The Structure of the International Monetary System

Anyone looking at recent financial headlines could be forgiven for thinking that the international monetary system is under heavy strains. The People's Bank of China faces severe private capital outflows, a result of the yuan's appreciation in tandem with the U.S. dollar and the slowing of the Chinese economy. The Bank of Japan is battling persistent deflation by trying to depreciate the yen. The European Central Bank has clearly telegraphed that it would welcome further depreciation of the euro. In the United States, notwithstanding a modest "lift-off" in December 2015, the Federal Reserve is confronted with a global slowdown and a rising dollar. Policy discussions explicitly mention the possibility of negative rates in the future. Talk of "currency wars" abounds.

To understand the current environment, it is helpful to step back and consider the international monetary system circa 1960, during the Bretton Woods era.

The International Monetary System then...

Back in those days, the international monetary system was relatively simple. Market economies pegged their currencies to the U.S. dollar. In turn, the United States maintained the value of its dollar at $35 per ounce of gold. With the assistance of the International Monetary Fund, countries could obtain liquidity to deal with "temporary" imbalances, but it was incumbent upon them to implement a fiscal and monetary policy mix that would be consistent with a stable dollar parity or, infrequently, to request an adjustment in their exchange rate.

The United States faced no such constraint. The requirement to maintain the $35 an ounce parity had only minimal bite on U.S. monetary authorities, as long as foreign central banks were willing, or could be convinced, to support the dollar. By design then, the system was asymmetric and dependent on the U.S., a situation that reflected the country's economic and political strengths in the immediate aftermath of World War II.1

Not everyone was happy about this state of affairs. Some objected to the special role of the dollar. In 1965, France famously requested the conversion of its dollar reserves into gold, while its minister of finance complained loudly about the United States' "exorbitant privilege."2 The Bretton Woods regime allowed the U.S. to acquire valuable foreign assets, so the argument went, because the dollar reserves required to maintain the dollar parity of foreign countries amounted to automatic low-interest, dollar-denominated loans to the U.S.3

Others worried about the long-term sustainability of the system. As the world economy grew rapidly in the 1950s and 1960s, so did the global demand for liquidity and the stock of dollar assets held abroad. With unchanged global gold supplies, something had to give. This is the celebrated "Triffin dilemma."4 In 1968, Triffin's predictions came to pass: Faced with a run on gold reserves, the U.S. authorities suspended dollar-gold convertibility. Shortly thereafter, the Bretton Woods system of fixed but adjustable parities was consigned to the dustbin of history.

Outside the Zero Lower Bound: Exorbitant Privilege, Safe Assets, and Exorbitant Duty

Under the new regime, countries were free to adjust monetary policy independently. Mundell's "Trilemma" required either that market forces determine the value of the currency or that capital controls be imposed.5 In principle, this environment should be more symmetrical: no more "exorbitant privilege" for the U.S. since other countries would not be forced to hold low-interest dollar reserves to maintain their dollar exchange rate; no asymmetry in external adjustment between the U.S. and the rest of the world since exchange rates would now adjust freely; and no Triffin dilemma since dollar liquidity would be de-coupled from gold supply.

Yet, recent research illustrates that the era of floating rates shares many of the same structural features as the Bretton Woods regime. Consider the question of the "exorbitant privilege," defined as the excess return on U.S. gross external assets relative to U.S. gross external liabilities. Hélène Rey and I set out to measure this excess return using disaggregated data on the U.S. Net International Investment Position and its balance of payments. These calculations are often imprecise, given the coarseness of the historical data, but they all point in the same direction: the U.S. earns a significant excess return which has increased since the end of the Bretton Woods regime from 0.8 percent per annum between 1952 and 1972, to between 2.0 percent and 3.8 percent per annum since 1973.6

