Program Report: Development Economics

The Development Economics (DEV) program was launched in 2012 and has 190 affiliated researchers. The success the program is enjoying today is in very large part thanks to Duncan Thomas, who led the program for its first six years. A unique aspect of the program is its close connections with BREAD, the Bureau for Research and Economic Analysis of Development, which is an independent group with worldwide membership. Our fall program meeting is held jointly with BREAD every other year.

Development economics is, broadly speaking, the study of two questions. First, why are some countries poor while other countries are wealthy? Second—and this is a vast topic which comprises much of the group’s research—how do the particular circumstances of low- and middle-income countries shape the functioning of markets and other types of economic activities? Put another way, for the many areas we study in economics and for which NBER programs exist—such as labor, health, industrial organization, and the environment—how are the economics different in countries that are typically poorer, with more informality and often a weaker institutional sector than in wealthy countries?

These broad questions have been studied for decades, but the specific focus of the research is constantly evolving. Our goal in this summary is to take stock of themes that have emerged or become more central to the program’s work in the period since the last Development Economics Program Report in 2018.

We began this piece by considering which substantive themes have been most prominent in recent years. Our holistic assessment of the field is based on helping to organize and participating in NBER conferences, and reading new NBER Working Papers over this period. We don’t claim that our summary is definitive or exhaustive; we highlight four themes that stood out for us as illustrative of the exciting research happening in development economics.

We then conducted an experiment to see how our assessment of the prominent research topics in this program compared to that of a generative AI model. After finalizing our summary, we uploaded the titles, authors, and abstracts of all 1,972 NBER Working Papers in the DEV program from its inception through the end of 2025 to ChatGPT version 5.2.

We report our summary and then ChatGPT’s summary below, followed by its answers to two bonus questions we asked it about trends within the program, specifically which themes have become less prominent over time and what the important methodological pivots have been.

Program Directors’ Summary: Four Important Themes

One theme that has received substantial attention is the design of anti-poverty social protection programs and their impacts. This has been a long-standing area of interest in development economics, but activity has surged in recent years. Many recent studies examine cash transfers, which have become more widespread in part because the expansion of mobile money and electronic banking has simplified the logistics of delivering them. As one example, Dennis Egger, Johannes Haushofer, Edward Miguel, Paul Niehaus, and Michael Walker study the impacts of unconditional cash transfers provided to households in rural Kenya using a research design that can capture the general equilibrium effects of the transfers and quantify the multiplier effect that arises as the transferred money ricochets through the local economy.1

