How Does ESG Investing Affect an Institution’s Portfolio Composition?

Financial institutions that mention environmental, social, and governance (ESG) criteria in their investment policies had $35 trillion in assets under management in 2020. To assess how these criteria affect portfolio composition, however, it is necessary to compare their actual portfolio holdings with a counterfactual that describes what their portfolio holdings would have been in the absence of any ESG considerations. In Green Tilts (NBER Working Paper 31320), Lubos Pastor, Robert Stambaugh, and Lucian Taylor estimate the extent to which ESG factors alter investment portfolios.

The researchers first note problems with the usual measure of the amount of ESG investment, which is simply the total assets of institutions declaring an ESG objective. Those institutions hold varying mixes of “green” (ESG-favored) and “brown” (disfavored) stocks. Counting all of their assets as green overestimates the importance of ESG investing. At the same time, institutions that do not explicitly mention ESG criteria in their investment policies might engage in ESG investing. For example, they might expect higher returns on ESG stocks than on other stocks. This would create a downward bias in the estimated importance of ESG considerations.

About 6 percent of US equity investments are explained by “ESG tilt,” much less than the total assets managed by institutions subscribing to ESG principles.

To estimate the importance of ESG investing, the researchers analyze institutional investors’ holdings of US stocks as reported in SEC form 13F filings. The sample includes US-based institutions with more than $100 million in stock investments — a group that includes investment companies, banks, insurance companies, pension funds, and endowments — as well as foreign institutions that hold US stocks.

For each stock held by each institution, the researchers estimate a portfolio allocation share absent any ESG considerations. They define the difference between the observed share and the predicted share absent ESG considerations as the stock’s “ESG tilt” for this institution. They further decompose this tilt into an extensive-margin component, reflecting the institution’s binary decision about whether or not to hold a particular stock, and an intensive-margin tilt, reflecting the amount of the stock held conditional on a positive holding. Intensive-margin tilts are twice as important as extensive ones in their analysis. The researchers aggregate the ESG tilts for specific stocks and institutions to create institution- and market-level estimates of the extent to which ESG considerations affect portfolio composition.

The results suggest that about 6 percent of US equity investment allocations represent ESG tilt, a much lower figure than the percentage of total assets that are held by institutions that subscribe to ESG principles. The aggregate importance of ESG tilts is relatively constant over the 2012–21 period, reflecting a combination of increasing ESG tilts in institutions’ actively managed portfolios, from about 14 percent to 25 percent over the last five years, and a decline in active management by institutional investors over the same period. Passive strategies, such as investing in all of the stocks in a stock index, do not involve any ESG tilt.

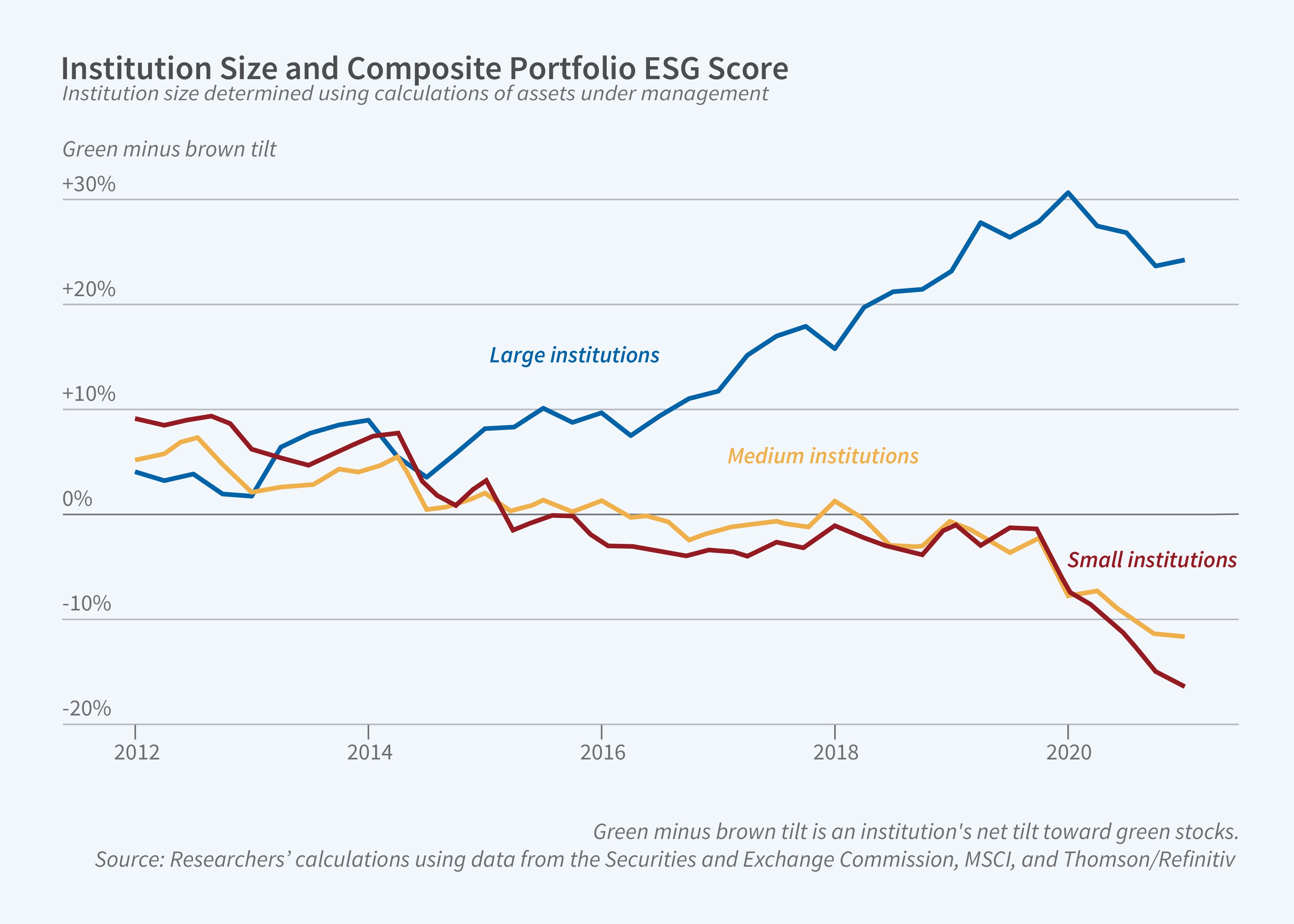

The researchers’ ESG tilt measure reflects the share of an institution’s investment choices that can be explained by stocks’ ESG characteristics, which captures choices that both actively favor green stocks and disfavor brown stocks. The two can be separated. Within the largest firms in the investment industry, green tilts dominate brown tilts, and the strength of green tilts is growing over time. Most of the reductions in brown-stock holdings occur on the intensive margin, rather than as complete divestment.

The extent of green tilt is positively related to the assets under management of the 13F-filing institution. It is also greater for institutions — accounting for 76 percent of the assets under management in the sample — that have signed the United Nations’ Principles for Responsible Investment.

—Shakked Noy