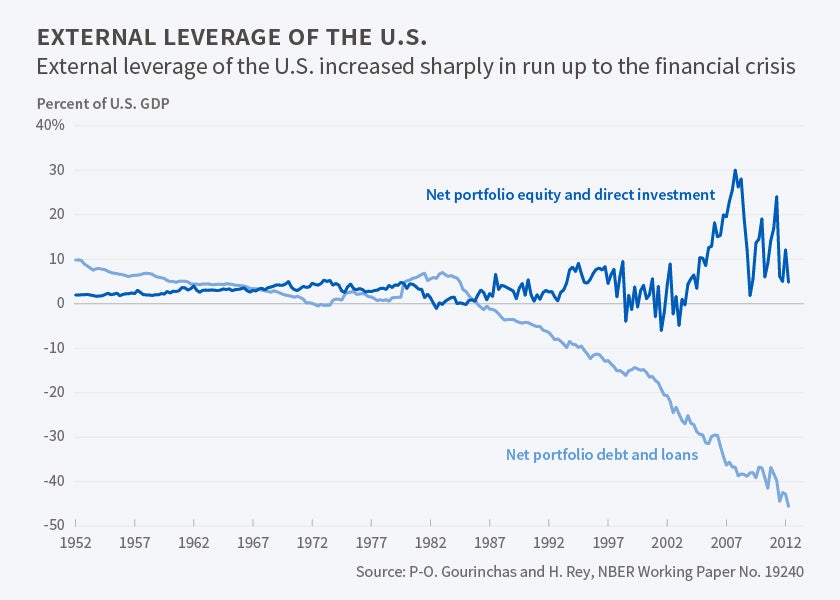

A large share of these excess returns arises because of the changing composition of the U.S. external balance sheet over time. As financial globalization proceeded, U.S. investors concentrated their foreign holdings in risky and/or illiquid securities such as portfolio equity or direct investment, while foreign investors concentrated their U.S. asset purchases in portfolio debt, especially Treasuries and bonds issued by government-affiliated agencies in areas such as housing finance, and cross-border loans.7 [See Figure 1.] The "exorbitant privilege" should be properly understood as a risk premium.

These large and growing U.S. excess returns have first-order implications for the sustainability of U.S. trade deficits and the interpretation of current account deficits. As an illustration of the orders of magnitude involved, suppose that the U.S. has a balanced net international investment position with gross assets and liabilities of 100 percent of GDP. An excess return of 2 percent per annum implies that, on average, the U.S. can run an annual trade deficit of 2 percent of GDP while leaving its net international investment position unchanged. More generally, since a large part of realized returns take the form of valuation gains due to changes in asset prices and exchange rates, the current account, which excludes non-produced income such as capital gains, will provide an increasingly distorted picture of the change in a country's external position.8

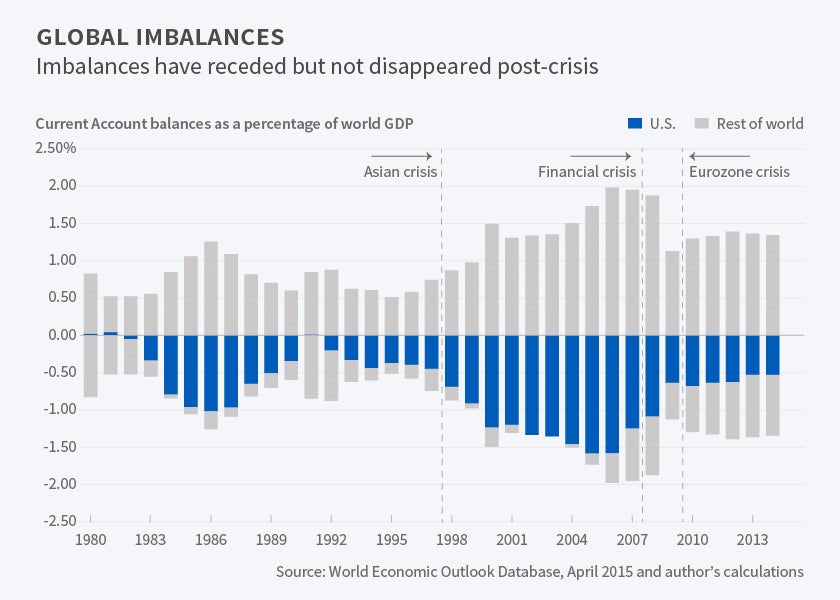

Consider next the question of external adjustment. The U.S. still faces a very different process than most other countries. For instance, Rey and I found that a deterioration of the U.S. trade balance or of its net international investment position is often followed by a predictable depreciation of the U.S. dollar against other currencies. This depreciation may subsequently improve the U.S. trade balance along the usual channels, but it also improves the return on U.S. financial assets held abroad, thereby making the U.S. relatively richer.9 Most other countries don't seem to enjoy a similar advantage.10 These findings help us understand why markets have taken a somewhat benign view of persistent U.S current account deficits since the 1980s. [See Figure 2.]