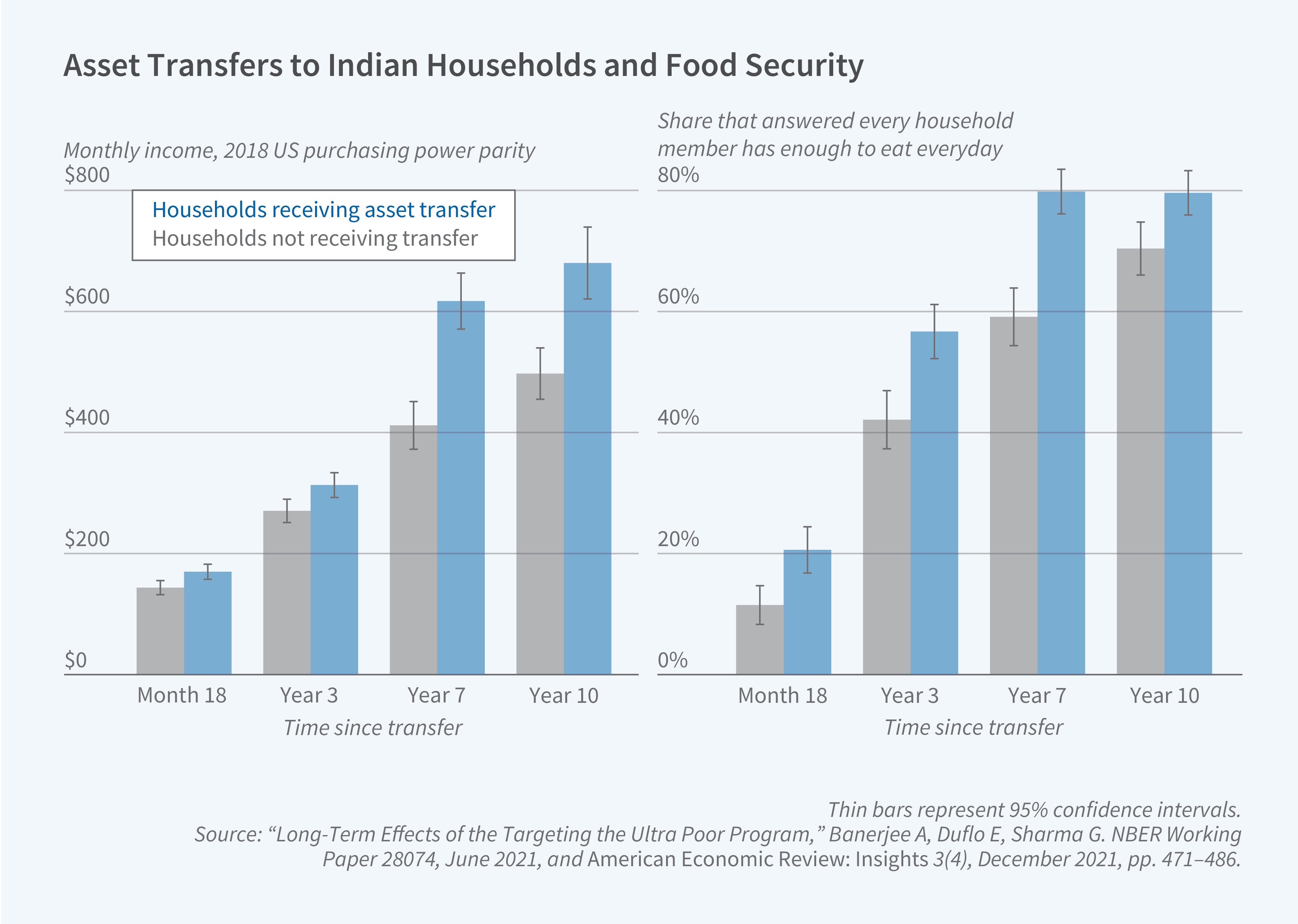

Among non-cash transfer programs, one that gained attention a decade ago is the multifaceted “graduation” program pioneered by the Bangladeshi nonprofit BRAC. In recent years, researchers have analyzed long-run effects of the program, for example, as done by Abhijit Banerjee, Esther Duflo, and Garima Sharma for India; conducted multi-arm randomized trials to understand which components of the multifaceted program are crucial and which might be extraneous, for example, as done by Emily Beam, Lasse Brune, Narayan Das, Stefan Dercon, Nathanael Goldberg, Rozina Haque, Dean Karlan, Maliha Khan, Doug Parkerson, Ashley Pople, Yasuyuki Sawada, Christopher Udry, and Rocco Zizzamia for Ghana; and used the program as a laboratory to test whether households face poverty traps, as done by Clare Balboni, Oriana Bandiera, Robin Burgess, Maitreesh Ghatak, and Anton Heil for Bangladesh.2,3,4

Another active area within social protection is targeting, or identifying which households should be beneficiaries. Researchers have investigated machine-learning approaches that target the expected gains from treatment (Johannes Haushofer, Paul Niehaus, Carlos Paramo, Edward Miguel, and Michael W. Walker), elicitation of the community’s opinion (Sudarno Sumarto, Elan Satriawan, Benjamin A. Olken, Abhijit Banerjee, Achmad Tohari, Vivi Alatas, and Rema Hanna), and workfare-type schemes (Marianne Bertrand, Bruno Crépon, Alicia Marguerie, and Patrick Premand), for example.5,6,7 This literature highlights that a policymaker’s choice about whom to target often is a balancing act among cost and other practicalities, multiple program goals, distributional concerns, and tolerance for errors of inclusion versus errors of exclusion.

