Modern InfoTech and the Democratization of Security Filings

After the SEC’s EDGAR system expanded access to firms’ financial data, the role of expert analysis in moving stock prices declined, and firm investment became less sensitive to market price swings.

Modern information technology has democratized corporate disclosures, making them broadly available and easy and inexpensive to access. In theory, the timely spread of key data about firms should enable investors to stay informed about company prospects, thereby reducing their risk and potentially lowering the cost of capital to firms. Conventional wisdom suggests that the more broadly a company’s information is disseminated, the more liquid and less volatile its stock. New research reported in The Real Effects of Modern Information Technologies (NBER Working Paper 27529) finds that putting US company filings online in the 1990s has had more nuanced effects.

The researchers, Itay Goldstein, Shijie Yang, and Luo Zuo, study the impact of the adoption of the US Securities and Exchange Commission’s (SEC’s) Electronic Data Gathering, Analysis, and Retrieval (EDGAR) system. The system includes detailed information on a range of corporate securities filings. EDGAR was implemented gradually over a period of three years. The SEC divided public companies into 10 groups and ordered the first group to put their documents on EDGAR in April 1993. The last group began posting to EDGAR in May 1996.

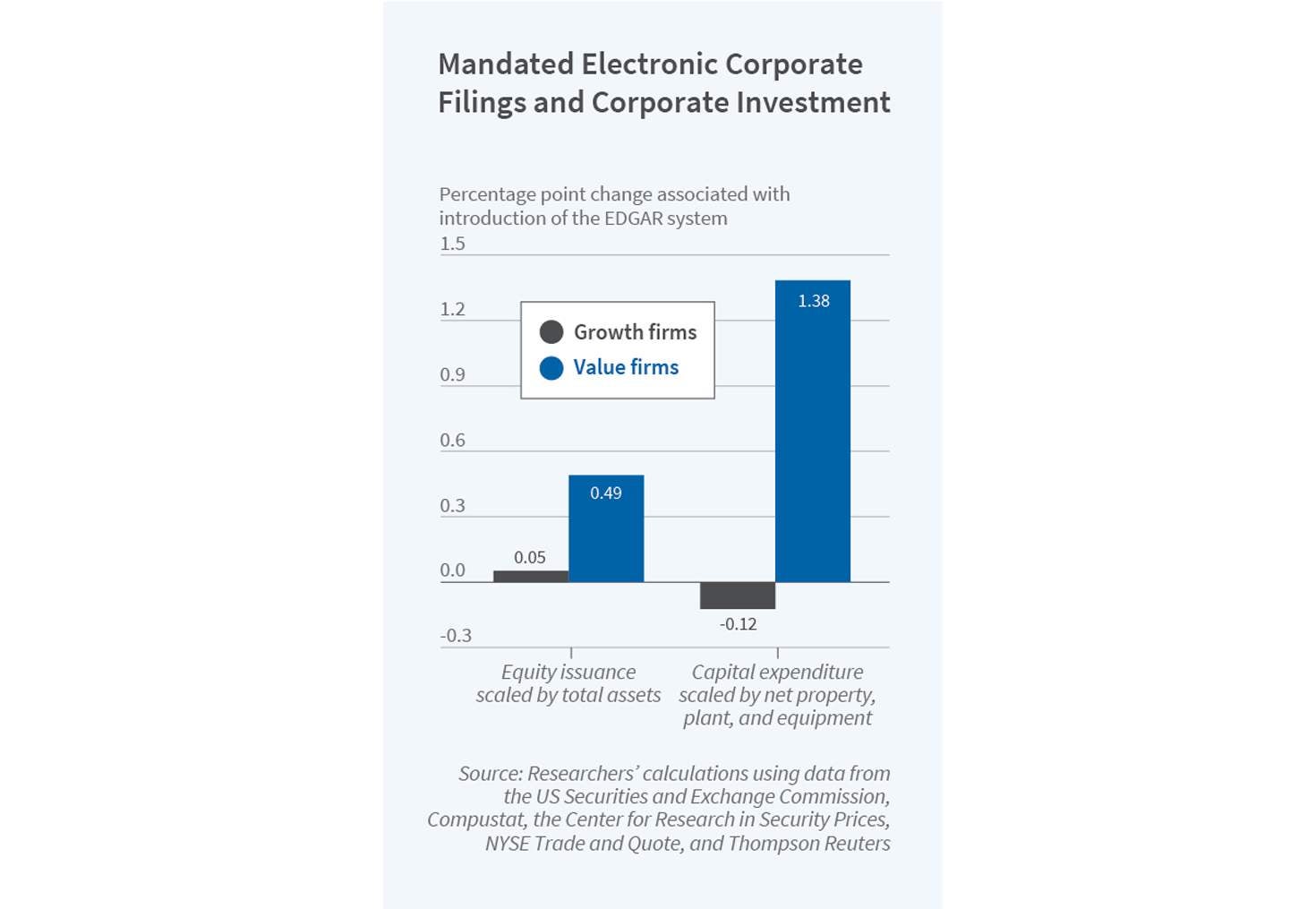

The researchers find that of the 3,020 firms in the study sample — which excluded financial firms, utilities, and companies worth less than $10 million — companies moving onto EDGAR saw a 10 percent rise in corporate investment but a 20 percent decline in investment-to-price sensitivity. A rise in equity finance contributed to the increase in corporate investment. The researchers conjecture that the reason for decreased investment-to-price sensitivity was that managers learned less from the price swings of their company’s stock because swings were based on more-democratized but less-precise analysis by market participants. This resulted in heterogeneous effects across firms: returns on value firms improved, while returns on high-growth firms, which are particularly dependent on market analysis, declined. “Our findings suggest that it is important to consider this tradeoff between financing and learning when evaluating the real effects of modern information technologies,” the researchers conclude.

The fall in investment-to-price sensitivity reflects a subtle information crowding-out effect. As traders begin to buy and sell stock in a company, they set share prices. Those prices reflect the traders’ private information, which even the company’s managers may not know. Managers can therefore learn from the share price. With expanded disclosure, however, less-sophisticated retail investors are on a more-level playing field with institutional investors. The researchers find that once a company becomes an EDGAR filer, it experiences a decrease in ownership by institutional investors. The rough pricing signals of the public disclosures provide enough information to make it less profitable, and therefore less likely, for institutional investors to engage in deeper analysis that would yield more precise signals about the firm’s fundamental value, and potentially inform the managers.

“This crowding-out effect happens because it takes time to develop high-precision signals and the trading profits based on these signals are reduced when low-precision signals have already been reflected in prices,” the researchers reason. Losing external deep analysis is more costly for managers of growth firms than of value firms, because traders’ potential information advantage lies in evaluating a company’s growth prospects. They can analyze its industry and competition, market trends, and consumer demand — information that, when reflected in share prices, can benefit growth-company managers.

— Laurent Belsie