What accounts for this risk premium? In my work with Ricardo Caballero and Emmanuel Farhi, we argue that it reflects a superior capacity of the U.S. to supply "safe" assets—assets that will deliver stable returns even in global downturns. To illustrate the argument, consider a world consisting of only two regions, the U.S. (U) and the rest of the world (R). The regions may vary in their capacity to produce safe assets because of differences in the soundness of their fiscal policy or in their levels of financial development. They may also differ in their demand for these assets because of demographic differences, financial frictions, and/or differences in preferences for saving.11

Suppose U is a natural net supplier of these assets. If the two regions were forced to live in financial autarky, unable to borrow from, or lend to, one another, the price of safe assets would be higher in R, and their return lower. If the two regions integrate financially, capital will flow from R to U, as R investors are eager to purchase U’s safe assets. From the perspective of U, two things happen: It runs a current account deficit (foreign capital flows in), and interest rates decrease. By the same logic, suppose R’s risky assets offer a higher autarky return. Then U would also want to invest in these risky assets. The pattern of cross-border gross financial flows and positions would resemble the one we observe in the data with the U.S. investing in foreign risky assets, issuing safe assets, and earning a risk premium.12

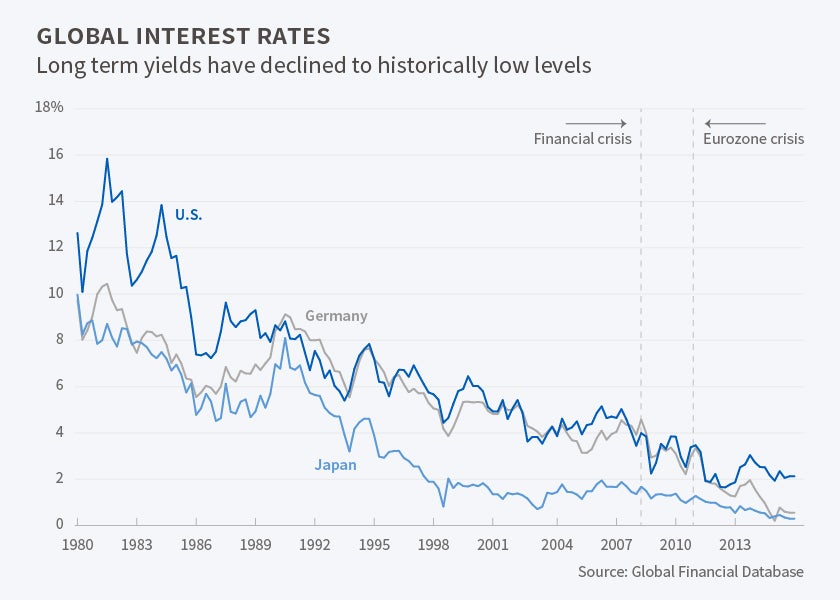

This line of research successfully accounts for the simultaneous deterioration in U.S. current account balances [Figure 2], the secular decline in real interest rates [Figure 3], and the increased leverage of the U.S. external portfolio since the 1980s [Figure 1]. These trends reflect a combination of shocks such as the collapse of the Japanese equity and housing bubbles of the early 1990s and the Asian financial crisis of 1997, and trends such as the integration of China into the world economy with low initial levels of financial development and rapidly aging populations in Japan, Germany, and China.13 The flip side of the "exorbitant privilege" is an increased vulnerability of the United States' external portfolio to global shocks, which Rey and I dubbed the "exorbitant duty."14 Indeed, we estimate that, at the peak of the global financial crisis, U.S. valuation losses, corresponding to the valuation gains of the rest of the world, amounted to roughly 14 percent of U.S. GDP.15 We then build a model in which the U.S. has more risk-absorbing capacity than the rest of the world. The model replicates the external portfolio structure of the U.S., long on risky assets and short on safe ones—exorbitant privilege as well as exorbitant duty. The model has one key implication: Willingly or not, global suppliers of safe-haven assets must bear more exposure to global risks. These findings carry important lessons for regional safe-asset providers such as Germany or Switzerland, or for future safe-asset providers, be they the eurozone or China. Lower funding costs come with a commensurate increase in the global exposure of their external balance sheet.

