Do Changes in the Stock Market Affect Retirement Decisions?

After posting record gains in the late 1990s, the US stock market fell dramatically starting in the year 2000. Over a twelve-month period, the benchmark S&P 500 Index lost one-quarter of its value and the NASDAQ Composite Index lost over sixty percent of its value.

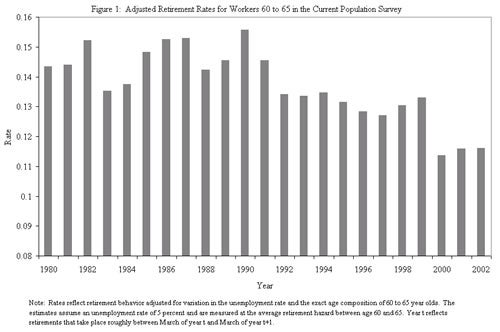

With more workers exposed to the stock market now than ever before, often through participation in 401(k)-type pension plans, it was widely predicted that the market drop would force many older workers to postpone retirement. In fact, as Figure 1 illustrates, retirement rates dropped by two percentage points in 2000, suggesting that such a re-sponse may have occurred.

In Bulls, Bears, and Retire-ment Decisions (NBER Working Paper 10779), Courtney Coile and Phillip Levine investigate the relationship between stock market performance and retirement behavior, paying particular attention to the boom and bust periods of the late 1990s and early 2000s. The authors use data from the Current Population Survey, the Health and Retirement Study, and the Survey of Consumer Finances.

The authors begin by noting reasons to be skeptical that Figure 1 reflects a causal relationship between stock market performance and retirement. First, retirement rates did not rise during the market boom of the late 1990s, even after adjusting for the effect of the strong economy. Second, as the sustained market decline only began in September 2000, the retirement response in late 2000 would had to have been very large to drive a two-point reduction for the year as a whole.

To determine the plausibility of a large response, the authors investigate the stock holdings of older households before the market decline. While two-thirds of these households had an individual retirement account (IRA) or 401(k)-type pension plan, fewer than half chose to invest it mostly or entirely in stocks. Moreover, typical stock holdings for these households were roughly equal to one year of household income. Thus for most families, even a sizeable drop in the stock market would result in a relatively small loss and be unlikely to trigger a change in retirement behavior.

To explore this point further, the authors make a simple calculation: assuming that households with no or very low stock assets did not change their retirement behavior as a result of the market crash in 2000, how large would the change in retirement behavior among stock-owning households had to have been to generate a two-point drop in retirement rates? They find that the response among these households would have to have been extremely (even implausibly) strong.

Next, the authors compare the effect of the stock market on the retirement behavior of individuals likely to have been differentially affected by changes in the market, such as people with and without 401(k)-type pension plans. If stock market performance affects retirement, then those who are more likely to own stocks should be more likely to retire in the boom period and less likely to retire during the bust.

The authors find little support for this hypothesis. On the contrary, the drop in retirement rates in the bust period is smaller for people who are more likely to own stocks. And there is no evidence of a greater rise in retirement rates in the boom period for those who are more likely to own stocks. The authors also fail to find any relationship between stock market exposure and labor force re-entry decisions.

The authors conclude that there is little evidence that the stock market affects retirement or labor force re-entry. They attribute this to the relatively small number of older workers with large stock holdings, noting that some individuals who experienced large gains or losses due to market fluctuations may certainly have responded. They point out that their results leave unexplained the drop in retirement rates in the year 2000 and suggest that the drop in wealth from the market crash may have been reflected primarily in changes in consumption and other behaviors.