The Role of Financial Factors in Economic Fluctuations

The 2008–09 global financial crisis and ensuing worldwide recession have brought renewed attention to the importance of credit conditions for the macroeconomy. From a theoretical perspective, two broad mechanisms link credit conditions to macroeconomic outcomes.

First, financial frictions on the side of borrowers imply that their borrowing costs include an external finance premium — the cost of borrowing above and beyond the relevant risk-free interest rate. Theory tells us that this external finance premium should vary with the net worth of the borrower relative to the amount borrowed — in effect, higher borrower leverage implies greater borrowing costs. During an economic downturn, the external finance premium increases as asset prices fall and leverage rises; this increase in borrowing costs causes a reduction in spending by households and firms, which further exacerbates the downturn.

Second, conditional on the quality of borrowers' balance sheets, the supply of credit offered by financial intermediaries may also vary over the cycle, rising in booms and falling in recessions. Financial disruptions reduce credit supply and cause borrowing costs to rise, conditional on the default characteristics of the borrowers. Broadly speaking, my work in this area uses information on borrowers' costs obtained from corporate bond prices to understand the role of credit supply fluctuations in determining economic outcomes.

The Predictive Content of Credit Spreads

To identify disruptions in credit markets, research on the role of asset prices in economic fluctuations has focused on the information content of various corporate credit spreads. This prior research, however, finds mixed results in the ability of credit spreads to forecast economic activity. A limitation of this literature is its reliance on aggregate credit spread indices that allow for a significant mismatch in the maturity composition of corporate bond yields and their risk-free Treasury counterparts. In effect, such series mix duration risk with credit risk.

In my first paper on this topic, Vladimir Yankov, Egon Zakrajšek, and I provide evidence that credit spreads are robust forecasters of economic activity, using a broad array of credit spreads constructed directly from the secondary bond prices on outstanding senior unsecured debt issued by a large panel of nonfinancial firms.1 This allows us to construct a credit spread for each bond outstanding, based on comparing the bond price to that of a synthetic risk-free Treasury security with matched cash flows. This "ground-up" approach solves the problem of maturity mismatch when constructing credit-spread indices.

An additional advantage of this ground-up approach is that we are able to construct matched portfolios of equity returns, allowing us to examine the information content of bond spreads that is independent of the information contained in stock prices of the same set of firms, as well as in macroeconomic variables measuring economic activity, inflation, interest rates, and other financial indicators. We document that our portfolio-based bond spreads contain substantial predictive power for economic activity and outperform — especially at longer horizons — standard credit-risk indicators.

This analysis is conducted using standard in-sample forecasting methods. A follow- up paper written with Jon Faust, Jonathan Wright, and Zakrajšek employs a large number of real and financial indicators to forecast real-time measures of economic activity within a Bayesian Model Averaging (BMA) framework.2 Our results indicate that BMA yields consistent improvements in the prediction of real activity measures, at horizons from the current quarter ("nowcasting") out to four quarters hence. The gains in forecast accuracy owe exclusively to the inclusion of our portfolio credit spreads in the set of predictors. Put differently, BMA consistently assigns a high posterior weight to models that include these financial indicators.

The Excess Bond Premium

An important question is the extent to which the predictive content of credit spreads occurs because of credit demand, including the cyclical variation in borrowers' credit risk, as opposed to variation in the willingness of bond holders to bear such risk, which we believe relates to credit-supply considerations.