At the Zero Lower Bound: Capital Flows and Currency Wars

With the global financial crisis and its aftermath, we have entered a new phase in the relationship between safe-asset im-balances and capital flows. The crisis triggered a sharp contraction in safe-asset supply and a surge in global demand as house-holds and the non-financial corporate sector attempted to deleverage. These shocks further depressed equilibrium real interest rates, pushing policy rates throughout the developed world to the Zero Lower Bound (ZLB).16

In recent theoretical work, Caballero, Farhi, and I show that the safe-asset scarcity mutates at the ZLB, from a benign phenomenon that depresses risk-free rates to a malign one where interest rates cannot equilibrate asset markets any longer, leading to a global recession. The reason is that the decline in output reduces net-asset demand more than asset supply.17 Hence our analysis predicts the emergence of potentially persistent global-liquidity traps, a situation that actually exists in most of the advanced economies today.

Our theoretical model features nominal rigidities, so that the ZLB matters, and a non-Ricardian setting, so that heterogeneity in asset supply and demand affects interest rates. We use this framework to address two questions.

First, we ask: What is the role of capital flows at the ZLB? We find that, everything else equal, capital flows propagate recessions from one country to another. Countries with more-severe safe-asset scarcities under financial autarky will experience milder recessions when integrated, and will run current account surpluses. In effect, current account surpluses help spread liquidity traps globally. Next we ask: What is the role of exchange rates? Here, our theoretical analysis delivers an important result: Within a range, the nominal exchange rate becomes indeterminate. The fundamental reason is that exchange rates are indeterminate when countries follow pure interest-rate targets, as is the case at the ZLB.18 In our environment, this indeterminacy has real consequences. Different values of the nominal exchange rate translate into different values of the real exchange rate, and therefore affect the relative demand for domestic versus foreign goods. Our theoretical framework provides a powerful way to think about the current lively debate on currency wars. By pursuing policies that lead to a more-depreciated exchange rate, a country can shift the burden of the global recession onto its trading partners, a beggar-thy-neighbor policy.19

Our analysis also uncovers a new and important dimension of the "exorbitant duty" faced by safe-asset net suppliers. In a ZLB environment, such nations either must have more-appreciated currencies, as a result of investors' flight to safety, or lower funding costs, because their currencies are expected to appreciate in case of global shocks. The first effect tends to worsen the size of the ZLB recession for these countries. The second indicates that these safe-asset suppliers are more likely to hit the ZLB in the first place and experience a recession. Either way, safe-asset suppliers shoulder a larger share of the burden. Yet, because issuance of safe assets anywhere, public or private, is beneficial everywhere, the global provision of safe assets may remain inadequate.

This recent research illustrates that the fundamental structure of the international monetary system may largely transcend formal exchange-rate arrangements, with U.S. dollar assets at the center. Going forward, this raises a number of important questions which current research is exploring. First, a recent and influential line of work is questioning whether floating exchange rates provide much insulation against foreign shocks, a central tenet of Mundell's Trilemma.20 If they don't, monetary authorities may find that they are even more dependent on the monetary policy "at the center" than was the case during Bretton Woods.

Second, our results point to a modern — and more sinister — version of the Triffin dilemma. As the world economy grows faster than that of the U.S., so does the global demand for safe assets relative to their supply.21 This depresses global interest rates and could push the global economy into a persistent ZLB environment, a form of secular stagnation.22

One likely response would be the endogenous emergence of alternatives to dollar-denominated safe assets produced either by the private sector or by other countries. This raises the difficult question of how different safe assets can coexist and compete in equilibrium, and suggests that the safety of an asset is an equilibrium outcome, one that depends both on the underlying fundamental characteristics of the asset itself and also of the coordination decisions of investors.23

Finally, a body of empirical evidence suggests that environments with low interest rates may fuel leverage boom and bust cycles. The vulnerability of emerging and advanced economies alike to these crises has been amply demonstrated in the past. At the country level, the empirical evidence suggests that self-insurance via official reserve (safe asset) accumulation is an effective line of defense against leveraged booms.24 But what is optimal at the level of an individual country may be inefficient at a global level if it fuels further safe-asset scarcity and depresses global interest rates. This question is central to current discussions on global safety nets.