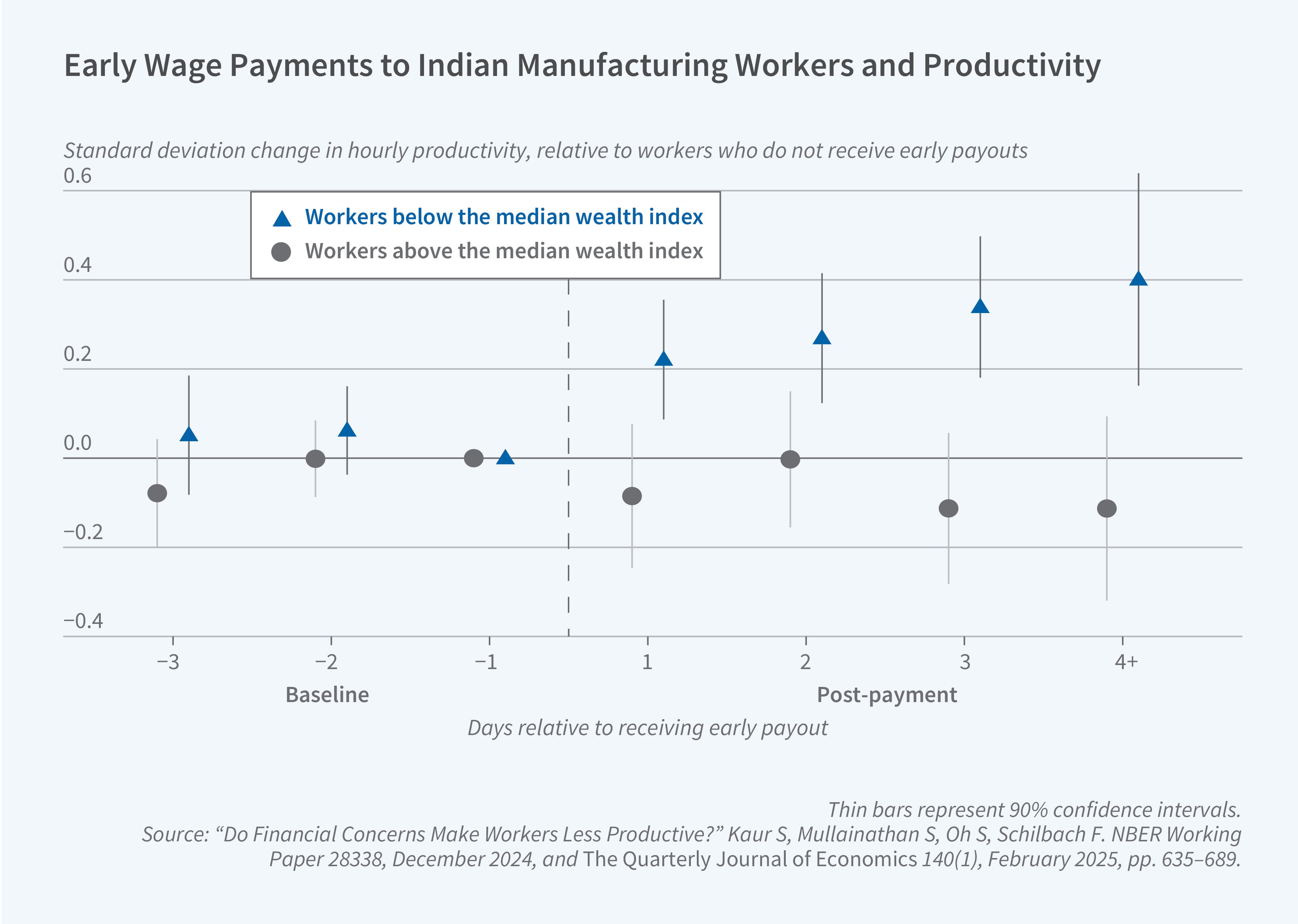

A second theme that has emerged in recent years is the psychology of poverty, or how poverty affects cognition and mental health. For example, Supreet Kaur, Sendhil Mullainathan, Suanna Oh, and Frank Schilbach use an intricately designed experiment in India to document how financial worries occupy workers’ thoughts while they are on the job and dampen their performance; cash-rich workers are more productive workers.8 Francis Annan and Belinda Archibong provided mobile phone credit to individuals in Ghana during the COVID-19 pandemic and found that doing so reduced recipients’ psychological distress.9