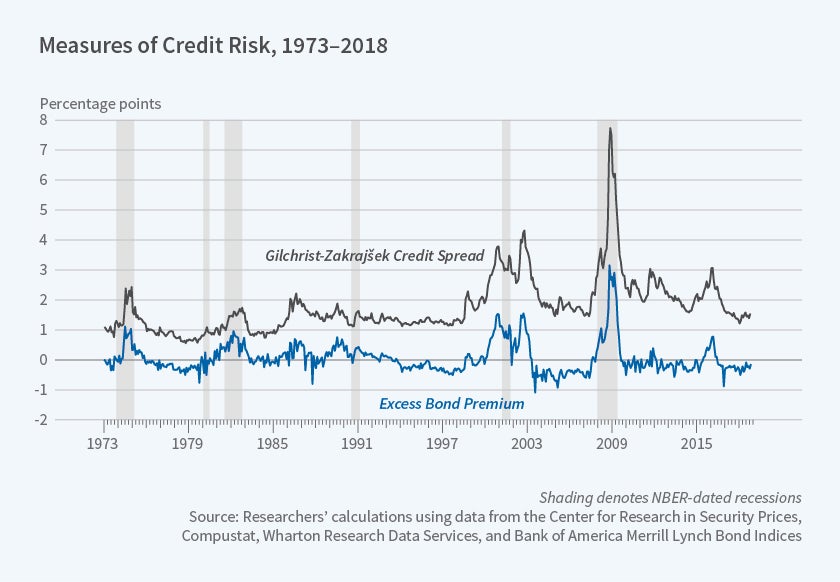

To address this issue, Zakrajšek and I follow the same ground-up approach to construct a single index of credit spreads — the Gilchrist-Zakrajšek (GZ) spread — based on all available bond data outstanding dating back to 1973.3 Using a flexible empirical framework, we then decompose this credit spread into two parts: a component reflecting the available firm-specific information on default risk and the excess bond premium (EBP), a residual component that can be thought of as capturing investor attitudes toward corporate credit risk — that is, credit market sentiment. In effect, the EBP tries to capture the variation in the average price of bearing U.S. corporate credit risk, above and beyond the compensation that investors in the corporate bond market require for expected defaults.

Figure 1 shows these two credit-risk indicators from January 1973 through October 2018. Both the GZ credit spread and the EBP increase significantly prior to, or during, most of the cyclical downturns since the early 1970s. In addition, both indicators reach an all-time high at the peak of the financial turmoil associated with the collapse of Lehman Brothers in September 2008.

A closer look at the excess bond premium in the period prior to the Lehman collapse offers a significant insight. Notably, the EBP is at its lowest point during the 2003–06 period, which is often viewed as a period of excessive risk-taking in the financial sector. The EBP begins to increase in early 2007, concomitant with the slowdown in home prices and rising concerns regarding the quality of commercial paper backed by securitized mortgage assets. These concerns substantially predate significant evidence of an impending slowdown in economic activity. In this sense, the EBP captures well the investor sentiment in the corporate bond market, as well as in other markets for risky assets, in the run-up to the financial crisis.

Using the GZ credit spread, we again document the ability of credit spreads to predict a wide range of real activity variables at both the one-quarter and one-year horizons. Focusing on data since the mid-1980s, a period that saw a substantial deepening of the U.S. corporate bond market, our results indicate that the excess bond premium accounts for all of the forecasting power of credit spreads for macroeconomic outcomes.

Such forecasting exercises do not allow a causal interpretation. Using standard identification methods from the structural vector autoregression (VAR) literature, we further document that innovations in the EBP that are orthogonal to the current state of the economy lead to significant declines in economic activity and equity prices. In quantitative terms, these estimates are on a par with the estimated effects of contractionary monetary policy shocks.

We also show that during the 2007–09 financial crisis, a deterioration in the creditworthiness of broker-dealers — who are key financial intermediaries in the corporate cash market — led to an increase in the excess bond premium. These findings support the notion that a rise in the EBP represents a reduction in the effective risk-bearing capacity of the financial sector and, as a result, a contraction in the supply of credit that has significant adverse consequences for the macroeconomy.

