When the Fed Lowers U.S. Rates, Emerging Market Loans Soar

Reductions in the target interest rate are associated with sharp increases in dollar-denominated loan volumes in emerging markets relative to developed markets.

Roughly 80 percent of cross-border loans to emerging market economies are estimated to be denominated in U.S. dollars. Dollar-denominated credits make up 60 percent of Europe's emerging market economies' cross-border lending and over 90 percent of foreign banks' loans to emerging market economies in Africa, Asia, and the Americas. Foreign bank loans account for about half of all emerging market economies' external liabilities.

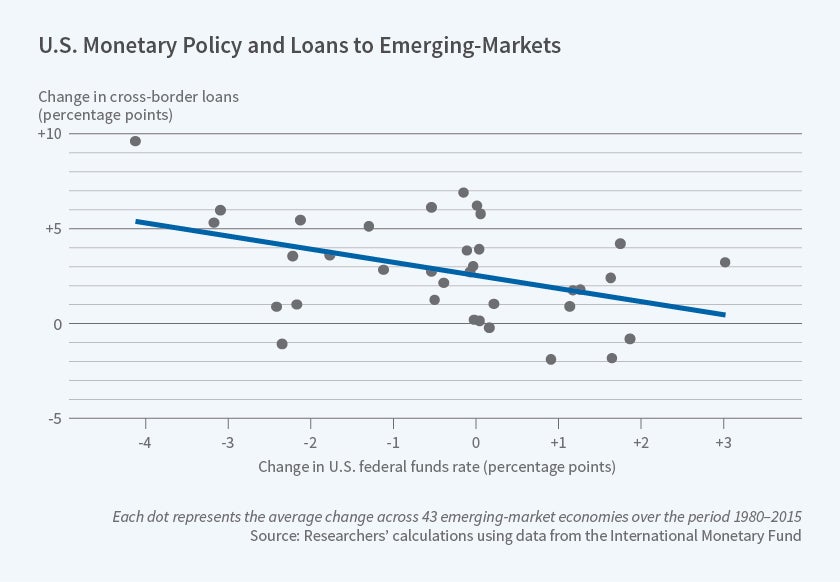

In U.S. Monetary Policy and Emerging Market Credit Cycles (NBER Working Paper 25185), Falk Bräuning and Victoria Ivashina find that when the Federal Reserve lowers U.S. interest rates, there is an increase in cross-border loan volumes by global banks, particularly with regard to emerging market economies. Studying the 1980-2015 period, even after accounting for differences in GDP growth, inflation, and forecast future economic performance, they find that a 4 percentage point cut in the Federal Reserve's target interest rate (a typical decrease during an easing cycle) increased loan volumes in emerging markets by 32 percent relative to the volumes in developed markets.

Using data from the Thomson Reuters DealScan database on global syndicated corporate loan issues, the researchers show that the result holds for non-U.S. banks and for banks with portfolios that have little exposure to the United States. Controlling for individual borrowers, their home countries, loan amounts, currency, maturity, interest rates, and lenders in the loan syndicate shows that the results apply to borrowers in non-tradable industries and those in countries having little trade linkage with the United States.

Loan volumes also respond to the yield spread — the difference between the 10-year U.S. Treasury yield and the federal funds rate. As the spread narrows and banks rebalance their lending portfolios toward risker assets, a 1 percent decrease in the U.S. spread increases emerging market economy lending volumes by about 16 percent. This effect was particularly relevant earlier this decade, when the Federal Reserve kept the federal funds rate at zero and eased monetary policy through unconventional measures that directly impacted long-term rates.

Monetary policy easing also is associated with higher loan volumes to riskier firms. In response to a 25 basis point decrease in the U.S. federal funds rate, firms with a 1 percentage point higher borrowing cost than their country average enjoy a 1 percent higher increase in loans than that afforded to average borrowers.

When U.S. monetary policy tightens, loan volumes from foreign banks fall. Increases in the federal funds rate of 25 basis points were associated with a 4.2 percentage point larger overall decline in dollar credit for emerging market firms than for developed market firms. Local bank lenders do not offset a contraction in foreign bank credit. Rather, local dollar credit also contracts. A 25 basis point increase in the federal funds rate leads to a 3.5 percentage point drop in local credit.

Changes in eurozone rates affect the volume of euro-denominated cross-border lending of U.S. banks to non-euro borrowers, but they do not affect the volume of dollar-denominated credits. The researchers conclude that "foreign monetary policy is relevant only for the loans in the corresponding foreign currency."

— Linda Gorman