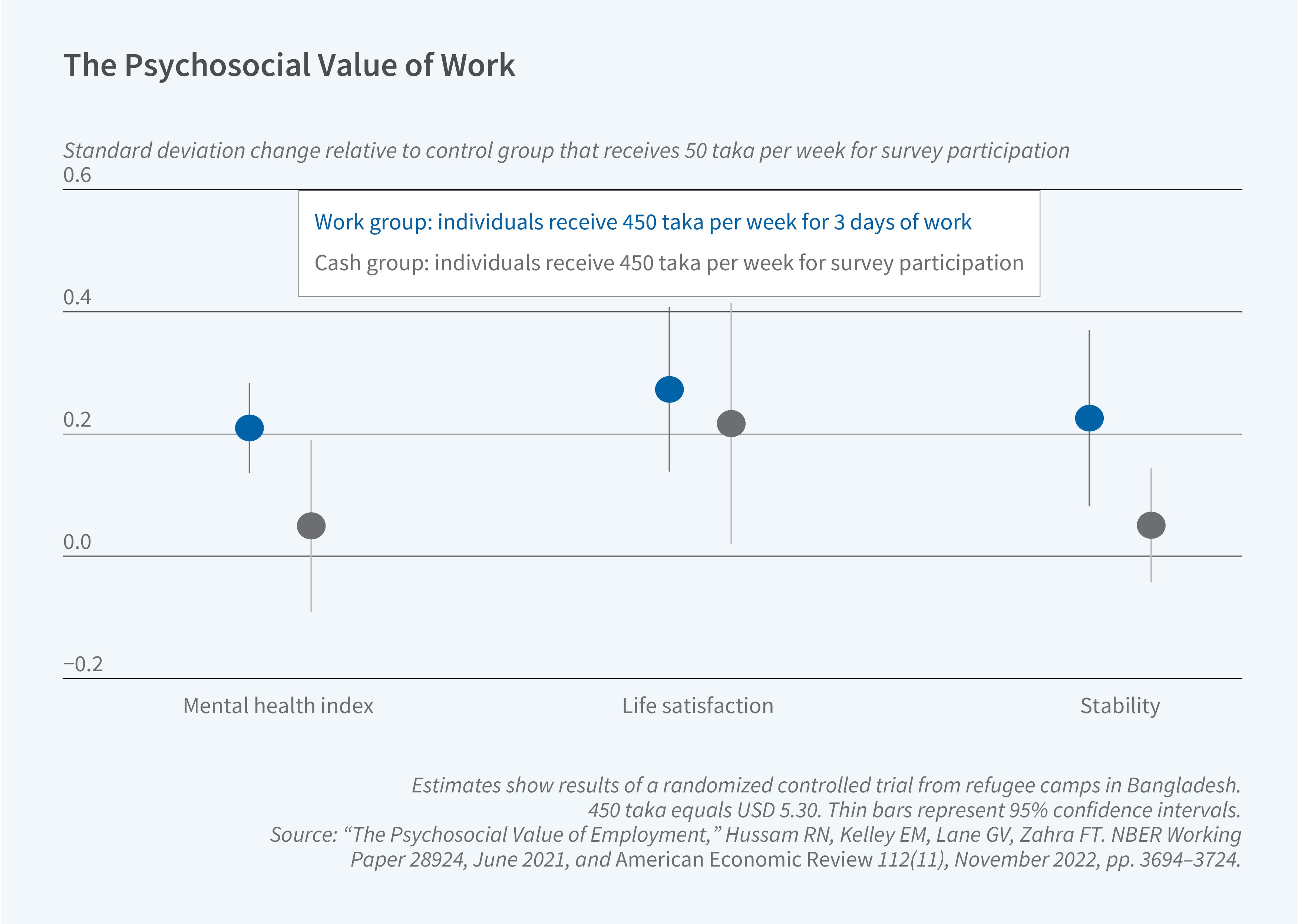

Researchers are also increasingly studying mental health problems, which often go undiagnosed and untreated in low- and middle-income countries. Nathan Barker, Gharad Bryan, Dean Karlan, Angela Ofori-Atta, and Christopher Udry find that cognitive behavioral therapy improved mental health, cognition, and physical health among a general population of poor households in Ghana, suggesting that mental health interventions can improve human capital and economic outcomes.10 Scholars are also increasingly collecting data on mental health outcomes to enrich our understanding of how policies can improve (or harm) people’s welfare. For example, Reshmaan Hussam, Erin Kelley, Gregory Lane, and Fatima Zahra show that providing employment opportunities to individuals residing in refugee camps in Bangladesh improves their mental health (e.g., reduces depression) more than giving them an income-equivalent cash transfer does.11

A third theme has been the collection of microdata to answer macroeconomic questions related to development, as highlighted by Francisco Buera, Joseph Kaboski, and Robert Townsend.12 Sometimes the goal is to measure the general equilibrium effects of policies, as mentioned above when discussing cash transfers under the theme of social protection. Another example comes from Lauren Bergquist, Craig McIntosh, and Meredith Startz, who quantify the effects of improved market integration resulting from the use of a matching platform that reduces search costs for buyers and sellers in agricultural markets in Uganda.13 David Atkin, Baptiste Bernadac, Dave Donaldson, Tishara Garg, and Federico Huneeus use comprehensive microdata on firms, workers, and purchases to understand who bears the ultimate incidence of distortions throughout the economy.14

