Quantifying the Impact of ECB Policies during the Debt Crisis

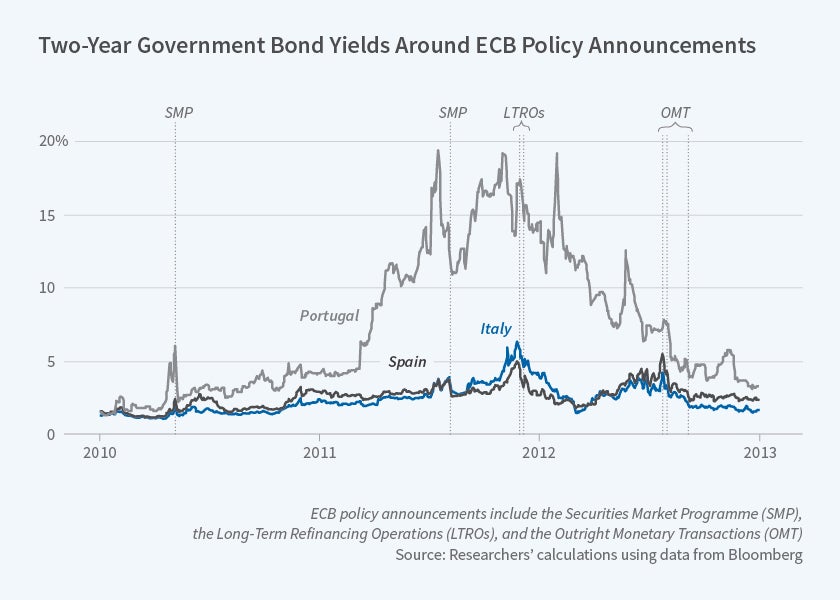

Two-year bond yields declined by 400 basis points for Italy and Spain, by 500 basis points for Ireland and Portugal, and by 1,000 basis points for Greece.

During the European debt crisis, several countries experienced large increases in government borrowing costs. The yields on government bonds for Ireland, Italy, Portugal, and Spain rose from around 2 percent in 2009 to between 7 and 20 percent in 2011, and Greek two-year bond yields rose to 200 percent in 2012. In response to this situation, the European Central Bank (ECB) enacted policies designed to reduce bond yields, including the Securities Markets Programme (SMP), Outright Monetary Transactions (OMT), and Long-Term Refinancing Operations (LTRO).

In ECB Policies Involving Government Bond Purchases: Impact and Channels (NBER Working Paper No. 23985), Arvind Krishnamurthy, Stefan Nagel, and Annette Vissing-Jorgensen examine the effects of these policies and quantify the effect of the SMP and OMT on bond yields. They also test for broader macroeconomic effects from these policies in the form of stock and corporate bond price increases both in distressed nations and in core eurozone countries.

The SMP, which started in May 2010, allowed the ECB to directly purchase government debt, with an initial focus on debt issued by Greece, Ireland, and Portugal. The program expanded to include Italy and Spain in 2011. In September 2012, the ECB initiated the OMT, which also allowed for government bond purchases but required that countries apply for the program and agree to undergo fiscal adjustments. The ECB also enacted three-year LTROs, an extension of a previous program that provided loans to banks. These loans were used, in part, to buy government debt.

The researchers find large decreases in sovereign bond yields following the introduction of the SMP and OMT. The yields on bonds with two-year maturities declined by 400 basis points for Italy and Spain (around 200 basis points each from the SMP and the OMT), by 500 basis points for Ireland and Portugal, and by 1,000 basis points for Greece. The LTRO policy had more modest impacts. The researchers find that the largest impact was a 50 basis point reduction in borrowing costs for Spain.

To analyze why yields declined, the researchers focus on Italy, Spain, and Portugal for reasons of data availability. The ECB publicly specified two goals for its programs. It sought to reduce the possibility that eurozone countries would split off and redenominate domestic debt in new currencies ("redenomination risk") and it hoped to stabilize dysfunctional segments of the bond market, a problem called "market segmentation." In addition to affecting redenomination risk and market segmentation, the ECB's actions may also affect the default risk for sovereign bonds by changing market expectations of fiscal transfers and via lower redenomination risk and market segmentation lowering borrowing costs and thus default risk.

For both the SMP and OMT, the researchers find that the majority of the decline in yields can be explained by a drop in default risk and a fall in the degree of market segmentation. In Italy, default risk accounted for 30 percent of the fall in yields, while a decline in market segmentation was responsible for the other 70 percent. In Spain, default risk accounted for 42 percent, market segmentation for 43 percent, and redenomination risk for 15 percent. For Portugal, falling default risk explained 40 percent of the decline, a reduction in market segmentation explained 36 percent, and a decline in redenomination risk explained 24 percent.

The SMP and the OMT also had substantial impacts on the stock markets of the distressed countries and core eurozone countries. The SMP led to a 4 percent increase in stock values, and the OMT led to a 13 percent rise. Stock market returns following the LTRO were mixed — some countries saw positive returns; others experienced negative returns.

— Morgan Foy