Heterogeneous Mental Health Effects of Shocks to Housing Prices

US house prices fell by 34 percent between 2006 and 2012. But the downturn was more severe in some parts of the country than in others. For example, home values in Phoenix and Las Vegas dropped by 46 and 60 percent, respectively. In contrast, house prices in Pittsburgh and Buffalo didn’t fall at all, instead increasing by 5 and 6 percent over this time period.

How did the overall housing downturn, and the associated Great Recession, affect mental health among older adults? In Economic Crises and Mental Health: Effects of the Great Recession on Older Americans (NBER Working Paper 29817), David M. Cutler and Noémie Sportiche show that consequences varied with financial stability and race. To demonstrate these effects, the researchers compare changes in mental health in communities with greater house price reductions to changes in communities with smaller reductions.

Longitudinal data from the Health and Retirement Study between 2000 and 2016 allow the researchers to trace mental health over time for 9,425 adults aged 51 to 61, below typical retirement ages. The researchers match the data for each person to the annual housing price index, calculated by the Federal Housing Finance Agency, for the community where they lived prior to the recession.

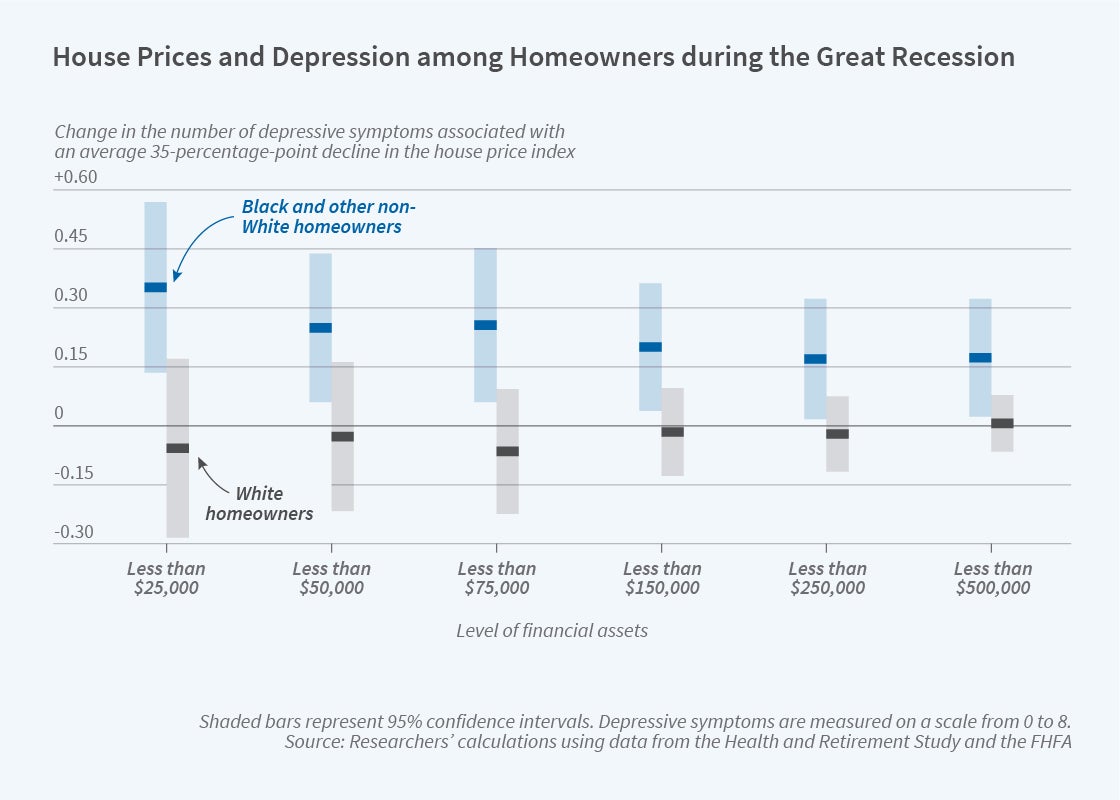

While the researchers discern no impact of the economic downturn on mental health outcomes for the average older adult, they find evidence of mental health consequences among less financially secure homeowners. Among those with less than $75,000 in financial assets, a decline in home values is associated with elevated rates of depression, with effects concentrated among Black and other non-White adults. Specifically, a 35 percent reduction in house prices is associated with 0.3 additional depressive symptoms (out of eight that were measured) and 0.2 additional functional limitations (out of seven that were measured) among Black and other non-White homeowners. While White homeowners did not exhibit increased symptoms of depression or functional limitations, they did increase their use of medications intended to treat anxiety or depression.

The figure shows how the impact on depression symptoms varies with financial assets. Among Black adults, the rise in depression symptoms is greatest at lower levels of financial assets but extends to higher financial asset levels. For White homeowners, there is little evidence of increased depression symptoms at any level of the wealth distribution.

The researchers interpret the change in housing prices as a measure of overall economic conditions, rather than only housing market conditions. They emphasize that the worsened health outcomes aren’t necessarily attributable to personal experiences with the housing market — such as foreclosures, deterioration of neighborhood conditions, or personal losses of housing wealth. Rather, their findings capture the overall effects of exposure to a distressed local housing market and the accompanying economic conditions, such as elevated unemployment.

While the researchers cannot identify the pathway through which falling house prices affect the mental health of these adults, they note that the mental health of adults just a few years older — senior citizens aged 65 to 74 — was unaffected by the change in the housing market. The researchers infer that mental health effects may be mediated by features of the labor or housing market that do not impact retirees or ameliorated by social insurance programs that are available to senior citizens.

The researchers acknowledge support from the US Social Security Administration through Grant #DRC 12000002-04 to the National Bureau of Economic Research as part of the SSA Retirement and Disability Research Consortium and the National Institute of Mental Health of the National Institutes of Health under Award Number T32MH019733.