The micro-macro approach has also been used to study poverty traps caused by lumpy capital goods that could increase productivity. An important drag on growth could stem from small firms being unable to achieve sufficient scale to cover fixed costs. Researchers have explored whether rental markets allow these capital costs to be smoothed over many small firms; Julieta Caunedo and Namrata Kala study this in agriculture in India, and Vittorio Bassi, Raffaela Muoio, Tommaso Porzio, Ritwika Sen, and Esau Tugume study it for manufacturing firms in Uganda.15,16 Small firms still might have preferences for larger, lumpier investments, as shown by Joseph Kaboski, Molly Lipscomb, Virgiliu Midrigan, and Carolyn Pelnik, but the findings on capital rental markets suggest that indivisibilities at the individual level may not pose as large an aggregate constraint as one may have thought.17

A fourth theme is the increasing work at the intersection of environmental economics and development economics. Much of this work is on climate change, which is projected to be particularly devastating in low- and middle-income countries. The harms from climate change are myriad. Water scarcity is upending the norms of coexistence between pastoralist and agricultural communities in Africa, as evidenced by increasing intergroup conflict, examined by Eoin McGuirk and Nathan Nunn.18 How households and communities adapt to climate change and counteract the harms is critically important, and researchers are beginning to make progress on this. For example, Jenny Aker and Kelsey Jack study the barriers farmers in Niger face in adopting rainwater harvesting techniques that can help prevent the soil degradation and desertification brought about by climate change.19 Climate change will also make weather more variable in many places, and Fiona Burlig, Amir Jina, Kelley, Gregory Lane, and Harshil Sahai study whether access to accurate weather forecasts can help farmers in India prepare and tailor their actions to the likely realized weather.20