Recession Probabilities

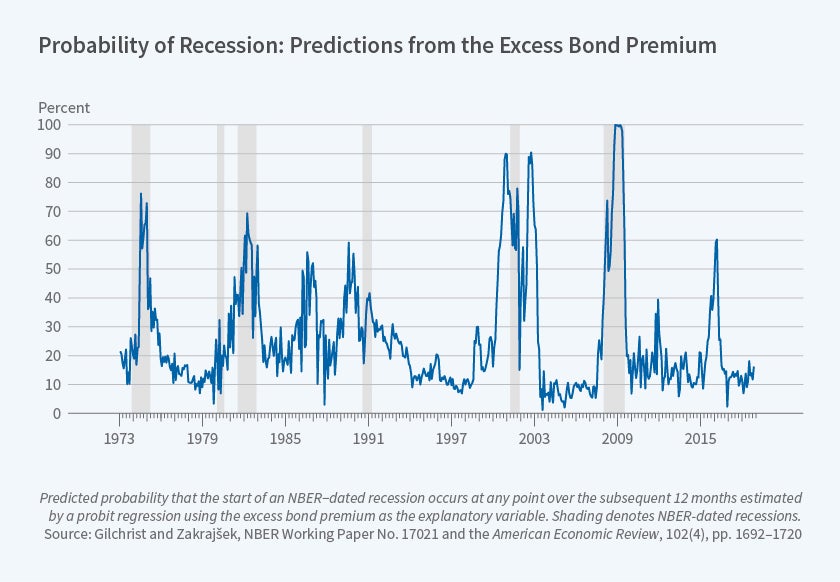

More recent work with Giovani Favara, Kurt Lewis, and Zakrajšek focuses on the ability of the excess bond premium to predict National Bureau of Economic Research-dated recessions, using a standard binary recession indicator approach.4 The leading statistical model in this area relies on a combination of the real federal funds rate and the term spread as the two primary recession predictors. Consistent with our prior results, we document that the GZ credit spread contains significant information — above and beyond these two variables — for recession risk over the 1973-2016 sample period. We further document that over the past four decades, the predictive power of credit spreads for economic downturns is due entirely to the EBP. Moreover, a model based solely on the EBP explains over half of the total variation captured by the broader model that includes the additional interest rate series.

To see the predictive content of the excess bond premium for recession outcomes, Figure 2 plots the implied recession probabilities from a statistical model that relies solely on the excess bond premium. In the post-1985 sample period, the EBP captures most of the variation in recession probabilities implied by such a framework. It also predicts the onset of the 2007–09 recession very well.

European Evidence

In other recent work, Benoit Mojon and I follow the same ground-up approach to construct credit risk indicators for euro-area banks and nonfinancial corporations.5

These indicators reveal that the financial crisis of 2008 dramatically increased the cost of market funding for both banks and nonfinancial firms in the euro area. The 2008 financial crisis also led to a systematic divergence in credit spreads for financial firms across national boundaries. Credit spreads for financial institutions in the periphery countries, Spain and Italy, widened considerably relative to their counterparts in the core countries such as France and Germany. This divergence in cross-country credit risk increased further as the European sovereign debt crisis intensified in 2010. This dramatic widening of such spreads in the periphery relative to the core of the euro zone reflects the disruptions to credit supply experienced by the periphery, as rising concerns regarding sovereign default risk spilled over into the private sector.

Consistent with this view, we show that credit spreads provide substantial predictive content for a variety of real activity and lending measures for the euro area as a whole and for individual countries. Again, using structural VAR methods to determine causality, our analysis implies that disruptions in corporate credit markets lead to sizable contractions in output, increases in unemployment, and declines in inflation across the euro area.

Causes of the Great Recession

An important question is why the fall in home prices and the resulting financial turmoil had such severe economic consequences during the Great Recession. One answer is that falling home prices led to a sharp reduction in spending by households, owing both to wealth effects and to households' propensity to borrow against housing wealth. An alternative view is that declining home prices led to financial sector losses and a sharp, broad-based decline in credit available to both firms and households.

