The Market for Stand-Alone Prescription Drug Insurance

Prescription drugs play an increasingly important role in treating both chronic and acute health conditions, yet many Americans lack insurance coverage for prescription drugs. Medicare, the government health insurance program for seniors and the disabled, provides no coverage for prescription drugs. As a result, one in four seniors has no drug coverage and many others are underinsured. Roughly one-quarter of non-elderly Americans also have no drug coverage, a figure somewhat higher than the share of this population without health insurance.

One possible solution is for insurance companies to offer stand-alone prescription drug insurance plans for purchase by individuals. Like all insurance, prescription drug insurance is potentially plagued by adverse selection, the tendency of those who know they are at higher risk of making a claim to be more likely to purchase the insurance. In extreme cases, the presence of adverse selection can trigger a death spiral, where only the worst risks purchase coverage and the private insurance market collapses. This problem can be avoided if insurers charge higher premiums to high-risk individuals, but insurers may lack the necessary data to determine an individual's risk level or may be prohibited from charging different rates on this basis.

In Adverse Selection and the Challenges to Stand-Alone Prescription Drug Insurance (NBER Working Paper 9919), Mark Pauly and Yuhui Zeng explore the extent to which adverse selection poses a problem in the case of stand-alone prescription drug insurance. Adverse selection is more likely to be a problem if there are large differences in expenditures across people and some persistence in expenditures over time, so that individuals know whether they are at high risk for having large expenditures in the future.

The authors examine the distribution and persistence of drug expenditures using a database of claims for 140,000 insured, non-elderly persons during the 1994-1998 period assembled by the MEDSTAT Group. They find that drug expenditures are highly skewed; in 1994, individuals in the top quintile of the sample (that is, the 20% of individuals with the highest drug expenditures) spent 3.9 times as much the average person in the sample.

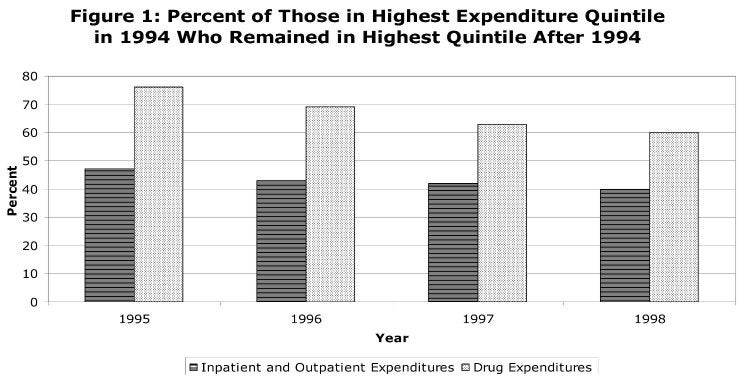

Even more interestingly, the authors find strong persistence in drug expenditures from year to year. As Figure 1 illustrates, 76% of individuals who were in the top quintile of drug expenditures in 1994 were also in the top quintile the following year, and 60%were still in the top quintile four years later. The degree of persistence in drug expenditures is substantially higher than that in inpatient and outpatient expenditures, suggesting that adverse selection is likely to be more of a problem for stand-alone prescription drug insurance than for health insurance. Moreover, the authors find that persistence in drug expenditures rises with age, suggesting that adverse selection is more of a problem for prescription drug insurance plans aimed at seniors.

Finally, the authors undertake a simulation exercise to explore whether a death spiral is likely to occur in the market for stand-alone prescription drug insurance. The exercise involves first predicting an individual's expected health expenditures for the next year based on their age, gender, and current expenditures and calculating the uncertainty surrounding this estimate. The authors then estimate what each individual would be willing to pay for insurance to eliminate the uncertainty in expenditures and determine which individuals would choose to purchase insurance.

The findings from this exercise are striking. When drug coverage is offered as part of a total health insurance plan, virtually all individuals choose to purchase insurance. When stand-alone drug coverage is offered, a death spiral occurs and only very high-risk individuals choose to purchase insurance. The logic for this finding is simple - for a low-risk individual, the premium is much higher than the expected expenditures next year, and because prescription drug expenses are relatively predictable, the individual is not willing to pay much to eliminate the small risk of high expenditures and opts out of the insurance. By contrast, health insurance expenditures as a whole are less predictable, so the individual is willing to pay more to eliminate the risk and chooses to buy the insurance.

The authors conclude that subsidies for stand-alone prescription drug plans, a potential solution sometimes mentioned in the current discussion of how to extend drug coverage to the Medicare population, would need to be on the order of 70-90% of the premium to entice most seniors to join such plans.

This research was supported by the Merck Company Foundation, but reflects only the views of the authors, not of the Merck Company Foundation. The research was summarized by Courtney Coile.