When Financing Terms Are Generous, Car Buyers Pay More

When prospective buyers have access to longer-term loans with lower monthly payments, the transaction prices for automobiles increase.

The supply of auto loans, and the terms of these loans, play a central role in the auto market. The relationships between the behavior of lenders, auto dealers, and consumers are complex. In The Capitalization of Consumer Financing into Durable Goods Prices (NBER Working Paper No. 24699) Bronson Argyle, Taylor D. Nadauld, Christopher Palmer, and Ryan D. Pratt examine one aspect of this market. They test whether consumers pay more for used cars when they have access to loans that allow a longer time for repayment. All else constant, they find that a 12-month reduction in the term available for loan repayment is associated with about a 3 percent decline in the selling price for the car.

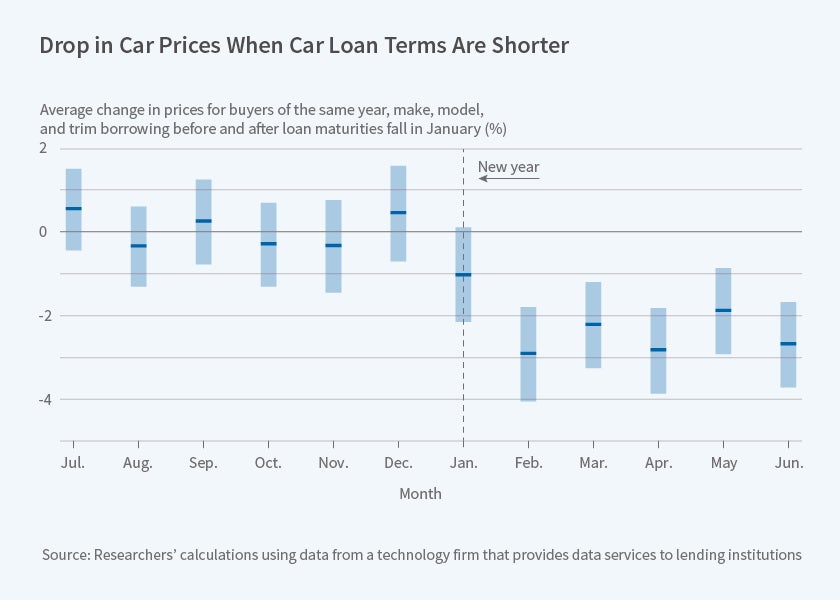

The researchers recognize that the maturity of the auto loan that a potential buyer can access depends on many factors. For example, most lenders reduce the maturity of the loans they offer as the age of the car increases. However, many lenders reduce their maximum loan length offer at the beginning of the calendar year, resulting in different repayment requirements for otherwise identical cars purchased just a few weeks apart. A loan for a car in December may allow a 72-month maximum period for repayment, but a loan for the same car in early January may require repayment within 60 months. The researchers use this discontinuity in loan terms to compare prices paid by consumers who have access to loans of different maturities, even though they and the cars they are buying are otherwise similar. They find that borrowers pay about 3.6 percent less for their cars when the loan maturity they are offered declines by 12 months. Auto dealers are able to charge more when consumers have access to more generous credit that lowers their monthly payment for a given purchase price.

The researchers consider the confounding possibility that those given shorter maturities receive different interest rates. They find that interest rates are higher on loans of longer maturity, by 24 basis points per month. However, interest rate variation explains only 20 percent of the change in the price variation across year end; changes in loan maturity account for the other 80 percent. After allowing for the effect of loan maturity on interest rates, they find that being offered a 12-month shorter maturity loan is associated with a 2.8 percent decline in the purchase price. They interpret this as evidence that buyers who are offered shorter-maturity loans, with correspondingly higher monthly payments, value the car-cum-loan package less than those who have access to longer-term loans, and that market prices reflect this.

When credit is looser, buyers can expect to face higher prices for used cars. The researchers calculate that if a prospective buyer has an annual discount rate of less than 8.9 percent — that is, the buyer would prefer $100 now rather than any amount less than $108.90 in a year's time — then the benefits of a longer loan term are more than offset by the higher purchase price such loan terms may induce. They point out that increases in the prices of automobiles and other durable goods in periods of relatively looser credit may attenuate the link between credit market changes and aggregate economic activity.

— Morgan Foy