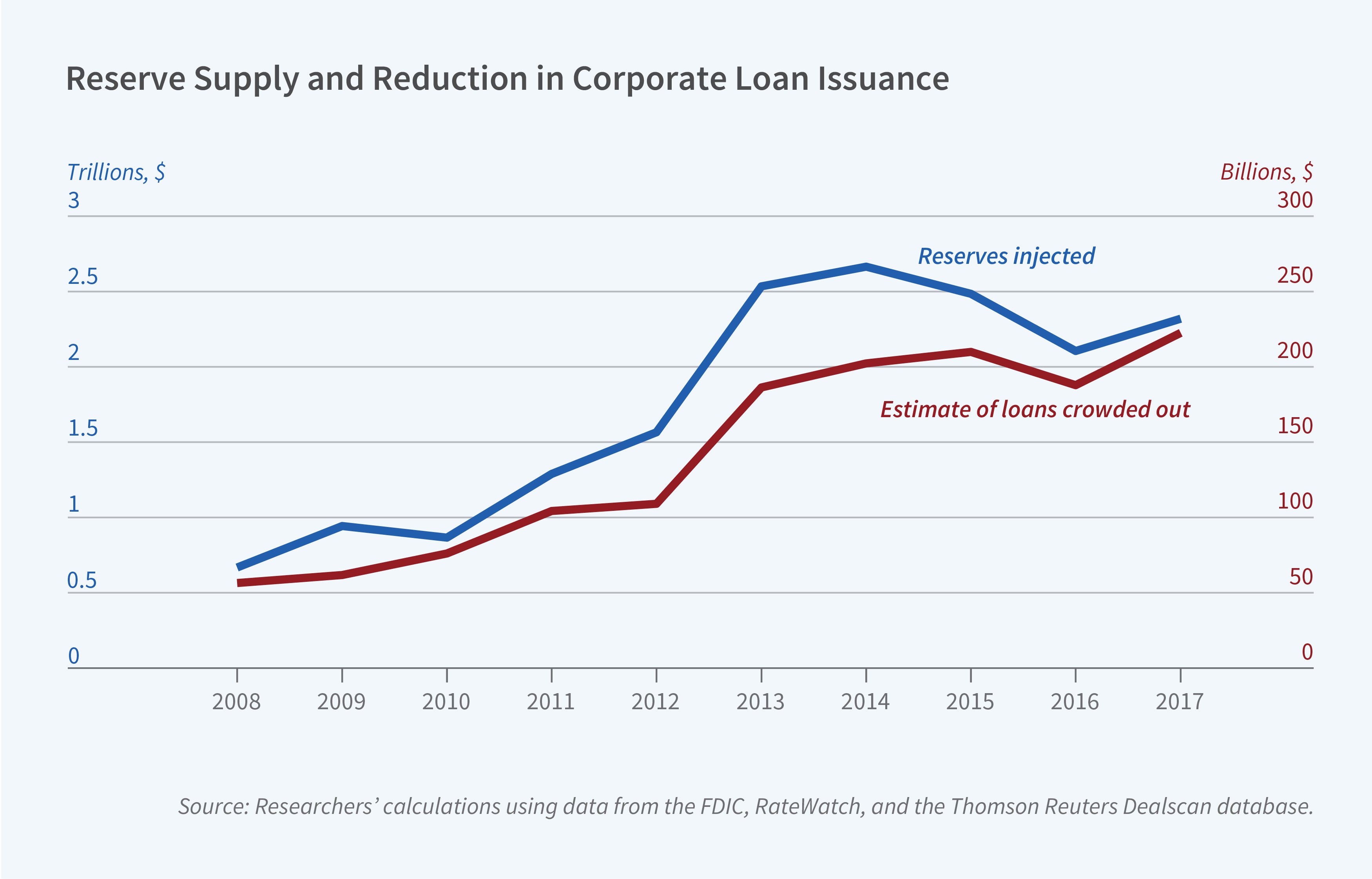

In response to the financial crisis of 2007–08, the Federal Reserve’s multitrillion dollar quantitative easing program used central bank reserves — liquid assets that must be held within the banking system — to purchase assets from outside the banking system. This had the effect of substantially increasing banks’ holdings of liquid assets as well as their total asset holdings. In aggregate, central bank reserves rose from less than $50 billion at the beginning of 2008 to $2.8 trillion in 2015.

In The Reserve Supply Channel of Unconventional Monetary Policy (NBER Working Paper 31693), William Diamond, Zhengyang Jiang, and Yiming Ma study the effect of this inflow of liquid assets on banks’ total lending. They note that the potential impact is ambiguous because an injection of liquid assets into a bank reduces the risk of extending the bank’s illiquid lending, which could result in more lending, but it also worsens the bank’s leverage ratio. Central bank reserve holdings count as part of a bank’s total assets, so a bank that holds more reserves must either reduce its holdings of other assets such as loans or raise more costly equity financing to satisfy leverage ratio regulations.

Every $1 increase in central bank reserves crowds out 8 cents of new bank lending, especially lending to firms.

The researchers present time series evidence showing that the expansion of central bank reserves from $0.02 trillion to $3.8 trillion between 2006 and 2021 coincided with a fall in banks’ share of loans and other illiquid assets from 83 percent to 63 percent. This suggests that growth in central bank reserves led to reduced lending, but it is inconclusive because the fall in lending could be explained by depressed demand for loans due to the Great Recession and business cycle fluctuations.

The researchers therefore develop estimates of both the demand for bank lending, using natural disasters as a source of variation in demand, and the cost of supplying loans, by tracing out the effects of differential deposit growth across different regions on banks’ observed costs. Combining these estimates in a structural model, they find that every additional $1 of central bank reserves crowds out about 8 cents of new bank lending to firms, consistent with the time series evidence. Overall, the researchers find that the expansion of central bank reserves between 2008 and 2017 reduced new bank lending by an average of about $140 billion per year, with a large part of this effect on bank lending to firms.

— Shakked Noy