The COVID-19 Pandemic and Innovation in Remote Work Technologies

In the spring of 2020, roughly half of all paid labor in the United States was performed from home. Although that share declined as the COVID-19 pandemic receded, the share of full paid workdays supplied remotely has remained over 25 percent since 2023, approximately four times the pre-pandemic level.

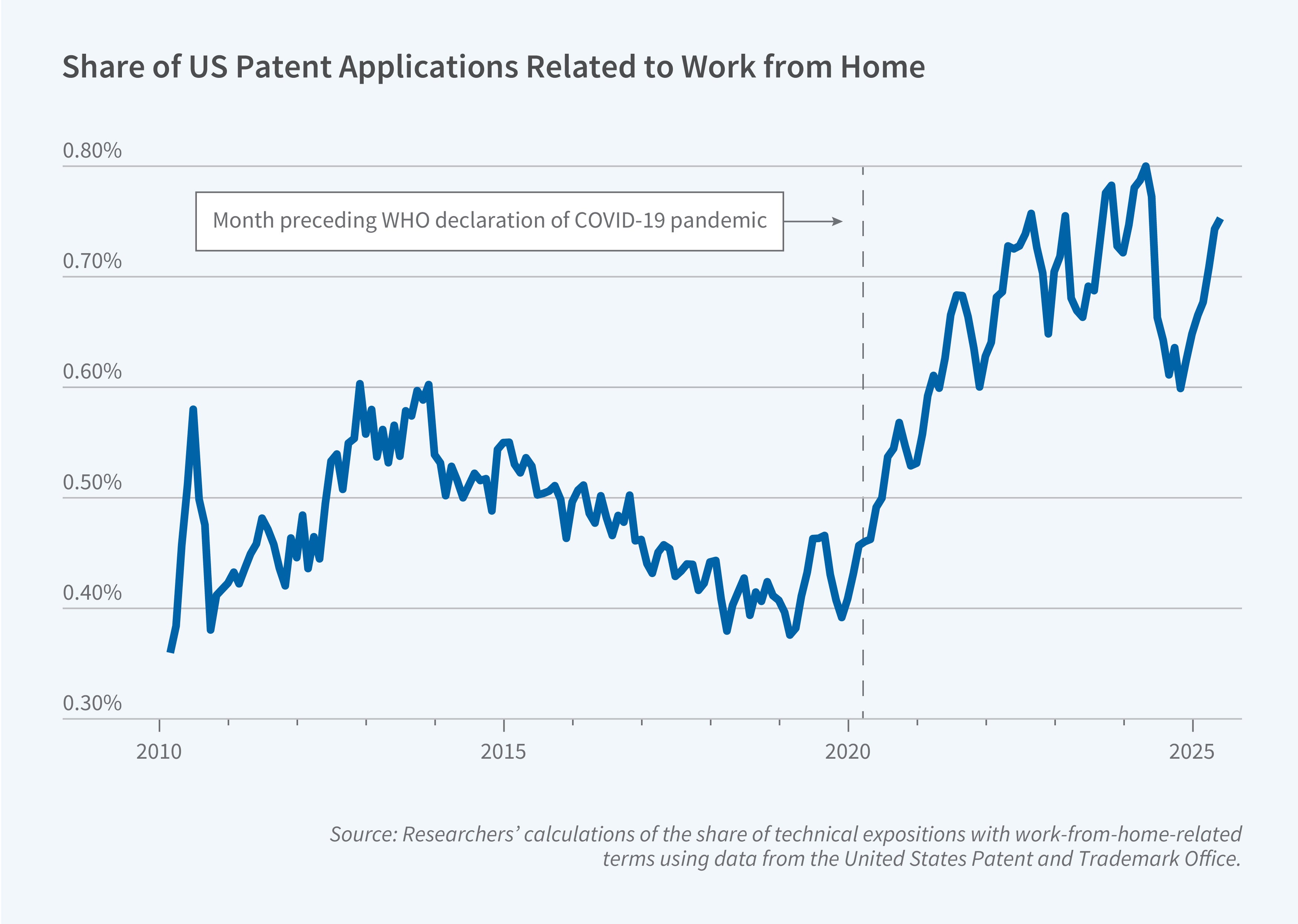

In Demand-Driven Technical Change: Evidence from WFH Technologies (NBER Working Paper 35083), Steven J. Davis, Nicholas Bloom, and Mihai A. Codreanu investigate whether the pandemic steered inventive activity toward technologies that facilitate working from home. They analyze the text of approximately 5.6 million US patent applications filed between January 2010 and July 2025 and published by March 2026. They construct a dictionary of 49 terms spanning four categories—communication and collaboration, remote access and digital infrastructure, home-based work, and flexible and mobile work—and search for these terms across patent titles, abstracts, claims, and descriptions. A patent application is classified as supporting work from home (WFH) if it contains at least one term from this dictionary.

The COVID-19 pandemic shifted innovation, particularly by corporations, toward technologies that are associated with remote work.

The share of patent applications advancing WFH technologies rose by approximately 60 percent in the three years following the start of the pandemic. As of mid-2025, the share was still more than 50 percent above its pre-pandemic level of 0.42 percent. The persistence of the higher patent share suggests that the rise in this share was not due only to firms rushing to patent nearly completed WFH innovations in the first few months of the pandemic.

The largest gains in patent activity appear in audio and speech processing, telecommunications, computing, healthcare IT, and optics. At a more granular level, video telephony and transmission, telephone exchange systems, speech recognition, and audio signal processing show the most pronounced increases. These are precisely the technology areas underpinning platforms such as Zoom, Microsoft Teams, and Cisco Webex.

Corporations drove the WFH innovation response, with their WFH patent share rising from roughly 0.5 percent to about 0.8 percent. Universities, in contrast, showed no discernible increase. This pattern is consistent with the theory that profit incentives, rather than curiosity-driven research agendas, drove the innovation response. Among individual firms, Zoom showed the largest absolute increase in WFH patent volume, followed by Huawei, Sony, Beijing Dajia Internet Information Technology, and Dell.

The researchers acknowledge support from the University of Chicago Booth School of Business, the Hoover Institution, Stanford Economics, and the Stanford Institute for Economic Policy Research.