Mortgage Shoppers: Beware of High-Cost Options

There is surprisingly little empirical evidence on how households choose among complex financial products such as mortgages. A key reason is the difficulty in determining the choice sets that borrowers face when selecting among potential loans. Usually, researchers see only the mortgage that the borrower ultimately chooses.

In Price Discrimination and Mortgage Choice (NBER Working Paper 31652), Jamie Coen, Anil K Kashyap, and May Rostom assemble a unique dataset that contains information on the mortgage options on offer at the bank where a loan was taken out and at other banks offering similar products. They establish a number of facts about mortgage selection and document the price dispersion on mortgage menus both within and across banks.

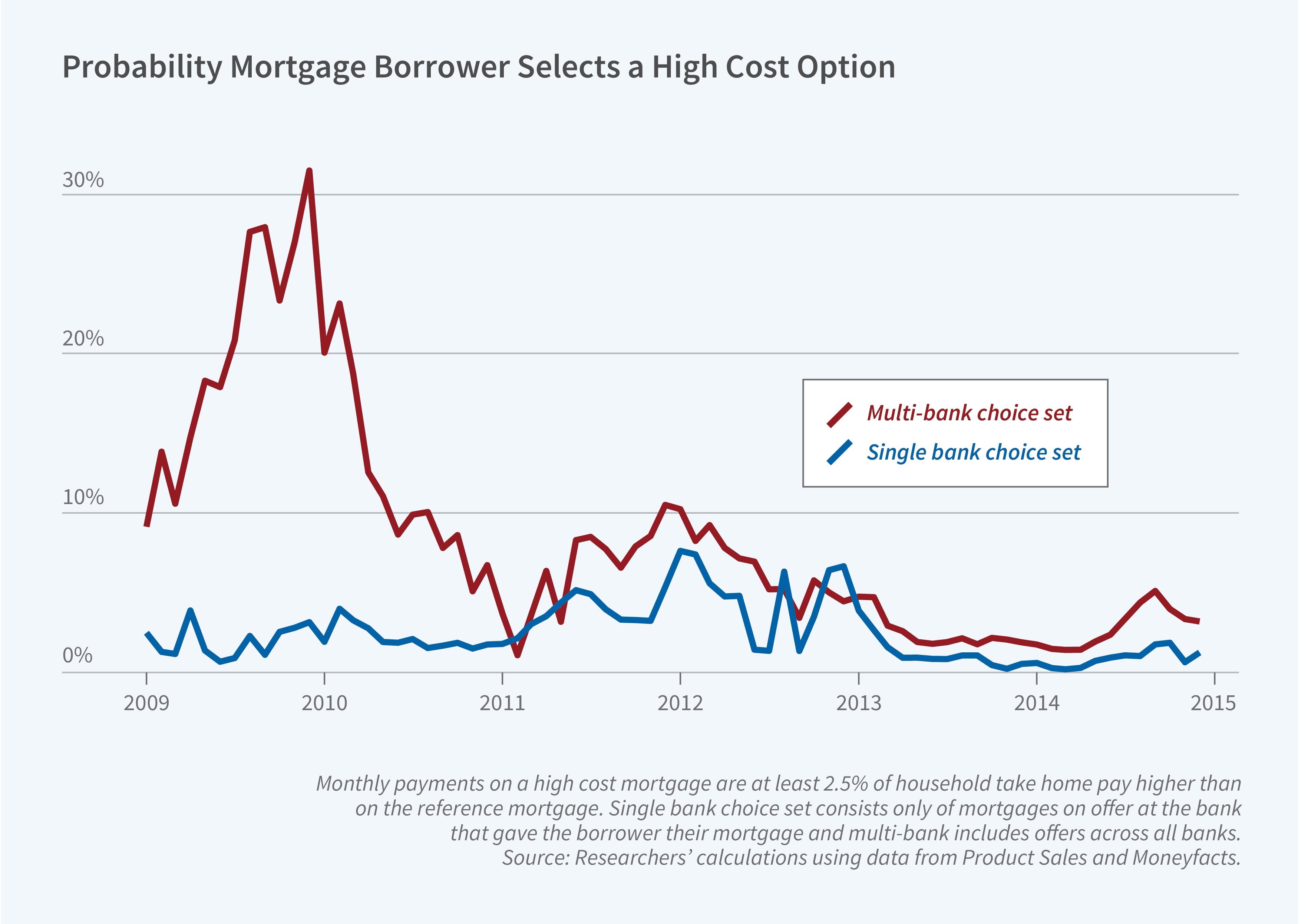

The choice sets show three recurrent patterns. First, all banks offer many mortgages with slightly different options. Second, most mortgages have nearly equivalent total costs to borrowers. Third, mixed into some menus are some very expensive choices which, if selected, would generate windfall profits for the banks. These patterns suggest that banks attempt to discriminate by price because they recognize that consumers are heterogeneous. Because they cannot legally tailor menus to individual characteristics, nor tell which customers are shopping at other lenders, they offer menus with options that cater to a wide range of borrower preferences.

While many mortgage offerings have nearly equivalent total costs to borrowers, some mortgage menus contain expensive choices that net windfall profits for lenders.

Though a bank may know that some customers are unable to identify the cheapest mortgage, it can only imperfectly target them. It must therefore post a menu that will not deter more sophisticated borrowers while potentially generating high profits from customers less able to identify cheaper loans. Even though customers rarely pick the cheapest products offered, in most cases the cost consequences are only modest.

Borrowers who pick expensive mortgages generally face poor menus with large price dispersion, the researchers find. Menus with many pricey options are more commonly offered to borrowers with higher loan-to-value and loan-to-income ratios, who are typically younger, more likely to be first-time buyers, and have lower incomes. Lenders thus try to price discriminate by making it easy for customers who might be prone to select badly to do so without scaring away other borrowers. Competition between lenders seems to explain why most borrowers can find a reasonable mortgage even if they do not pick particularly well, but about 7 percent of borrowers select a mortgage that is much more expensive than others in their choice set.

The researchers suggest that lenders may think of their clientele as consisting of two types of borrowers: sophisticated customers and randomizers. Randomizers walk into a bank and pick a random choice from the menu. They don’t shop at other banks, are unaware of alternatives, or don’t qualify for mortgages with other lenders. Sophisticated customers go to other banks, consider all options, and pick the cheapest available.

In this environment, lenders must balance two considerations: providing cheap options to entice sophisticated customers and offering expensive options to profit from randomizers. The menu will feature price dispersion, with good options for sophisticated customers and bad options for randomizers. The higher the percentage of randomizers, the more banks will want to fill the mortgage menu with bad options.

— Lauri Scherer

Kashyap thanks the Center for Research in Securities Prices and the Initiative on Global Markets at the University of Chicago Booth School of Business as well as the National Science Foundation for a grant administered by the National Bureau of Economic Research for research support.