Monetary Policy’s Disparate Impact on Labor Market Subgroups

In tight labor markets, expansionary monetary policy has its largest impact on employment growth for demographic groups with lower than average labor market attachment.

Employment among populations with lower labor force attachment responds more to expansionary monetary policy in tight labor markets than employment among more attached groups, according to Nittai K. Bergman, David A. Matsa, and Michael Weber in Inclusive Monetary Policy: How Tight Labor Markets Facilitate Broad-Based Employment Growth (NBER Working Paper 29651).

The findings suggest that by tightening labor markets, the Federal Reserve’s recent move from strict to average inflation targeting especially benefits workers with lower labor force attachment.

Following its 2020 Monetary Policy Report, the Federal Reserve emphasized maximum employment as a “broad-based and inclusive goal” and stressed the importance of a strong labor market to generate employment gains widely across society. Monetary policy’s effects on different segments of the labor market, however, are not well understood. The researchers seek to address this gap.

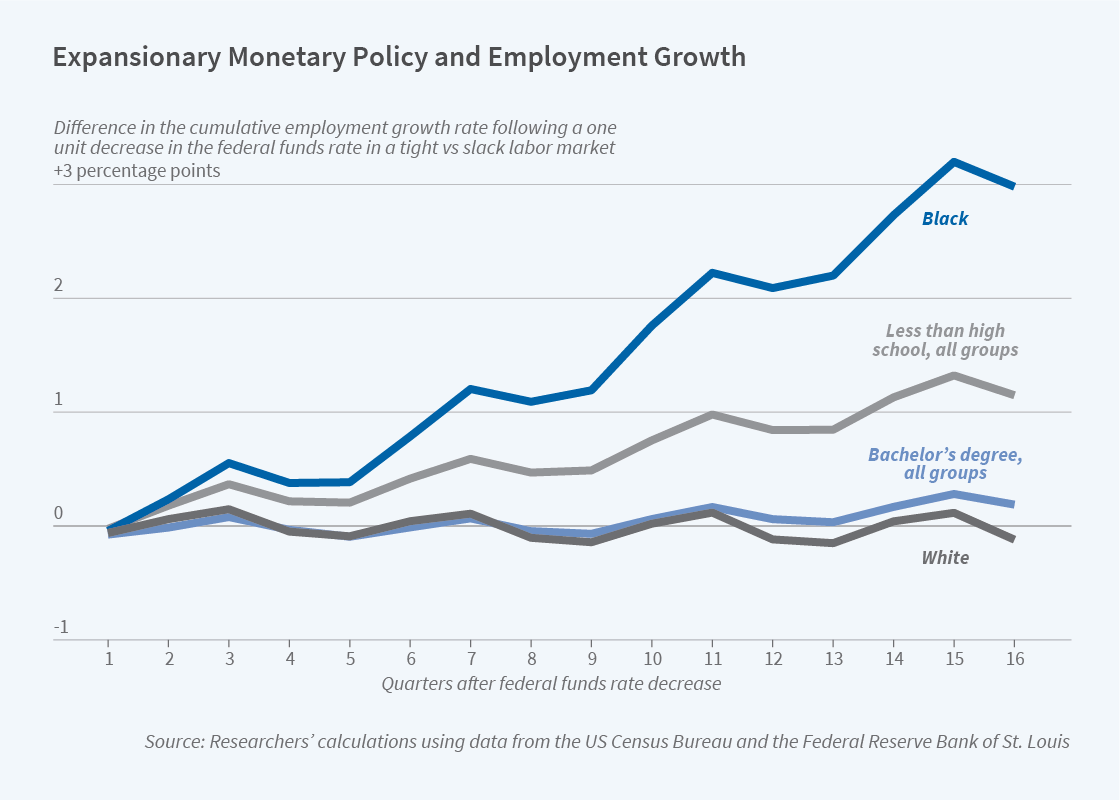

The study tracks the impact of monetary policy on workers in different demographic groups, defined by race, education, and gender. For each group, the researchers estimate how employment growth in 895 local labor markets is related to the federal funds rate and local labor market tightness, which they measure as the market’s aggregate prime-age employment-to-population ratio. They study the period 1990 to 2019. For groups with lower average labor market attachment — Blacks, the least educated, and women — expansionary monetary policy has a larger effect on employment growth in tighter labor markets. For example, they find that a one standard deviation drop in the federal funds rate (2.25 percentage points) increases the Black employment growth rate over the next two years by 0.91 percentage points more in tight labor markets than in slack ones. Similarly, for workers who did not complete high school, a one standard deviation drop in the federal funds rate increases employment growth over the subsequent two years by 0.39 percentage points more in tight labor markets than in slack ones. These differential impacts in tight and loose labor markets represent gains in mean employment growth rates during the sample period of 9 percent for Black people and 18 percent for those who did not finish high school.

The researchers also present a heterogeneous-worker New Keynesian model that provides a framework for interpreting their finding that monetary policy has these disparate effects. Workers are differentiated by their productivity levels, which could vary due to differences in education levels, on-the-job discrimination, or other reasons. The trade-off between unemployment and inflation — the Phillips curve — plays a key role in determining optimal central bank policy in this setting. When the inflationary pressures from a tight labor market are modest, as evidence from the two decades prior to the pandemic suggests, then the central bank can retain low interest rates longer. This expansionary policy results in a higher labor force participation rate for low-productivity workers over time.

The theoretical and empirical results in this study both highlight the role of labor market tightness in mediating the impact of monetary policy on workers with low labor force attachment. They suggest that the Federal Reserve’s recent change in monetary policy regime, from strict to average inflation targeting, will over time increase the labor market activity of demographic groups with lower historical employment rates.

— Lauri Scherer