Better Management Enables Better Tax Planning Too

Multinational manufacturing enterprises that are better at monitoring and planning production are likely also more adept at shifting their profits to low-tax countries.

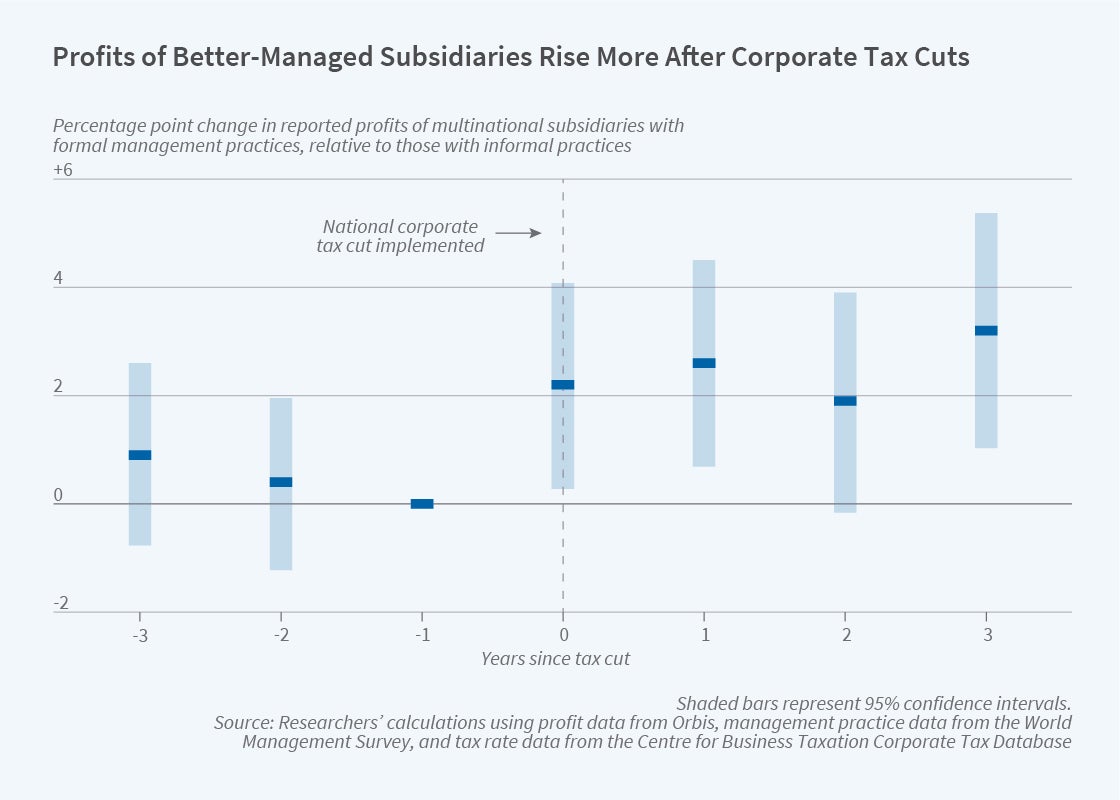

Better management leads to higher profits, but among multinational manufacturers this is primarily true for their operations in low-tax countries. In high-tax countries, better management is often associated with lower profits. The reason, according to a new study, seems to be profit shifting.

The researchers suggest that well-managed manufacturing firms that excel at regularizing and predicting production can make the necessary moves during the year to shift their paper profits from operations in high-tax to those in low-tax nations. The result is that many multinational enterprises (MNEs) in the manufacturing sector consistently report near-zero profits in high-tax nations while reporting high profits in low-tax nations, even though the productivity of their factories in both locales is high.

In Organizational Capacity and Profit Shifting (NBER Working Paper 29225), Katarzyna A. Bilicka and Daniela Scur find that the average MNE subsidiary in a country with a relatively low corporate tax rate of 22 percent reports a return on assets that is nearly 3 percentage points lower than a comparable subsidiary in a country with a relatively high 30 percent corporate tax rate.

By matching 15 years’ worth of information management practices with accounting data for nearly 1,400 MNEs operating in 21 countries, the researchers conclude that subsidiaries with certain management practices generate higher revenues, but that on average, those revenues do not translate into higher reported profits in high-tax nations. The type of management practice that most consistently correlates with low profits in high-tax nations is related to a firm’s ability to monitor production. While good managers can matter, the researchers argue that managers cannot shift profits without appropriate firm-wide structures. Profit-shifting ability also varies with the level of centralized decision-making.

One way to reduce a subsidiary’s tax burden is to take advantage of tax provisions such as investment incentives. Well-managed firms may be more effective at claiming tax relief that they are entitled to. Beyond that step, however, well-managed MNEs can use three common strategies to lower the overall tax burden across their networks of subsidiaries. These are debt shifting, transfer pricing, and patent location.

To shift debt, a subsidiary in a high-tax nation borrows money from a subsidiary in a low-tax one. The high-tax unit deducts the interest payments, reducing its profits, while the low-tax unit receives those payments, which are taxable, but at a lower rate than the deductions. Transfer pricing involves a high-tax unit buying intermediate products from a low-tax unit at inflated prices, thus reducing the profits of the high-tax unit and increasing those of the low-tax unit. Finally, firms may have some flexibility to locate their patents in a low-tax country. This means that the profits the patents generate are taxed at low rates. When subsidiaries in high-tax locations pay royalties on those patents to their low-tax counterparts, the royalty payments lower profits in the high-tax location and raise them in the low-tax one.

The researchers note that there are some limits to profit shifting: firms don’t want high-tax units to show losses, which might damage investor perceptions or trigger provisions in debt covenants. Transfer pricing may also be limited because, when goods are easily priced in other markets, tax authorities may challenge the tax-motivated pricing rules.

— Laurent Belsie