How Do State Medigap Requirements Affect the Health of SSDI Beneficiaries?

Recipients of Social Security Disability Insurance (SSDI) benefits are eligible for Medicare after 24 months of benefit receipt. However, the insurance provided by Medicare to SSDI beneficiaries and the over-age-65 population is incomplete, as there are substantial deductibles and co-insurance requirements, and no lifetime cap on out-of-pocket spending. Many Medicare beneficiaries have another source of insurance to address this. One potential source for this coverage is a supplemental “Medigap” policy, a type of insurance that arose to meet the demand for wrap-around coverage for expenses not paid by Medicare.

How important are Medigap policies to the SSDI population? This is the subject of a new working paper by researchers Philip Armour and Claire O’Hanlon, “How Does Supplemental Medicare Coverage Affect the Disabled Under-65 Population? An Exploratory Analysis of the Health Effects of States’ Medigap Policies for SSDI Beneficiaries” (NBER Working Paper 25564).

States have policies governing the availability and allowable rates for Medigap policies for the under-65 population. These include “guaranteed issue” requirements that compel insurers to sell Medigap policies to under-65 beneficiaries who wish to purchase them, open enrollment requirements, and premium rating rules that require insurers to offer the same premiums to over-65 and under-65 beneficiaries or to all under-65 beneficiaries. The number of states with a guaranteed issue requirement has been rising over time, from 24 in 2004 to 32 in 2018. In states without a guaranteed issue requirement, Medigap policies may still be offered by insurers voluntarily.

The authors first document that these laws affect the availability of Medigap policies. In states with guaranteed issue, under-65 beneficiaries have access to an average of 126 Medigap policies, versus 24 in states without this requirement.

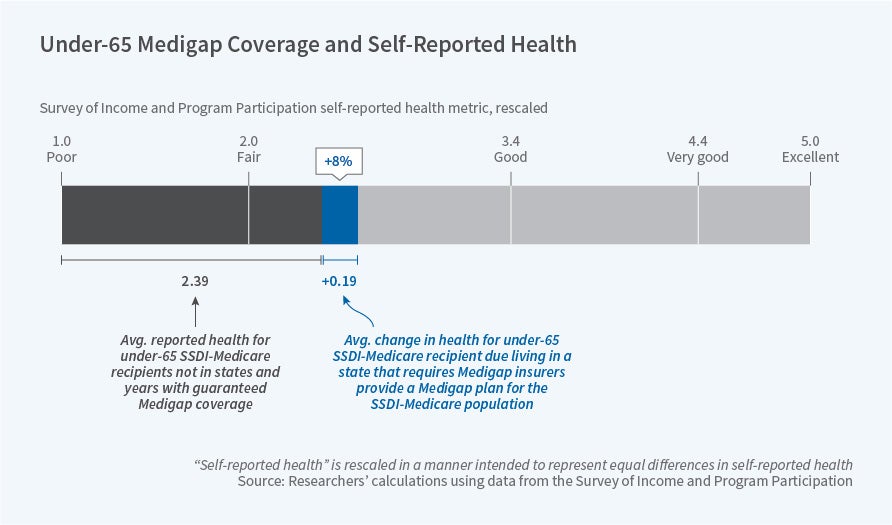

Next, the authors examine the effect of having a guaranteed issue requirement on self-reported health using data from the Survey of Income and Program Participation. They find that having a requirement is associated with a 0.19-point increase on a 5-point health scale (which ranges from poor to excellent health). This is a large effect relative to the mean score of 2.4 for those in non-guaranteed issue states. Put differently, this result implies that one in five SSDI beneficiaries report a one-point increase in health as a result of having guaranteed issue in their state.

The overall conclusion from this analysis is that “states’ requiring Medigap insurers to offer at least one Medigap plan to the under-65 Medicare population measurably and substantially improves this population’s health.” The authors note “the size of the impact on changes in health indicates that state-level Medigap policy has not just a comparable, but a substantially larger effect on health for under-65 Medicare beneficiaries than Medicaid expansion on the marginal Oregon Medicaid entrant.” Additional research will be required in order to estimate the effects of these Medicap policies on morbidity, mortality, and other health outcomes.

This research was supported by the U.S. Social Security Administration through grant #11DRC12000002-06 to the National Bureau of Economic Research as part of the SSA Disability Research Consortium.