Co-Directors

Andrea Eisfeldt holds the Laurence D. and Lori W. Fink Endowed Chair in Finance at the UCLA Anderson School of Business. Her research has focused on topics including market liquidity, the role of intangibles in asset pricing, bank valuation, and macro-finance. She has been an NBER affiliate since 2014.

Sydney C. Ludvigson is the Julius Silver, Roslyn S. Silver, and Enid Silver Winslow Professor of Economics at New York University. Her research focuses on the interplay between asset markets and macroeconomic activity. She has been an NBER affiliate since 2003.

Featured Program Content

The US stock market has become more concentrated in recent years. Between 2015 and 2024, the share of the 10 largest stocks in total market capitalization rose...

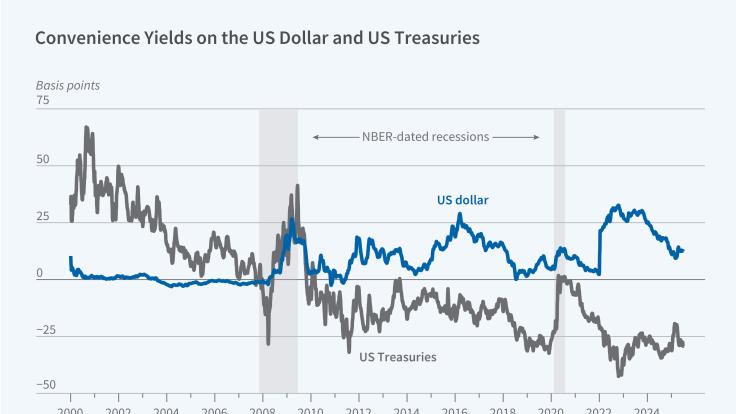

In Decoupling Dollar and Treasury Privilege (NBER Working Paper 35000), Wenxin Du, Ritt Keerati, and Jesse Schreger document a pronounced divergence...

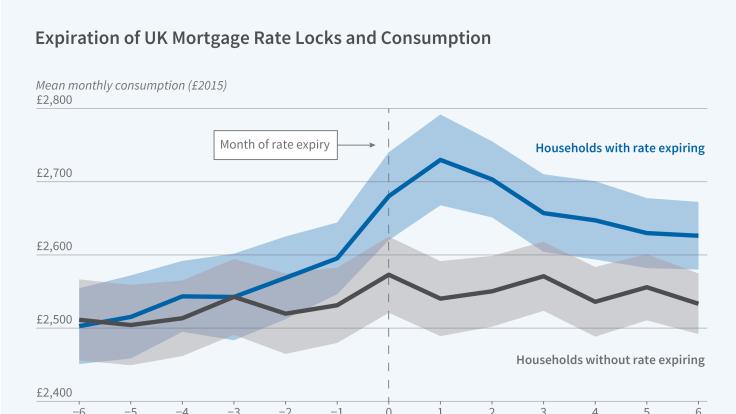

Interest rates on most UK mortgage products are fixed for shorter periods than the interest rates on US mortgages. They typically require borrowers to...