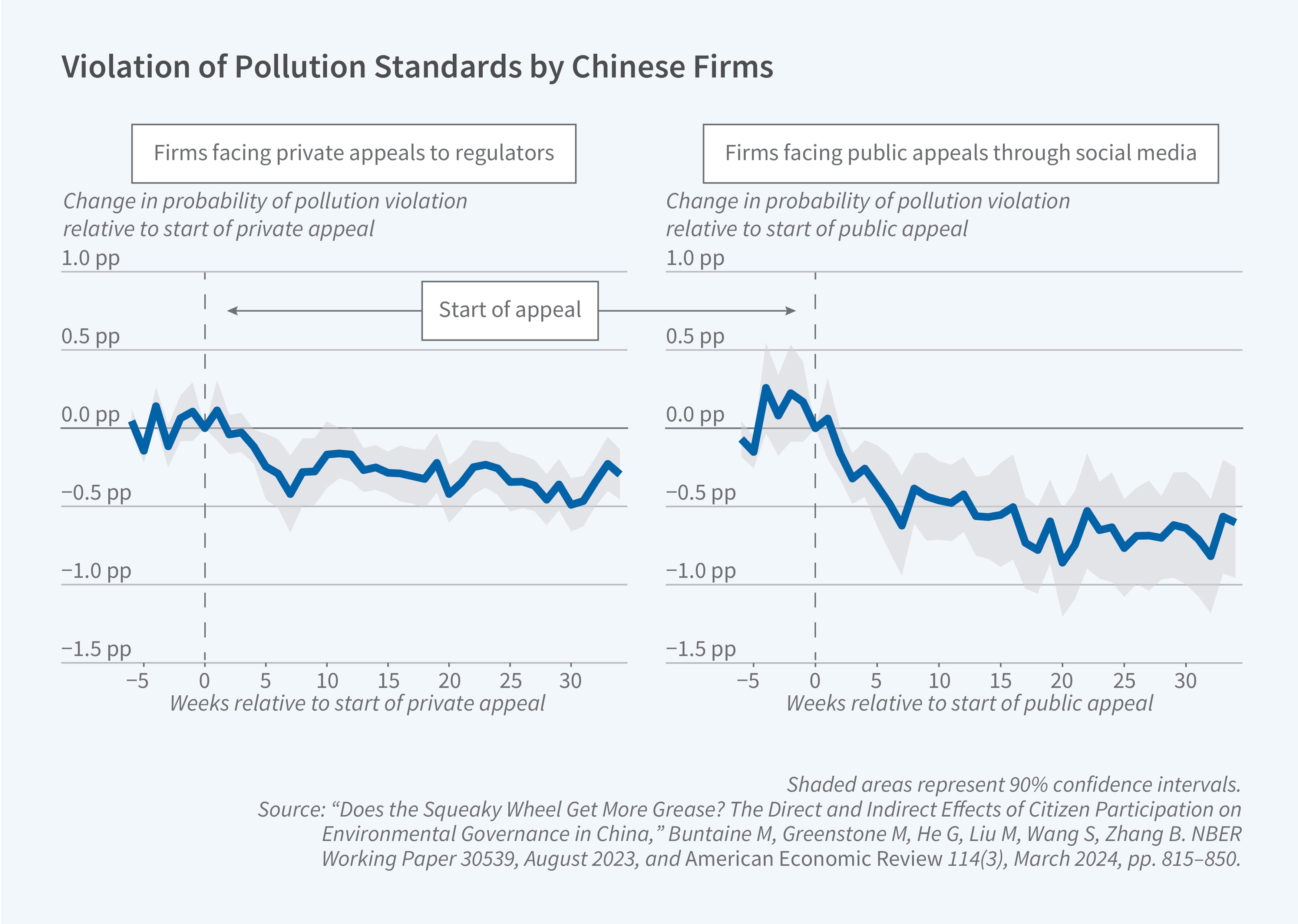

Another topic at the development-environment nexus is the importance of political economy considerations. Nicholas Ryan and Anant Sudarshan explore an equity-efficiency trade-off in relation to a policy in India that manages groundwater use through rations rather than prices.21 Mark Buntaine, Michael Greenstone, Guojun He, Mengdi Liu, Shaoda Wang, and Bing Zhang look at the role of citizen complaints in addressing pollution through a nationwide randomized controlled trial in China and find that public complaints posted on social media led to measurable reductions in pollution, whereas equivalent complaints submitted directly to the government, but not posted on social media, do not lead to such reductions.22 At a more aggregate level, Allan Hsiao, Jacob Moscona, and Karthik Sastry show that countries adjust their trade policy in response to climate-induced shocks to food productivity, particularly in election years. Although attempting to protect local farmers, this endogenous policy response limits the degree to which domestic consumers can benefit from improvements in foreign productivity and, on net, substantially reduces welfare for consumers in poor countries.23

Generative AI Summary: Four Important Themes24

ChatGPT delivered an alternative synthesis of the program. The prompts we used to generate the content below are available in the endnotes. While its summary highlights slightly different themes than our review, we are struck by the degree to which it is consistent with our assessment. The four main themes it suggested, reproduced verbatim, are:

“State Capacity, Governance, and Public Sector Effectiveness

A defining theme of DEV research since 2018 is a renewed focus on the state itself—how governments function, where they fail, and how capacity can be built. Papers study bureaucratic incentives, tax administration, procurement, regulation, and service delivery using administrative data and field experiments. Rather than treating weak institutions as fixed background conditions, this literature analyzes specific mechanisms—monitoring, incentives, information systems—that shape public-sector performance. The shift is toward actionable evidence on how governments in low- and middle-income countries can implement policy effectively at scale.

Social Protection, Redistribution, and Targeting

Another central theme is the expansion and evaluation of social protection systems, especially cash transfers, in-kind benefits, and emergency assistance. Research in this period examines targeting accuracy, spillovers, labor supply effects, and political economy constraints. A notable development is the use of large administrative datasets to study national programs rather than small pilots, allowing analysis of scale, general equilibrium effects, and long-run outcomes. This work is closely connected to pandemic-era expansions of safety nets but extends beyond them to questions of permanent redistribution and fiscal sustainability.

Firms, Productivity, and Structural Transformation

DEV research from 2018–2025 places increasing emphasis on firms and markets as engines of growth. Papers study misallocation, management practices, access to finance, supply chains, and market power, often combining experimental interventions with administrative and transaction data. Rather than viewing development as a simple shift from agriculture to manufacturing, the literature emphasizes services, informality, and within-sector productivity gains. Structural transformation is treated as a complex, firm-level process shaped by institutions, competition, and policy.

Human Capital, Early-Life Interventions, and Long-Run Impacts

Human capital remains a core area, but the focus has shifted toward long-run and intergenerational effects. Research evaluates education, health, nutrition, and early-childhood interventions with extended follow-up horizons, often linking experimental or quasi-experimental variation to adult outcomes. A key feature of this literature is its integration of administrative records—schooling, earnings, health—to assess persistence and heterogeneity of impacts. The emphasis is less on test scores alone and more on lifetime welfare, inequality, and mobility.”

Further AI-based Program Insights

We also gave ChatGPT two additional prompts. One was to identify themes that were central to the program in its first five years but have become less of a focus today. Here is the answer:

“Microcredit and Household Finance as Standalone Growth Tools

In the early DEV years, a large share of papers focused on microcredit, savings products, and household financial access as primary levers for poverty reduction. These studies often evaluated take-up, short-run consumption smoothing, and small business investment. While financial inclusion remains relevant, recent DEV research has largely moved away from treating microfinance as a transformative growth engine, instead embedding finance within broader analyses of firms, markets, and state capacity.