Endnotes

For a discussion of the original Bretton Woods negotiations and especially the exchanges between J. M. Keynes, on the U.K. delegation, and H. D. White, from the U.S. Treasury, see B. Stein, The Battle of Bretton Woods, Princeton, NJ: Princeton University Press, 2013.

R. Aron, Le Figaro, February 16, 1965, from Les Articles du Figaro, vol. II, Paris, France: Editions de Fallois, 1994, p.1475. For a historical perspective on the exorbitant privilege, see also B. Eichengreen, Exorbitant Privilege: The Rise and Fall of the Dollar, Oxford, United Kingdom: Oxford University Press, 2012.

J. Rueff, "The West is Risking a Credit Collapse," Fortune, June 1961, pp.126–7, 262, and 167–268.

R. Triffin, Gold and the Dollar Crisis: The Future of Convertibility, New Haven, CT: Yale University Press, 1960.

R. Mundell, "Capital Mobility and Stabilization Policy under Fixed and Flexible Exchange Rates," Canadian Journal of Economic and Political Science, 29(4), 1963, pp. 475–85.

P.-O. Gourinchas and H. Rey, "From World Banker to World Venture Capitalist: U.S. External Adjustment and the Exorbitant Privilege," NBER Working Paper 11563, August 2005, and in G7 Current Account Imbalances: Sustainability and Adjustment, R. Clarida, ed., Chicago, IL: University of Chicago Press, 2007. See also P.-O. Gourinchas and H. Rey, "External Adjustment, Global Imbalances and Valuation Effects," NBER Working Paper 19240, July 2013, and Chapter 10 in G. Gopinath, E. Helpman, and K. Rogoff, eds., Handbook of International Economics, Volume 4, Amsterdam, The Netherlands: North Holland, Elsevier, 2014, pp.585–645. For a more conservative estimate on a shorter time period, see S. Curcuru, T. Dvorak, and F. Warnock, "Cross-Border Return Differentials," NBER Working Paper 13768, February 2008, and Quarterly Journal of Economics, 123(4), 2008, pp. 1495–1530.

Recent work on the structure of global banking flows helps nuance this picture. For instance, H. Shin, "Global Banking Glut and Loan Risk Premium," IMF Economic Review, 60(2), 2012, pp. 155–92, shows that prior to the financial crisis, foreign banks borrowed dollars from U.S. money market funds, and invested in riskier U.S. assets such as mortgage backed securities.

See for instance M. Obstfeld, "Does the Current Account Still Matter," NBER Working Paper 17877, March 2012, and American Economic Review, 102(3), May 2012, pp. 1-23, and also P.-O. Gourinchas and H. Rey, "External Adjustment, Global Imbalances and Valuation Effects," NBER Working Paper 19240, July 2013, and Chapter 10 in, Handbook of International Economics, Volume 4, op. cit., for a range of countries.

P.-O. Gourinchas and H. Rey, "International Financial Adjustment," NBER Working Paper 11155, February 2005, and Journal of Political Economy, 115(4), August 2007, pp. 665–703. See also G. Corsetti and P. Konstantinou, "What Drives U.S. Foreign Borrowing? Evidence on the External Adjustment to Transitory and Permanent Shocks," American Economic Review, 102(2), April 2012, pp. 1062–92.

However, K. Rogoff and T. Tashiro, "Japan's Exorbitant Privilege," Journal of the Japanese and International Economies, 35, March 2015, pp. 43–61, find positive excess returns for Japan between 2001 and 2013.

R. Caballero, E. Farhi, and P.-O. Gourinchas, "An Equilibrium Model of 'Global Imbalances' and Low Interest Rates," NBER Working Paper 11996, February 2006, and American Economic Review, 98(1), 2008, pp. 358–93. See also B. Bernanke, "The Global Saving Glut and the U.S. Current Account Deficit," Sandridge Lecture, Virginia Association of Economics, Richmond, VA, Federal Reserve Board, March 2005; and E. Mendoza, V. Quadrini, and J.-V. Rios-Rull, "Financial Integration, Financial Deepness, and Global Imbalances," NBER Working Paper 12909, February 2007, and Journal of Political Economy, 117(3), 2009, pp. 371–410.