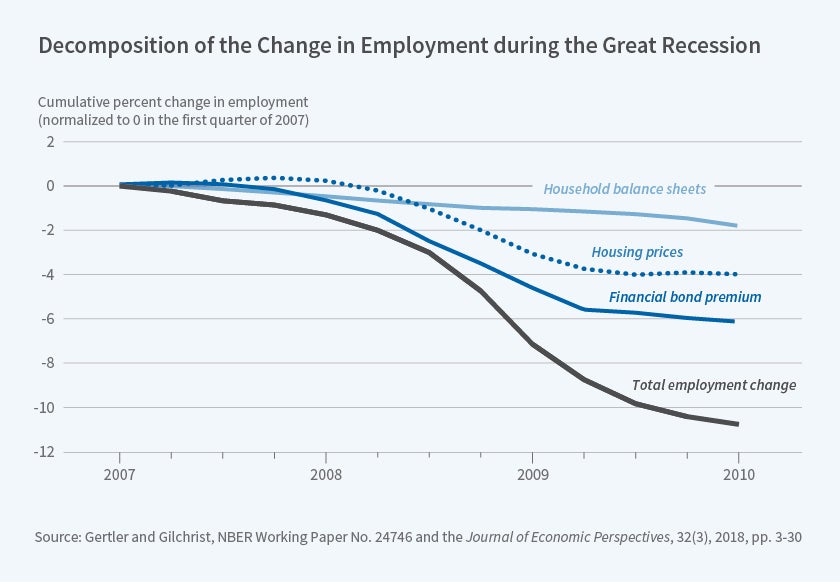

In a recent paper, Mark Gertler and I seek to assess the relative strength of these mechanisms within a panel data VAR framework.6 Household balance sheet effects during the crisis are identified through state-specific responses of employment to variation in home prices due to the differential degree to which households are indebted across geographic regions prior to the crisis. Conditional on such response, we then exploit time-variation in the EBP for financial sector bonds to capture an aggregate component that may be attributed to the broad-based declines in credit supply that are not specific to the household sector.

Figure 3 shows the resulting historical decomposition of aggregate employment into the usual effect of housing prices over the cycle that primarily affects construction employment, the household balance sheet effect specific to the Great Recession, and the effect of an aggregate reduction in credit supply as captured by the excess bond premium. This decomposition implies that contractions in the aggregate supply of credit, as measured by increases in the EBP, account for over 50 percent of the overall decline in employment during the 2007–10 period.

While much work remains to be done studying the link between credit conditions and economic activity, my research suggests that credit spreads forecast economic activity across a wide variety of settings. Moreover, the evidence suggests that disruptions in credit supply, as measured by variation in the excess bond premium, are a primary factor contributing to adverse economic outcomes. The fact that the excess bond premium rises prior to recessions and helps predict recession outcomes suggests that credit supply plays an important role in shaping the business cycle, and accounts for a large fraction of the overall decline in economic activity during the Great Recession.

Endnotes

S. Gilchrist, V. Yankov, and E. Zakrajšek, "Credit Market Shocks and Economic Fluctuations: Evidence from Corporate Bond and Stock Markets," NBER Working Paper 14863, April 2009, and Journal of Monetary Economics, 56(4), 2009, pp. 471–93.

J. Faust, J. Wright, S. Gilchrist, and E. Zakrajšek, "Credit Spreads as Predictors of Real-Time Economic Activity: A Bayesian Model-Averaging Approach," NBER Working Paper 16725, January 2011, and The Review of Economics and Statistics, 95(5), 2013, pp. 1501–19.

S. Gilchrist and E. Zakrajšek, "Credit Spreads and Business Cycle Fluctuations," NBER Working Paper 17021, May 2011, and the American Economic Review, 102(4), 2012, pp. 1692–1720.

G. Favara, S. Gilchrist, K. Lewis, and E. Zakrajšek, "Recession Risk and the Excess Bond Premium," FEDS Notes, Washington: Board of Governors of the Federal Reserve System, 2016, http://dx.doi.org/10.17016/2380-7172.1739.

S. Gilchrist and B. Mojon, "Credit Risk in the Euro Area," NBER Working Paper 20041, April 2014, and The Economic Journal, 128(608), 2017, pp. 118–58.

M. Gertler and S. Gilchrist, "What Happened? Financial Factors in the Great Recession," NBER Working Paper 24746, June 2018, and Journal of Economic Perspectives, 32(3), 2018, pp. 3–30.