Agricultural Technology Adoption in Isolation

Between 2013 and 2017, many DEV papers examined adoption of specific agricultural inputs—fertilizer, seeds, irrigation—often via small-scale randomized trials. In the 2021–2025 period, agriculture is more likely to appear within integrated studies of land use, climate risk, value chains, or structural transformation, rather than as isolated input-adoption problems. The emphasis has shifted from “why don’t farmers adopt X?” to how agriculture fits into economy-wide development paths.

Education Interventions Measured Primarily by Test Scores

Earlier DEV research devoted substantial attention to education interventions evaluated using short-run learning outcomes, especially test scores. While education remains central, recent work places less weight on test scores alone and more on long-run, labor-market, and intergenerational outcomes. The decline is not in interest, but in the dominance of narrowly defined schooling metrics as endpoints.

Informality as a Binary Condition

In the early period, informality was often treated as a binary state—formal versus informal firms or workers—with policy aimed at formalization per se. More recent DEV work treats informality as a spectrum, focusing on productivity, firm capabilities, enforcement, and the costs and benefits of remaining informal. This reflects a shift from classification toward mechanism and policy design.”

Finally, we asked the AI tool to describe some of the main methodological pivots between 2013–17 and 2021–25. Here is its answer:

“From Small-Scale RCTs to Administrative Data at Scale

In 2013–2017, DEV research was dominated by village- or household-level randomized controlled trials, often designed to answer tightly framed questions about take-up or short-run behavior. By 2021–2025, RCTs are still important but are increasingly complemented—or replaced—by large administrative datasets covering millions of individuals, firms, or transactions. This shift enables researchers to study national programs, policy implementation, and long-run outcomes, moving DEV from proof-of-concept experiments toward evaluation at scale.

Greater Emphasis on Long-Run and Dynamic Effects

Earlier DEV work often relied on short follow-up windows due to data constraints, emphasizing immediate impacts on consumption, inputs, or test scores. Recent research designs are explicitly dynamic, linking experimental or quasi-experimental variation to outcomes years later using administrative records. This allows credible analysis of persistence, fade-out, and intergenerational effects, fundamentally changing how interventions are judged.

Integration of Quasi-Experimental Designs with Rich Data

While causal inference was already central in 2013–2017, identification strategies have grown more sophisticated. The 2021–2025 literature frequently combines administrative data with natural experiments—policy thresholds, staggered rollouts, enforcement variation—using modern event-study and difference-in-differences frameworks. This reduces reliance on pure randomization while expanding the policy questions that can be addressed.

Measurement Innovation and Machine Learning

A notable methodological advance is the use of machine learning and new data sources to construct key variables—poverty proxies, firm productivity, targeting scores, or climate exposure. In earlier work, measurement was often coarse and survey-based. Recent DEV papers use ML as a complement to causal designs, improving precision and external validity without abandoning identification discipline.”

As with the summary of recent themes, we found ChatGPT’s answers interesting and broadly consistent with our own assessments.

Endnotes

General Equilibrium Effects of Cash Transfers: Experimental Evidence from Kenya” Egger D, Haushofer J, Miguel E, Niehaus P, Walker MW. NBER Working Paper 26600, October 2021, and Econometrica 90(6), November 2022, pp. 2603–2643.

Long-Term Effects of the "Targeting the Ultra Poor" Program, Banerjee A, Duflo E, Sharma G. NBER Working Paper 28074, June 2021, and American Economic Review: Insights 3(4), December 2021, pp. 471–486.

“Group versus Individual Coaching for Rural Social Protection Programs: Evidence from Uganda, Philippines, and Bangladesh,” Beam EA, Brune L, Das N, Dercon S, Goldberg N, Haque R, Karlan D, Khan M, Parkerson D, Pople A, Sawada Y, Udry C, Zizzamia R. NBER Working Paper 34309, October 2025.

Why Do People Stay Poor? Balboni CA, Bandiera O, Burgess R, Ghatak M, Heil A. NBER Working Paper 29340, October 2021, and The Quarterly Journal of Economics 137(2), May 2022, pp. 785–844.

Targeting Impact versus Deprivation, Haushofer J, Neihaus P, Paramo C, Miguel E, Walker MW. NBER Working Paper 30138, December 2022.

Community Targeting at Scale, Sumarto S, Satriawan E, Olken BA, Banerjee A, Tohari A, Alatas V, Hanna R. NBER Working Paper 33322, January 2025.