The implications in terms of overall current account surplus or deficit are more complex when both risky and safe assets are traded and depend on the relative scarcities in safe and risky asset. See R. Caballero, E. Farhi, and P.-O. Gourinchas, "Safe Asset Scarcity and Aggregate Demand," NBER Working Paper 22044, February 2016, and American Economic Review Papers and Proceedings, forthcoming.

On China, see Z. Song, K. Storesletten, and F. Zilibotti, "Growing Like China," American Economic Review, 101(1), 2011, pp. 196-233; and N. Coeurdacier, S. Guibaud, and K. Jin, "Credit Constraints and Growth in a Global Economy," American Economic Review, 105(9), 2015, pp. 2838–81.

P.-O. Gourinchas, H. Rey, and N. Govillot, "Exorbitant Privilege and Exorbitant Duty," University of California, Berkeley, mimeo, May 2010.

P.-O. Gourinchas, H. Rey, and K. Truempler, "The Financial Crisis and The Geography of Wealth Transfers," NBER Working Paper 17353, August 2011, and Journal of International Economics, 88(2), 2012, pp. 266–83, explore the geographic distribution of valuation gains and losses during the financial crisis and find that losses are concentrated in the U.S., the eurozone, and China.

Most estimates of the natural rate of interest rate such as T. Laubach and J. Williams, "Measuring the Natural Rate of Interest," Federal Reserve Bank of San Francisco Working Paper 2015–16, October 2015, or J. Hamilton, E. Harris, J. Hatzius, and K. West, "The Equilibrium Real Funds Rate: Past, Present, and Future," NBER Working Paper 21476, August 2015, are consistent with a substantial decline in the natural real interest rate. Strictly speaking, the ZLB should be defined as the lowest admissible nominal interest rate. As demonstrated by various central banks in recent months, this lowest admissible nominal interest rate may well be negative.

R. Caballero, E. Farhi, and P.-O. Gourinchas, "Global Imbalances and Currency Wars at the ZLB," NBER Working Paper 21670, October 2015. A related analysis is G. Eggertsson, N. Mehrotra, S. Singh, and L. Summers, "A Contagious Malady? Open Economy Dimensions of Secular Stagnation," Working paper, November 2015. By definition, the supply of true safe assets does not change with a decline in output, hence the recession disproportionately affects safe asset demand.

J. Kareken and N. Wallace, "On the Indeterminacy of Equilibrium Exchange Rates," Quarterly Journal of Economics, 96(2), 1981, pp. 207–22.

Outside the ZLB, this type of beggar-thy-neighbor policy is unnecessary since each country can reach potential output via traditional monetary policy while letting its currency fluctuate.

H. Rey, "Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence," NBER Working Paper 21162, May 2015, and in Proceedings of the Economic Policy Symposium, Jackson Hole, 2013, Federal Reserve Bank of Kansas City; and E. Farhi and I. Werning, "Dilemma not Trilemma? Capital Controls and Exchange Rates with Volatile Capital Flows," IMF Economic Review, 62(4), 2014, pp. 569–605. See also B. Bernanke, "Federal Reserve Policy in an International Context," IMF Economic Review, Mundell Fleming lecture, forthcoming 2016, for a dissenting view.

E. Farhi, P.-O. Gourinchas, and H. Rey, Reforming the International Monetary System, London, UK: Centre for Economic Policy Research (CEPR), 2011; See also, M. Obstfeld, "The International Monetary System: Living with Asymmetry," NBER Working Paper 17641, December 2011, and in R. Feenstra and A. Taylor, eds., Globalization in an Age of Crisis: Multilateral Economic Cooperation in the Twenty-First Century, Chicago, IL: University of Chicago Press, 2014, pp. 301–36.

L. Summers, "Have We Entered an Age of Secular Stagnation?" IMF Economic Review, 63(1), 2015, pp. 277–80.

P.-O. Gourinchas and O. Jeanne, "Global Safe Assets," BIS Working Paper 399, December 2012; See also Z. He, A. Krishnamurthy, and K. Millbradt, "A Model of the Reserve Asset," Stanford Graduate School of Business mimeo, 2015, for a model of competition between reserve assets.

P.-O. Gourinchas and M. Obstfeld, "Stories of the Twentieth Century for the Twenty-First," NBER Working Paper 17252, July 2011, and American Economic Journal: Macroeconomics, 4(1), 2012, pp. 226–65.