Do Workfare Programs Live Up to Their Promises? Experimental Evidence from Côte d’Ivoire, Bertrand M, Crépon B, Marguerie A, Premand P. NBER Working Paper 28664, April 2021.

Do Financial Concerns Make Workers Less Productive? Kaur S, Mullainathan S, Oh S, Schilbach F. NBER Working Paper 28338, December 2024.

The Value of Communication for Mental Health, Annan F, Archibong B. NBER Working Paper 31638, August 2023.

Mental Health Therapy as a Core Strategy for Increasing Human Capital: Evidence from Ghana, Barker N, Bryan GT, Karlan D, Ofori-Atta A, Udry CR. NBER Working Paper 29407, October 2021.

The Psychosocial Value of Employment, Hussam RN, Kelley EM, Lane GV, Zahra FT. NBER Working Paper 28924, June 2021.

From Micro to Macro Development, Buera FJ, Kaboski JP, Townsend RM. NBER Working Paper 28423, February 2021, and Journal of Economic Literature 61(2), June 2023, pp. 471–503.

Search Costs, Intermediation, and Trade: Experimental Evidence from Ugandan Agricultural Markets, Bergquist LF, McIntosh C, Startz M. NBER Working Paper 33221, December 2024.

The Incidence of Distortions, Atkin D, Bernadac B, Donaldson D, Garg T, Huneeus F. NBER Conference Paper presented at the BREAD/Development Economics Program Meeting, Fall 2025.

Mechanizing Agriculture, Caunedo J, Kala N. NBER Working Paper 29061, July 2022.

Achieving Scale Collectively, Bassi V, Muoio R, Porzio T, Sen R, Tugume E. NBER Working Paper 28928, June 2021, and Econometrica 90(6), November 2022, pp. 2603–2643.

How Important Are Investment Indivisibilities for Development? Experimental Evidence from Uganda, Kaboski J, Lipscomb M, Midrigan V, Pelnik C. NBER Working Paper 29773, February 2022.

Transhumant Pastoralism, Climate Change, and Conflict in Africa, McGuirk EF, Nunn N. NBER Working Paper 28243, May 2021.

Harvesting the Rain: The Adoption of Environmental Technologies in the Sahel, Aker JC, Jack K. NBER Working Paper 29518, November 2021.

The Value of Forecasts: Experimental Evidence from India, Burlig F, Jina A, Kelley EM, Lane GV, Sahai H. NBER Working Paper 32173, July 2025.

Rationing the Commons, Ryan N, Sudarshan A. NBER Working Paper 27473, July 2020, and Journal of Political Economy 130(1), January 2022, pp. 210–257.

Does the Squeaky Wheel Get More Grease? The Direct and Indirect Effects of Citizen Participation on Environmental Governance in China, Buntaine M, Greenstone M, He G, Liu M, Wang S, Zhang B. NBER Working Paper 30539, August 2023, and American Economic Review 114(3), March 2024, pp. 815–850.

Food Policy in a Warming World, Hsiao A, Moscona J, Sastry K. NBER Working Paper 32539, January 2026.

We uploaded the NBER Working Paper metadata (available at https://www.nber.org/research/data/nber-working-papers-and-chapters-metadata) to ChatGPT 5.2 (using a professional license that does not update ChatGPT’s model with uploaded data). We refined the prompts using test data from other programs (Labor Studies and Energy and Environmental Economics) but did not run it on the Development Economics corpus until our own summary above had been finalized. The three prompts that were used for ChatGPT are as follows:

1. Please summarize the 4 most important distinct topics and themes of research in this area during the period from 2018-2025 from the NBER .dta files uploaded. You can use a numbered list and subheadings, but within each subheading please give your answers in complete paragraphs, not bullet points. Your total answer should be less than 500 words. Can you try to make the writing style engaging to the reader yet concise.

2. Which 4 themes were central in 2013-2017 that are less central in the 2021-2025 period? Use the NBER .dta files uploaded. You can use a numbered list and subheadings, but within each subheading please give your answers in complete paragraphs, not bullet points. Your total answer should be less than 250 words. Can you try to make the writing style engaging to the reader yet concise.

3. How do the main methodologies and research design approaches used in the 2021-2025 period compare to the main methodologies used 2013-2017? Use the NBER .dta files uploaded. What are key methodological advances or changes? You can use a numbered list and subheadings, but within each subheading please give your answers in complete paragraphs, not bullet points. Your total answer should be less than 250 words. Can you try to make the writing style engaging to the reader yet concise.